You didn’t just think that there were only immediate and deferred annuities did you? Within each, there are fixed and variable categories.

While this was briefly discussed in the section above, it’s generally accepted that there are five basic annuity types;

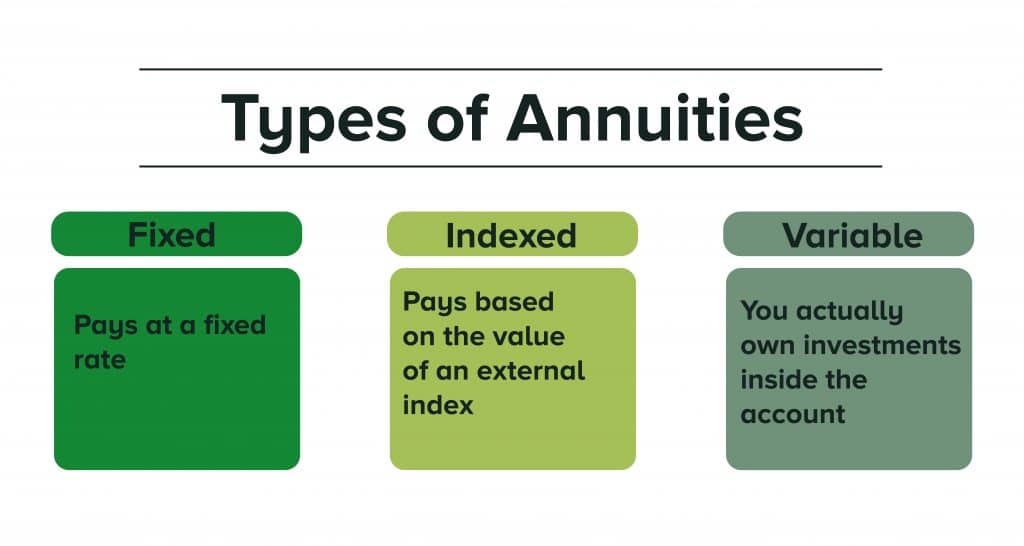

- Fixed annuity. A simple, straightforward option that’s similar to a CD. You’re guaranteed a fixed interest rate on your investment that could last anywhere between a year and the full length of your guarantee period. There are two types of fixed annuities, traditional fixed and Multi-Year Guarantee Annuity (MYGA).

- Variable annuity. A tax-deferred investment product with the highest upside. You can participate in investments including stocks, bonds, and mutual funds. However, you may lose your principal.

- Fixed indexed annuity. You’re able to earn interest from market exposure. But, if the market tanks, the interest rate is guaranteed to never be less than zero.

- Immediate annuity. With this type, you exchange a lump sum payment into a series of payments. These are guaranteed for the specified period of the contract. Income checks start right away.

- Deferred annuity. An easy-to-understand annuity where you pay a lump sum of money upfront today for recurring payments at a later date.

However, let’s dig even deeper and rundown the following types of annuities. Again, all of these will be either available in fixed or variable form.

Fixed vs. Variable Annuities

A fixed annuity, according to the Insurance Information Institute, is when “the insurance company guarantees the principal and a minimum rate of interest.” To put that in layman’s terms, “as long as the insurance company is financially sound, the money you have in a fixed annuity will grow and will not drop in value.”

“The growth of the annuity’s value and/or the benefits paid may be fixed at a dollar amount or by an interest rate, or they may grow by a specified formula,” adds the III. “The growth of the annuity’s value and/or the benefits paid does not depend directly or entirely on the performance of the investments the insurance company makes to support the annuity.”

There are some fixed annuities “credit higher interest rate than the minimum, via a policy dividend that may be declared by the company’s board of directors.” But, this will only occur “if the company’s actual investment, expense and mortality experience is more favorable than was expected.”

And, it should be known that fixed annuities are regulated by your state’s insurance departments.

What else should I know about fixed and variable annuities?

If you have money placed in a variable annuity, then it’s actually invested into a fund, like a mutual fund. The thing is, it’s only accessible to investors who happen to be “in the insurance company’s variable life insurance and variable annuities,” explains the III. “The fund has a particular investment objective, and the value of your money in a variable annuity—and the amount of money to be paid out to you—is determined by the investment performance (net of expenses) of that fund.”

A majority of “variable annuities are structured to offer investors many different fund alternatives.” And, just like fixed annuities, variable annuities are regulated by state insurance departments. But, they’re also kept in check by the Federal Securities and Exchange Commission.

Types of Fixed Annuities

Did you also know that there are a couple of different types of fixed annuities? If not, consider yourself newly informed.

The first is an equity-indexed annuity. Yes. It’s a fixed annuity. At the same time, the rate of interest is linked to the returns of an index, such as the S&P 500. This hybrid annuity “credits a minimum rate of interest, just as a fixed annuity does, but its value is also based on the performance of a specified stock index—usually computed as a fraction of that index’s total return,” clarifies the III.

The second type is what’s known as a market-value-adjusted annuity. It “combines two desirable features—the ability to select and fix the time period and interest rate over which your annuity will grow, and the flexibility to withdraw money from the annuity before the end of the time period selected,” states the III.

If you want to withdraw, this product type offers more flexibility. The reason is that it adjusts “the annuity’s value, up or down, to reflect the change in the interest rate ‘market’ (that is, the general level of interest rates) from the start of the selected time period to the time of withdrawal.”

But, wait, there’s more…

If you recall, there were deferred and immediate annuities. But, there are also the following types of annuities — which are available in fixed or variable forms.

Lifetime vs. Fixed Period Annuities

With a fixed period annuity will receive an income within a specified period of time, like five or ten years. What’s great about this type is that your age doesn’t influence how much your payments will be. Instead, payments are dependent “on the amount paid into the annuity, the length of the payout period, and (if it’s a fixed annuity) an interest rate that the insurance company believes it can support for the length of the pay-out period.”

A lifetime annuity, as you might assume, provides income for the remainder of your life. As the III adds, there’s also a variation of lifetime annuities that will continue “income until the second one of two annuitants dies. No other type of financial product can promise to do this.”

How much will you get paid? That does depend on your age, “the amount paid into the annuity, and (if it’s a fixed annuity) an interest rate that the insurance company believes it can support for the length of the expected pay-out period.”

There’s also something known as a “pure” lifetime annuity. It’s a lifetime annuity with the caveat that payments cease when the annuitant dies — regardless if not much time has passed since they began. Suffice to say, a lot of annuity buyers are uncomfortable with this possibility.

To put them a little more at ease, annuity companies add a guaranteed period. It’s pretty much a fixed period annuity that’s in addition to their lifetime annuity. That means when you have this combination, and you pass away “before the fixed period ends, the income continues to your beneficiaries until the end of that period.”

Qualified vs. Non-Qualified Annuities

Do want an annuity that can be invested and dispersed into a tax-favored retirement, such as an IRA? If so, then you’re in luck thanks to a qualified annuity.

With this type of annuity, the premiums or contributions that you make towards an IRA or Keogh plan or plans governed by Internal Revenue Code sections, 401(k), 403(b), or 457, are not classified as taxable income for the year that it was paid. “All other tax provisions that apply to non-qualified annuities also apply to qualified annuities,” notes the III.

Since there’s a qualified annuity, then there has to be a non-qualified annuity as well. After all, you can’t have yin without yang. With this type, it would be purchased separately from, or “outside of,” a tax-favored retirement plan. “Investment earnings of all annuities, qualified and non-qualified, are tax-deferred until they are withdrawn; at that point, they are treated as taxable income (regardless of whether they came from selling capital at a gain or from dividends),” the III explains.

Single-Premium vs. Flexible Premium Annuities

Still hungry for more annuities? Hope you have a healthy appetite because we have a couple more annuity types to present.

A single premium annuity is an annuity funded by, well, a single payment. You can then invest the payment for the long haul with a single premium deferred annuity. Or, it can be “invested for a short time, after which payout begins—a single premium immediate annuity,” states the III.

“Single premium annuities are often funded by rollovers or from the sale of an appreciated asset.” Examples include publicly traded securities, real estate, and personal property.

On the flip side, there’s also a flexible premium annuity. It’s “an annuity that is intended to be funded by a series of payments,” explains the III. “Flexible premium annuities are only deferred annuities.” That means “they are designed to have a significant period of payments into the annuity plus investment growth before any money is withdrawn from them.”

Did you save room for dessert? We hope so. Because there are even more annuity variations to briefly go over.

Registered Index-Linked Annuity

A registered index-linked annuity (RILA) is a tax-deferred long-term savings option. Its key feature is that it limits exposure to downside risk, while also providing growth opportunity. It has more potential for growth than a fixed-indexed annuity, but the potential return could be less.

And, it also has less risk than a variable annuity.

Part of the return performance will be based on an underlying index or indexes. Furthermore, RILAs provide an option to convert the annuity into a stream of income payments in retirement — this would through annuitization. And, since a RILA is not a stock market investment, there’s no direct participation in any stock or equity investments.

Ultimately, with a RILA, you’re accepting a level of risk in exchange for higher upside potential.

Long-Term Care Annuity

This is a deferred fixed annuity (hybrid annuity). It’s designed to help pay for long-term care costs so that you aren’t draining your retirement savings. An LTC annuity can assist you in paying for a nursing home, assisted living, home healthcare, chronic illness, and terminal illness expenses. An alternative to this would be adding a long-term care rider to a deferred annuity.

While there are similarities, an LTC differs from long-term care insurance in a couple of ways. Mainly, there isn’t a growth component and if you don’t need long-term care, the premiums will not be paid back — unless you added on a return of premium rider. With a long-term care annuity, you may be able to receive annualized payments regardless if you use the long-term care rider’s benefits or not.

The Medicaid Annuity

An MCA is a unique Single Premium Immediate Annuity. It’s meant to help cover a person’s nursing home care and medical bills if eligible for Medicaid.

“Medicaid-compliant annuities are the greatest planning tools if you have a loved one in a nursing home and you are trying to get Medicaid benefits,” says Patrick Simasko, a financial advisor and estate planning attorney at Simasko Law in Mount Clemens, Michigan. Still, he says, “they are very complicated, so you definitely need an expert to put a Medicaid plan together.”

Secondary Market Annuity

Do you need to sell your annuity? Maybe because you need to pay for an unexpected medical expense? If so, you are able to sell your annuity. When you do sell your annuity to a third party, this is called a secondary market annuity, or SMA for short.

The process is fairly straightforward. First, contact a representative from an annuity buyer. You may want to get a referral from your financial advisor first or research the company known for its service. Next, receive a quote and consult with a financial planner.

And, if you agree to the sale, complete the required paperwork. Once approved by either a court or insurance company, you’ll receive your cash in a lump sum.

Two-Tiered Annuity

“A two-tier annuity has two different interest rates, depending on how long you hold the annuity,” explains Denise Sullivan for Zacks. “If you hold onto your annuity until its maturity date, you will be entitled to an interest rate that is higher than the rate on a comparable single-tier annuity.” But, “if you decide to cash out the annuity before this date, your earnings will be retroactively adjusted down to a much lower rate.”

Two-tier annuities are known for producing higher returns than traditional annuities. However, it’s difficult to access your money. Moreover, this type of annuity is extremely rare these days so you probably won’t hear much about it.

Qualified Longevity Annuity Contract

A QLAC is a Deferred Income Annuity (DIA). It allows owners of a traditional IRA and defined contribution plan participants to ignore the QLAC funds in those accounts when calculating their Required Minimum Distributions (RMDs). In other words, this permits you to defer income past the age of 72.

Another advantage of a QLAC is that you can delay the beginning of receiving payments–up to age 85. Therefore, this eliminates the concern of outliving your savings. And, the longer you delay these payments, the higher your payout will be.

There are two limitations to a QLAC though. The first is that you can not exceed $135,000 in total lifetime contributions across all funding sources. And, second, QLAC contributions cannot exceed 25% of that specific funding source’s value.

The Charitable Gift Annuity.

“A charitable gift annuity is an arrangement between a donor and a non-profit organization in which the donor receives a regular payment for life-based on the value of assets transferred to the organization,” explains Troy Segal for Investopedia. “After the donor’s death, the assets are retained by the organization. The charitable gift annuity is a type of planned giving.”

“Such annuities are set up by an agreement between the charity and the individual annuitant or couple,” he adds. “The annuities simultaneously provide a charitable donation, a partial income tax deduction for the donation, and a guaranteed lifetime income stream to the annuitant and sometimes a spouse or other beneficiary.”

Structured Settlement

This is a settlement that’s derived and negotiated from the result of an individual winning a civil case. As an example, you were in a car accident and won a personal injury lawsuit. A settlement is negotiated and you’ll receive a lump sum of cash upfront to cover immediate expenses. This is often followed by a series of guaranteed payments over an agreed amount of time.

Generally, settlement scenarios include a personal injury case, workers compensation case, medical malpractice, and wrongful death claims.

And, overall, you can think of a Structured Settlement that has a court-ordered SPIA.

Putting it All Together

As you can see, there are more types of annuities than just the five that are discussed the most. But, do you need to memorize all of these different types? Of course not.

Some annuity types will never apply to you because they’re outdated, think the two-tier annuity. Others you just won’t have a need to be concerned with. For instance, if you’re not invited to a personal injury case you don’t have to be familiar with a structured settlement.

The main takeaway should be this, the different types of annuities are based on two primary factors; when you want to start receiving payments and how you would like your annuity to grow.

- When you begin receiving payments. You can either have money today or for the rest of your life.

- How your annuity investment grows. Annuities typically grow through interest rates (rates) or investing contributions into the market (variable).

Determining which annuity is right for you involves reviewing your goals, financial situation, and values. And, before making a final decision, speak with a financial advisor.

- What Is an Annuity?

- The Difference Immediate Annuities and Deferred Annuities

- How does an annuity work?

- The Benefits of a Deferred Annuity

- The Benefits of an Immediate Payment Annuity

- What Is a Variable Annuity?

- What Is a Fixed Index Annuity?

- What Is an Indexed Annuity?

- A Brief History of Annuities

- Will Annuities Recover?

- Money for Today or the Rest of Your Life?

- Are There Any Other Types of Annuities?

- Become Familiar With Annuity Fees

- What Are Your Payout Options?

- Weighing the Pros and Cons of Annuities

- Is An Annuity Right For You?

- How To Measure Your Annuity

- Understanding Annuity Formulas

- Annuity Calculators

- Questions To Ask Before Buying An Annuity

- Annuity Glossary Index