401(k) plans are usually delivered by employers. They’re managed by financial funds and they’re usually tax-deferred—your employer makes your contributions on your behalf with pre-tax dollars. You only pay the tax on that income after you retire and start receiving the funds.

They’re also limited. You can’t put as much as you want into your 401(k) on a tax-deferred basis.

IRAs are even more limited. While you can choose your own IRA, you can usually place no more than $500 a month into your account.

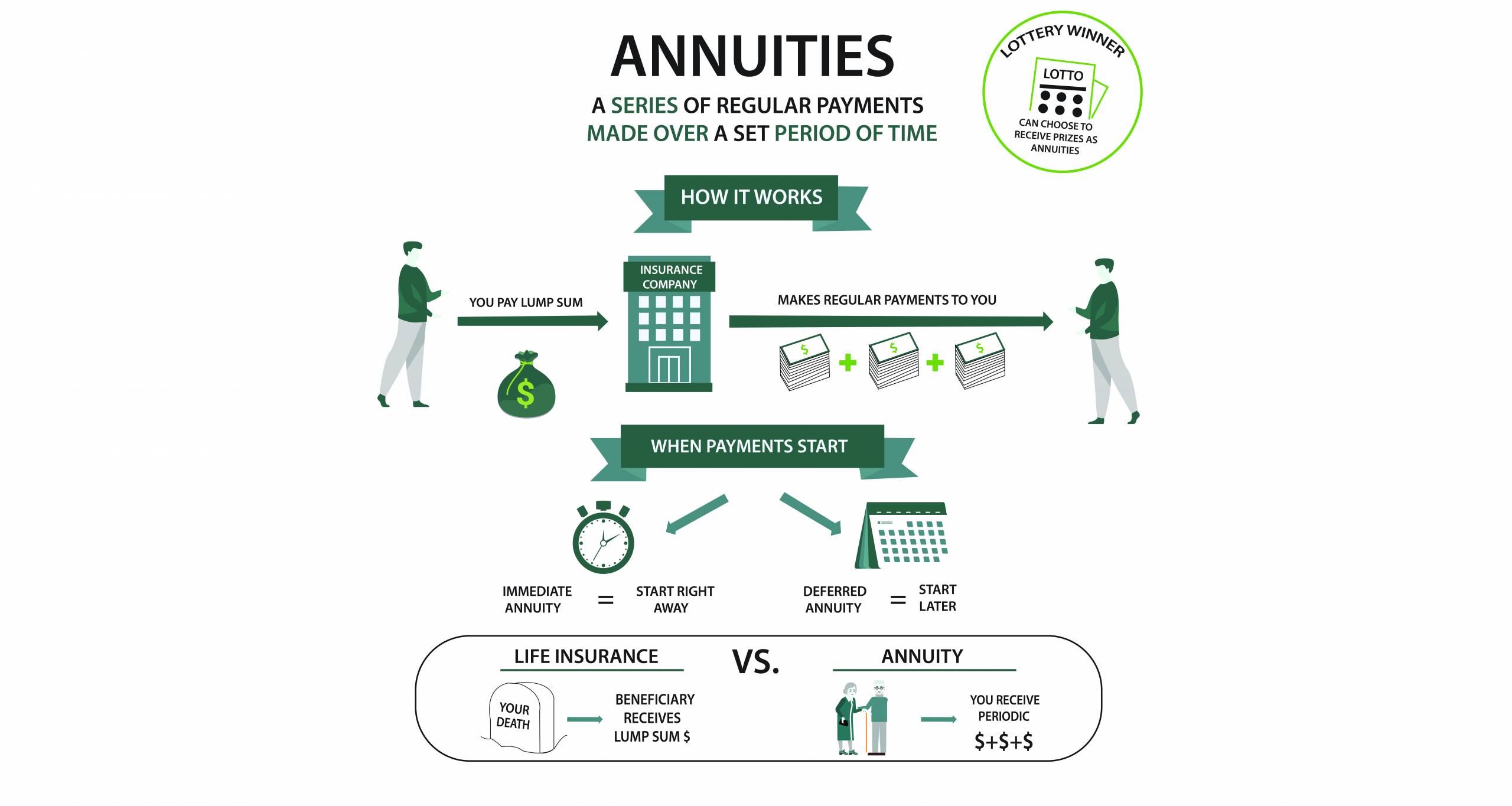

Retirement annuities are contracts with insurance companies. Like IRAs and 401(k) plans you can make contributions using pre-tax dollars and receive a monthly income in return.

The contents of the fund then grows on a tax-deferred basis, with no tax due until retirement. But there are no limits on the contributions you can make. You can put as much money into an annuity as you want.

That makes them valuable additions to your retirement planning toolkit.

If you’ve maxed out your 401(k) and your IRA, then buying an annuity can help you to continue shoveling money into the future and lowering your tax bill.