Last updated: July 2026

Like 401(k) plans, IRAs can come in a range of different flavors. Savers have different ways to prepare for their futures based on the levels of their income and their tax liability.

There are 3 different types of IRAs;

- Traditional IRA

- Roth IRA

- SEP IRA

Today we break down the three different types of IRAs:

The Traditional IRA

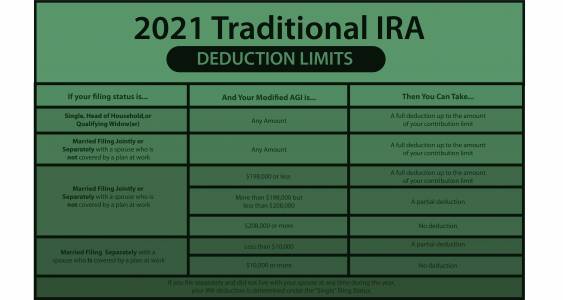

The traditional IRA is the plan you’re likely to be most familiar with. It works like a traditional 401(k) but with lower contribution limits, with deductions that can phase out as your income rises, and with a free choice of retirement funds.

Like a traditional 401(k), contributions are made pre-tax. If you want to know how these accounts stack alongside a workplace plan, see whether you can have a pension, a 401(k) and an IRA at the same time. The funds then grow and gain in interest without collecting tax liabilities until the payouts begin between the ages of 59½ and 73. At that age, your income is likely to be lower so the amount of taxes you have to pay should be lower too.

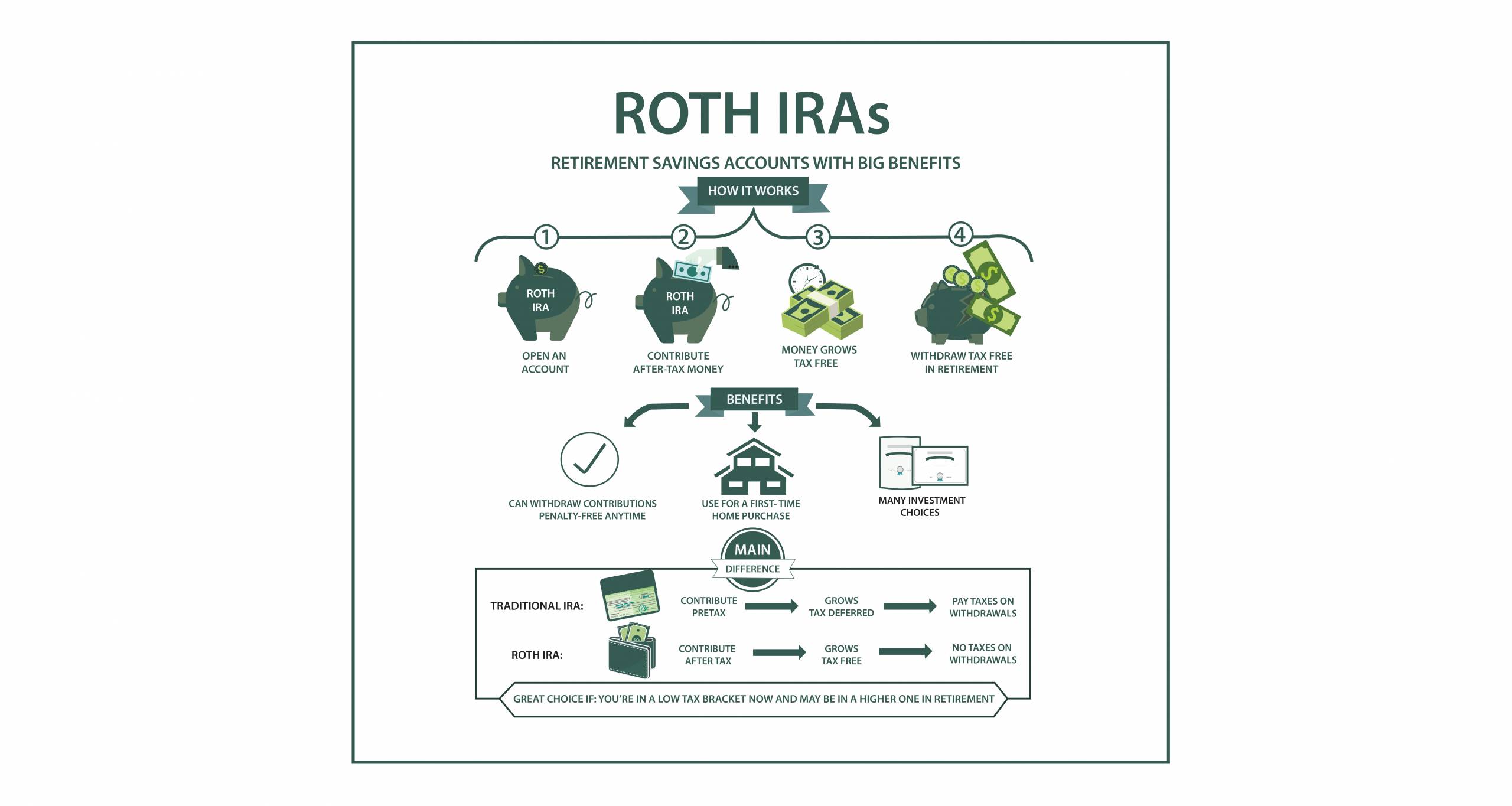

The Roth IRA

Just as 401(k) plans have Roth 401(k) plans, so IRAs also have their own Roth versions. For IRAs though they come with some special provisions.

Like Roth 401(k) plans, savers make their contributions with after-tax dollars. They’ll pay tax on their income, then put money into their Roth IRA. Those funds continue to grow and the distributions are tax-free. As you near retirement, many savers shift a portion of their IRA toward low-risk investments to protect what they’ve built.

In general, Roth plans are useful for people who expect to have a higher income after they retire than when they make their contributions.

Roth IRAs also keep the IRA contribution limit. Whether you use a Roth IRA or a traditional IRA, your combined contributions cannot exceed the annual IRA contribution limit, which the IRS adjusts periodically, with an additional catch-up amount allowed once you’re aged 50 or over.

But there are some additional conditions. First, Roth IRAs aren’t available to high earners. Above certain income thresholds, which the IRS sets and adjusts each year, your ability to contribute to a Roth IRA phases out and eventually disappears, so it’s worth confirming the current figures before you contribute.

On the other hand, once you’ve put money into your Roth IRA you can keep it there. While traditional 401(k) plans and IRAs require savers to start taking distributions at age 73 so that the tax authorities can get their share, your Roth IRA can remain untapped for as long as you want. That flexibility matters if you’re planning an early exit from work — for example, running the math on whether you’re able to retire at age 55.

It is important to note though that you can only contribute earned income to a Roth IRA. You can’t use it to hold rental income, capital gains or stock dividends and other passive income, interest from loans, or the proceeds from another retirement fund. It has to be money that you’ve made through work.

The SEP IRA

The big limitation of a 401(k) is that it can be complex and expensive. Companies don’t have to offer them and while a company that doesn’t provide a 401(k) plan will look less attractive to potential employees, some small companies just can’t afford them.

The big limitation of an IRA is its low contribution limits. There’s a good chance that you’ll want to contribute more to your retirement fund than the standard annual IRA contribution limit allows.

A Simplified Employee Pension, or SEP, IRA solves both those problems. It takes some elements of a 401(k) and some elements of an IRA. The result is a retirement fund that’s delivered through employers, gives employees some degree of control over the investments, and has relatively high contribution limits.

The role of an employer is the first important difference between a SEP IRA and other IRAs. Sole proprietors, partnerships, and corporations can all set up SEP IRAs. That lets them give their employees a retirement fund with contributions coming from pre-tax earnings. SEP IRAs enjoy the same deferments as traditional IRAs.

Which Type of IRA Is Right for You in 2026?

Choosing among the three types of IRAs comes down to three questions: how you want your money taxed, whether you are self-employed, and how much you want to contribute each year. A Traditional IRA gives you a tax break now and taxes your withdrawals later, a Roth IRA is funded with after-tax dollars so qualified withdrawals are tax-free, and a SEP IRA lets business owners and the self-employed set aside far more than a standard IRA allows.

Traditional vs. Roth: It Comes Down to Taxes

The core decision for most savers is Traditional versus Roth. If you expect to be in a lower tax bracket in retirement than you are today, the upfront deduction of a Traditional IRA is appealing. If you expect your income, or tax rates generally, to be higher later, paying tax now through a Roth IRA can be the smarter long-term move. Many people hedge by holding both. Whichever you choose, pair it with low-cost investments such as the top index funds for retirement to keep more of your returns.

The SEP IRA for the Self-Employed

If you freelance, run a small business, or earn 1099 income, a SEP IRA is worth a close look because its contribution ceiling is far higher than a Traditional or Roth IRA. It is simple to administer and contributions are generally tax-deductible to the business. For a broader view of how tax-advantaged accounts fit together, compare the trade-offs in our guide to annuities vs. a 401(k) and learn how hidden 401(k) fees can quietly shrink your savings.

Mind the Annual Limits and Income Rules

The IRS sets contribution limits and income phase-outs that change periodically, and Roth IRAs are off-limits to very high earners. Rather than rely on last year’s figures, confirm the current numbers directly with the IRS before you contribute. You can review the official rules on the IRS Individual Retirement Arrangements page. Once your account is open, focus on growth: see how to get good investment returns as a beginner and ways to protect your retirement savings from inflation.

Key Takeaways

Traditional, Roth, and SEP IRAs each solve a different problem: a deduction today, tax-free income tomorrow, or a higher ceiling for the self-employed. Match the account to your tax outlook and work situation, verify the current limits with the IRS, and invest your contributions rather than leaving them in cash.

Frequently Asked Questions

What are the three main types of IRAs?

The three most common types are the Traditional IRA, the Roth IRA, and the SEP IRA. Traditional and Roth IRAs are available to most individuals with earned income, while the SEP IRA is designed for self-employed people and small-business owners who want higher contribution limits.

Can I contribute to both a Traditional and a Roth IRA?

Yes. You can split contributions between a Traditional and a Roth IRA in the same year, but your combined contributions cannot exceed the single annual IRA limit set by the IRS. High earners may also face income limits that reduce or eliminate Roth eligibility.

Which IRA is best for self-employed workers?

A SEP IRA is often the best fit for freelancers and business owners because it allows much larger contributions than a Traditional or Roth IRA and is easy to set up. Those who want even more flexibility sometimes compare it with a solo 401(k) before deciding.

Related Reading: Just getting started? See how investing $50 a month can compound into real wealth.

Related Reading: Not sure which IRA fits? Try retirement planning with ChatGPT to model the trade-offs first.