Payment processing in 2016 was a busy, and surprising. 2016 was the year for payment processing thanks technological advances, to the Millennials, and because of the transition to EMV. That was just the beginning.

As we get ready to usher in 2017, let’s take a look back at the biggest events in payment processing in 2016.

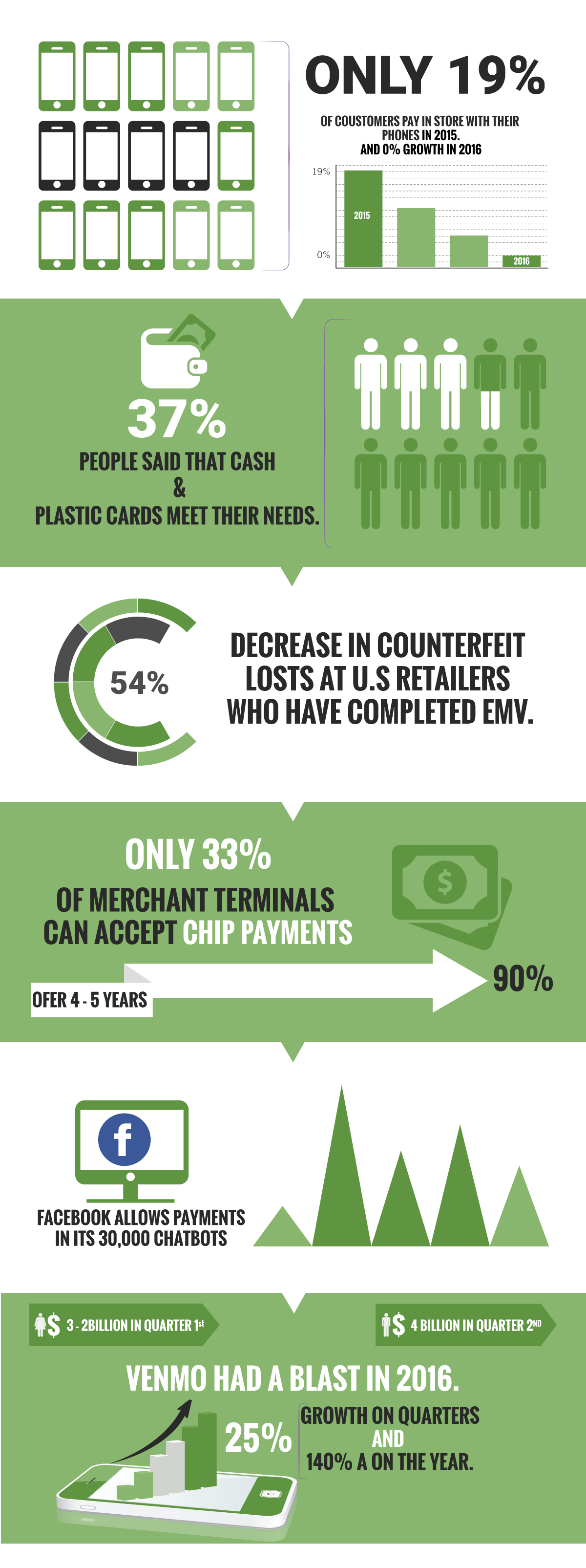

Mobile payments didn’t grow.

According to Accenture’s 2016 North America Digital Payments survey, “Making payments is part of consumers’ everyday lives,” the report states. “Before long, making digital payments will be too. Because after years of steady momentum, digital payments is on the verge of becoming mainstream—and there’s no turning back.”

However, here’s where things get interesting. “Even so, the use of mobile payments at the point of sale, which represents a significant portion of transaction volumes, is limited. Just 19 percent of consumers pay in store with their phones like last year.”

If you read that again it, it means that there was a zero percent growth in mobile payments at point of sale (POS).

The reason?

“Those who have yet to (37 percent) point to a simple reason why. eCash and plastic cards meet their needs. The reality, too, is that merchants have been slow to invest in modern card readers. Even if people want to pay by smartphone, they often cannot.”

Retailers fought back.

Business have been dealing with the headache of interchange for decades. But, in 2016, they began pushing back. Walmart Canada, for example, stopped accepting Visa in several high profile Canadian stores in order to negotiate more favorable terms.

Here in the States, there were several lawsuits brought on by retailers against Visa and MasterCard, which resulted in the appeals court rejecting a $5.7 billion card fee settlement of claims that they improperly fixed credit-card swipe fees.

EMV transition happened slowly.

It was a bit chaotic when the EMV liability shift occurred on October 1, 2015. However, the transaction has been relatively smooth, despite it going slower than expected.

The majority of Americans feel positively about the chip cards and chips have made credit card transactions safer. In fact, there was a 54 percent decrease in counterfeit fraud costs at U.S. retailers. These are retailers who have either completed EMV adoption or are close to completion.

However, only 33 percent of merchant terminals can accept chip payments. And, Visa believes that it’s going to take another 4 to 5 years to reach the expected 90 percent.

As a result, there are still cases of high levels of post-liability chargebacks. This forced Visa and MasterCard “to delay the U.S. domestic AFD EMV activation date from October 1, 2017 to October 1, 2020.”

Alipay goes global.

Alipay, the payment app run by Alibaba’s affiliate, Ant Financial, launched in Europe so that Chinese tourists could pay for things while traveling abroad. This was the company’s biggest push out of Asia yet. And, this could just be the beginning.

“The vision is targeting two billion people within next five to ten years. Not only in China but other countries too,” Sabrina Peng, president of Alipay International, told CNBC.

Facebook Messenger has allowed payments in its 30,000 chat bots.

Facebook’s head of Messenger David Marcus, announced at TechCrunch Disrupt SF 2016 in September that Messenger bots are now able to accept payments natively without sending users to an external website and is working with Stripe, PayPal, Braintree, Visa, MasterCard, and American Express.

PayPal partnered with Visa and MasterCard.

Paypal and credit card companies have been battling for years because it encouraged users to fund accounts via ACH, as opposed to a credit card. This year, PayPal, Visa, and MasterCard reached a partnership that would allow PayPal to enter the POS transactions market. With its new integrations into MasterPass and Visa Checkout, PayPal will not encourage MasterCard cardholders to link to a bank account via ACH.

The blockchain entered the spotlight.

Blockchain payment processing in 2016 saw distributed ledger technology finally enter the mainstream as major institutions began embracing and investing in blockchain technology.

Furthermore, financial professionals began to understand that blockchain’s value goes beyond cryptocurrency, and that it doesn’t have operate anonymously.

Because of this, expect 2017 to be blockchain’s banner year.

MCX went down.

The Merchant Customer Exchange announced in May that it was postponing the nationwide rollout of the smartphone app CurrentC. CurrentC would have been a rival to Apple Pay and Android Pay. This is after Walmart, CVS, and Kohls launched their own apps.

Some believe that it was doomed from the start since it used outdated technology, offered poor security, and came at a time when new retailers began transitioning to EMV-ready POS terminals, which also support NFC-technology. This allowed for more merchants to accept payment options like Apple Pay.

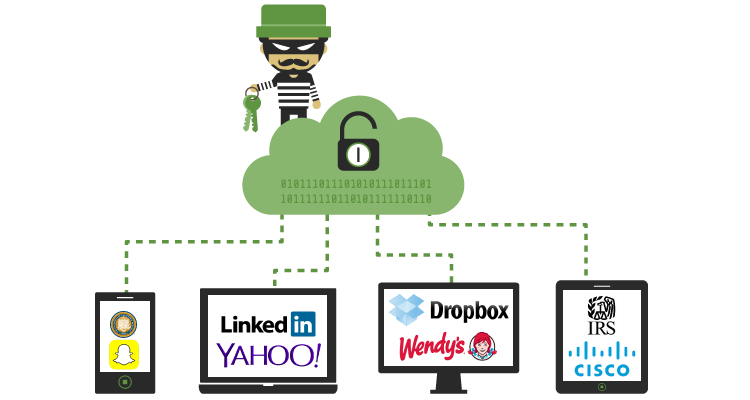

Data breaches.

2015 was one of the worst years for data breaches. And, payment processing in 2016 wasn’t much better. Organizations ranging from the Department of Justice, the IRS, U.S. Berkeley, Snapchat, Yahoo, Dropbox, LinkedIn, Wendy’s, and Cisco were all compromised.

While these didn’t necessarily impact the payment industry, and we’re fortunate enough not to have any high-profile consumer incidents, it proves that customers, retailers, and payment processors need to remain vigilant and make security a priority to prevent any disastrous data breaches.

Same-day ACH.

In September the ACH (automated clearinghouse or eCheck) network opened two new clearing windows which allowed for same-day settlement of transactions. During its first full month of processing, the network processed around $5 billion in same-day transactions – primarily for transactions regarding business-to-business and emergency payroll.

Currently, only ACH credits qualify for same-day clearing. However, ACH debits will occur in September 2017, which should be used for consumer bill pay.

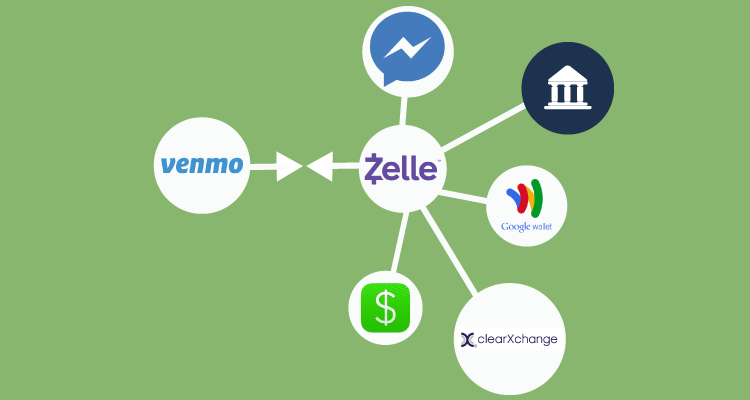

Venmo grew, but facing more competition.

Venmo had a solid 2016 – to put it lightly. “Specifically, Venmo processed $4 billion in transactions in Q2, compared with $3.2 billion the quarter previous. This is 25 percent growth on the quarter, and 140 percent growth on the year,” notes Bank Innovation. At this pace, Venmo is destined to become larger than any other bank P2P service.

But, Venmo could be face stiff competition from Zelle. Zelle is backed by the biggest banks in the U.S., Facebook Messenger, Square Cash, ClearXchange, and Google Wallet.

Emerging and developing nations working on becoming cashless.

Sweden may be on it’s way to becoming cashless society. Emerging and developing countries in Asia, Africa, and South America have experienced mobile payment growth. As technology becomes more affordable it’s dropping the barrier to entry. In India, for example, the digital wallet Paytm, added 10 million new users, growing its base to 160 million, in the month following India’s rupee crisis in November.

The retailer mobile wallet returns.

For the last several years digital wallets like Apple Pay, Samsung Pay, and Android have been battling for position and market share. However, retailers like Walmart, Starbucks, and Kohl’s have all successfully launched their own wallets this year.

Unlike mobile wallets like Apple Pay, retailer wallets allow for tighter control of the point-of-sale experience, as well as the integration of store rewards programs.

Payment Processing in 2016 and Beyond

It has been an exciting 2016 for the payments industry, and 2017 doesn’t look to disappoint, as we see exciting new players from all over the globe entering the playing field of payments.