You can help your relatives immensely by setting up an estate plan now, regardless of who you are. Essentially, whatever you own makes up your estate. These assets could be:

- Any property your own

- Whatever money you have in a bank account

- Stocks, bonds, and mutual funds invested through a taxable brokerage account

- A Roth IRA

- Your prized vinyl, stamp, coin, or art collection

Having a say in how your estate is distributed is essential to your estate planning. Although it may seem daunting, saving your loved ones thousands of dollars will likely be worth the effort now.

In short, you and your family can benefit from estate planning regardless of your net worth.

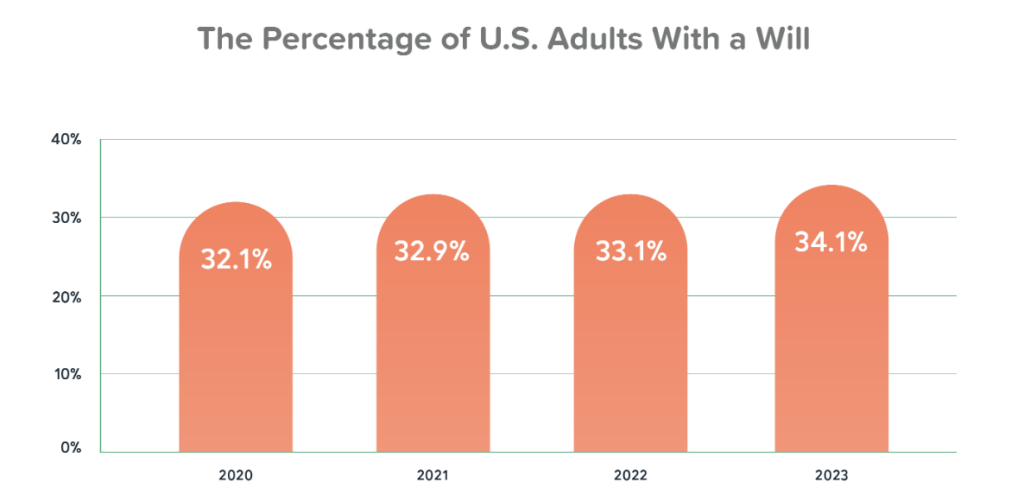

Despite this, 2 out of 3 Americans do not have any type of estate planning document, according to a survey conducted by Caring.com.

“Estate planning is one of the crucial elements of a comprehensive financial plan, but somehow is also the most overlooked component, with the majority of adults not having any form of estate planning document,” says Patrick Hicks, General Counsel and Head of Legal at Trust & Will. “Having an estate plan is a continuation of financial planning and essential to ensure that your efforts to provide for your loved ones last into the future and act as a foundation to build multigenerational wealth and leave a legacy.”

What is Estate Planning?

In essence, estate planning is deciding how you want to distribute your assets after you die — or become incapable of making financial decisions for yourself. If you have trouble putting together an estate plan, and have the funds, consult a financial adviser and a lawyer.

Again, whether you’re broke or not, an estate plan is essential. Even though estate planning may seem morbid, it has several advantages:

- Your wishes will be legally binding when deciding who gets your assets.

- In order to minimize your estate’s tax burden, you can arrange it in a way that minimizes taxes.

- The peace of mind of knowing that your financial affairs are in order means that your loved ones won’t inherit an administrative nightmare.

There are several elements to an estate plan, including:

- A will.

- Having someone you name to manage your finances if you are unable to do so is called an assignment of power of attorney.

- An advanced directive, also called a living will, expresses your wishes for life-sustaining medical interventions if you are terminally ill or incapable of communicating for yourself

- You can give someone you trust the authority to make medical decisions in your name by using a healthcare proxy.

There are some people who might benefit from a trust as well.

Estate Planning Checklist

Make an inventory.

Your possessions might seem insufficient to justify estate planning, but you may be surprised at just how much you actually have. As such, keeping track of your tangible and intangible assets is easy with an inventory.

Estates may contain tangible assets such as:

- Real estate such as homes, land, or other properties.

- Any type of vehicle, such as a car, motorcycle, or boat.

- Items such as coins, art, antiques, and trading cards that are considered collectibles.

- The rest of your personal belongings.

A person’s estate may contain the following intangible assets:

- Any savings accounts, checking accounts, or certificates of deposit.

- A mutual fund, stock, or bond.

- Workplace retirement plans such as 401(k)s and Individual Retirement Accounts (IRAs).

- Life insurance policy.

- A health savings account.

- An ownership interest in a business.

If you have outstanding liabilities, you should also list them. These are any debts that have not yet been paid in full like mortgages, credit cards, or other debts. If you die, an executor of your estate can notify creditors more easily by keeping a written record of your outstanding debts.

Prepare your estate plan.

Answer these questions about how to settle your affairs before meeting with an estate planning attorney:

- How should your assets be distributed to your heirs?

- If you have minor children, who should care for them?

- What is the cost of caring for and educating your children?

- During an illness or injury, who should manage your financial affairs?

- When it comes to distributing your assets, who should be in charge?

Decide what your directives will be.

Legal directives are an important part of an estate plan. These typically include:

A trust.

Your assets are placed in a trust for your benefit (and that of your beneficiaries) and managed by a trustee. Your trustee can take over if you become incapacitated or ill. When you die, the trust assets are transferred to the beneficiaries of your choice, bypassing probate. Alternatively, you can create an irrevocable trust, which cannot be changed or revoked.

Living wills are also known as medical care directives.

In the event that you become incapable of making medical decisions for yourself, it outlines your wishes for medical care. If you are incapable of making health care decisions, you can also give a trusted person medical power of attorney. Advance health care directives combine these two documents into one.

Power of attorney for financial matters.

When you are medically incapable of managing your financial affairs, someone else can. It is your designated agent’s responsibility to act on your behalf in legal and financial situations when you are unable to do so. In addition to paying bills and taxes, they’ll also be able to access and manage your assets.

Power of attorney with limited authority.

You may benefit from this if you feel uncomfortable about turning everything over to someone else. Your named representative’s powers are limited by this legal document. During the closing of a home sale or when selling a specific stock, you could grant the person authorized to sign the documents on your behalf.

Don’t give your power of attorney to just anyone.

Your financial well-being – or even your life – might be at their disposal. In case your primary choice is unavailable, you might want to assign medical and financial representation to different people.

Almost all states offer standardized forms for medical powers of attorney that can be filled out in the blanks. It is not uncommon for states to provide a form for financial power of attorney, as well as a living will or advanced directive.

Forms generally won’t cost you anything, but notarizing them will. There are different notary fees in different states, ranging from free to $25.

Your beneficiaries need to be reviewed.

Although your will and other documents may outline your wishes, they may not cover everything.

- Keep an eye on your retirement accounts and insurance policies. You need to keep track of beneficiary designations on retirement plans and insurance products. Beneficiary designations usually take precedence over wills.

- Make sure your stuff gets to the right people. The names of beneficiaries on policies and accounts established many years ago are sometimes forgotten. A life insurance policy that has your ex-spouse as a beneficiary, for example, might not pay out to your current spouse after you die.

- Be sure to fill out all beneficiary sections. During probate, an account may be distributed based on the state’s rules for distributing assets.

- Specify contingent beneficiaries. Having backup beneficiaries is essential if you forget to update the primary beneficiary designation and your primary beneficiary dies before you do.

Make sure you know the estate tax laws in your state.

It is often possible to minimize estate and inheritance taxes through estate planning. However, most people will not pay these taxes.

Only estates exceeding a certain amount are subject to estate taxes at the federal level. It generally applies to assets valued over $12.06 million in 2022 or $12.92 million in 2023 and has a tax rate of 18% to 40%. What if your estate exceeds the federal limit? Your heirs may benefit from a grantor-retained annuity trust, also known as a GRAT, which is an irrevocable trust.

Additionally, estate taxes are imposed in some states. If an estate’s value is below the federal government’s exemption amount, then the state may levy an estate tax. There are also inheritance taxes in some states. As a result, those who inherit your money may have to pay taxes

Consider the value of professional assistance.

In general, your situation will determine whether you need to hire an attorney or estate tax professional to help you create your estate plan.

- In the case of small estates and simple wishes, an online or packaged will-writing program may suffice. You will usually be guided through writing a will using an interview process about your life, finances, and other bequests, in accordance with IRS and state requirements. Your homemade will can even be updated as needed. Compared to working with an attorney, online wills are less expensive. With LegalZoom, you can create a simple will for $89, a comprehensive will for $99, and an estate plan package for $249. Nolo’s Quicken WillMaker and Trust lets you create over 35 documents ranges from $89 to $199.

- Getting legal and tax advice may be worthwhile if you have doubts about the process. When you live in a state with its own estate or inheritance taxes, they can help you determine if you’re on the right estate planning track. A will and powers of attorney can cost as little as $1,000. But a complex estate will require you to work with an attorney. The cost of hiring a lawyer can range from $100 per hour to $400 per hour or more.

- An estate attorney or tax professional can assist in navigating the sometimes complicated implications of a large and complex estate – such as childcare concerns, business issues, or non-familial heirs.

Maintain a current estate plan.

Keep your estate plan updated once it has been finalized. According to Bob Carlson, senior contributor to Forbes, paperwork should be reviewed every three to five years. Your estate needs to be reviewed and revised if you experience major life changes, such as:

- When a child is born, adopted, or dies

- Marriage, divorce, or separation

- Whenever you move to a new state

- A major income change has occurred

- Whenever the tax law has been significantly changed

FAQs

1. What is estate planning?

In estate planning, you work with professional advisors who know your goals and concerns, your assets, and how your family works. It might involve lawyers, accountants, financial planners, life insurance advisors, bankers, brokers, and more.

Tax planning may or may not be involved with estate planning, which involves transferring assets at death. Wills are the most common documents associated with this process.

2. Do I have an “estate”?

When someone dies, their estate is everything they own before they’re distributed by will, trust, or intestacy. An estate can have real property, like houses, as well as investment properties. It also includes personal property like bank accounts, stocks, jewelry, and cars.

3. What’s the point of planning?

An estate plan lets you decide who gets what from your estate, and how much. In addition, it prevents taxes from ruining the estate.

4. Is a will necessary?

No. Wills aren’t required by law. However, most people should make a plan for how their finances and property will be divided after they die.

For starters, you can control how your assets are distributed when you die by making a will. In the event you pass away without a will, you won’t be able to choose what happens to your stuff. Your will lets you decide who gets what, or whether certain people aren’t allowed to get anything. This is called disinheriting an heir. In many cases, naming the person who will wind up your affairs makes all the difference in how smoothly things go. Knowing they’ve picked someone they trust to handle their final affairs gives people peace of mind when they make a will.

Also, in an unfortunate scenario where you pass away while your children are still minors, a will lets you plan for their care. Plus, a will can save your heirs the trouble of going through probate. You can also avoid estate taxes by making a will. Your beneficiaries and heirs won’t have to pay estate taxes on the amounts you left them.

Wills aren’t permanent, so you can change them anytime. In case you decide to divide your estate differently later, you can make any adjustments you need.

5, What happens if I don’t have a will?

Without a will, your property passes according to state law, regardless of what you want. A person dying intestate means they die without a legal Will, and intestacy is what happens to their estate without one.

In most cases, the estate of a married person who dies with a spouse still alive goes to the spouse. If you don’t plan ahead, your surviving spouse can use your assets, savings, and retirement to support his or her new family.

A person’s spouse and children from a previous relationship are usually exceptions. A surviving spouse usually gets one-third of the estate if there’s no Will, and two-thirds goes to the children. Wills are needed if a person wants their assets disposed of differently than by statute. You can add a lot of stress and expense to an already emotional and difficult situation when you die without a will.

The good news? Wills don’t have to be complicated or expensive.

[Related: The Role of Real Estate in Your Retirement Planning]