The payment industry is rapidly evolving and transitioning from a cash-based world to a cashless one. As we shift to an increasingly digital world, here’s a closer look at the current state of the merchant payment processing industry and what to expect in the near-future.

Current Processing Methods

Gone are the days of merchants only accepting cash, checks, or swiping credit cards and then having to wait days, sometimes weeks, for the funds to become available in your account. Additionally, these traditional payment processing methods came with additional fees, such as processing fees or leasing equipment.

Processing payments have become increasingly convenient, for both the merchant and customer and affordable – especially if you accept global payments.

With that in mind, here are the most common processing methods for merchants:

Point-of-sale (POS) Credit Card Processing

These are the terminals that allow customers to make credit card payments. This processing method is commonly associated with traditional retail and countertop card machines. However, as we’ll discuss shortly, are being updated in order to be compatible with EMV and mobile payments.

Credit Card Swipers or Readers

These are small electronic devices that read the customer’s account information that has been embedded inside the magnetic stripe of cards.

This is typically used for in-person transactions. Thanks to companies like Square, PayPal, and QuickBooks GoPayment, merchants can attach a read to their mobile devices in order to process payments wherever they are. You don’t have to purchase equipment and processing fees are typically favorable. Square, for example, charges 2.75 percent and 3.5 percent + $0.15 for manually entering credit card transactions.

EMV Chip Readers

EMV (Europay, MasterCard, and Visa) standard was implemented to increase the security of physical credit card payments through the use of a chip that has been embedded into customers’ cards. While retailers haven’t 100 percent moved to EMV, since the EMV Liability Shift in 2015, EMV usage is expected rise in 2017. (The fact the businesses will be charged a fee if they don’t change to the chip method of payments, is driving this change.)

According to Business Insider;

Merchant adoption continues to rise, though it’s slowing — 1.75 million Visa merchants now accept chip cards, up by 110,000 since the previous quarter and over 1 million since last November. That’s still just 38 percent of US storefronts, but represents a significant figure of transaction volume because most major merchants accept EMV cards.

As more small businesses warm to the idea of EMV and upgrade their readers, likely because of the fraud protection benefits they can reap, it’s likely this figure will continue to rise steadily.

However, Visa and other networks recently delayed the migration for gas stations, somewhere that cards are used regularly and locations that see high fraud, by three years, which could continue to impact merchant upgrades.

Mobile Payment Processing

As mentioned above, mobile POS devices have allowed merchants to leave their traditional POS systems behind so that they can complete transactions wherever they like, particularly for food truck owners or merchants at farmer’s markets. Additionally, mobile payment processing can is also beneficial to brick-and-mortar merchants thanks to NFC technology.

“The growing use of NFC technology and digital wallets among consumers will continue in 2017,” writes Scott Blum, Vice President and Lead Business Development, Marketing, and Integrated Payments at Total Merchant Services.

“Most major players in the mobile device industry have delivered their own versions of the digital (or mobile) wallet (e.g. Apple Pay, Android Pay and Samsung Pay). With Apple Pay reporting a growth of one million new users per week, there are strong signs that many consumers prefer this method of payment,” adds Blum. “Digital wallets are quickly becoming the norm, particularly among millennials. Because digital wallet payments are faster than using EMV or traditional swipe credit cards, users are quickly converted and want their purchases to be seamless and fast wherever they go. This demand for digital wallets will significantly impact the way small business merchants provide payment services in 2017.”

In fact, the mobile POS market is expected to increase by a staggering 400 percent by 2019.

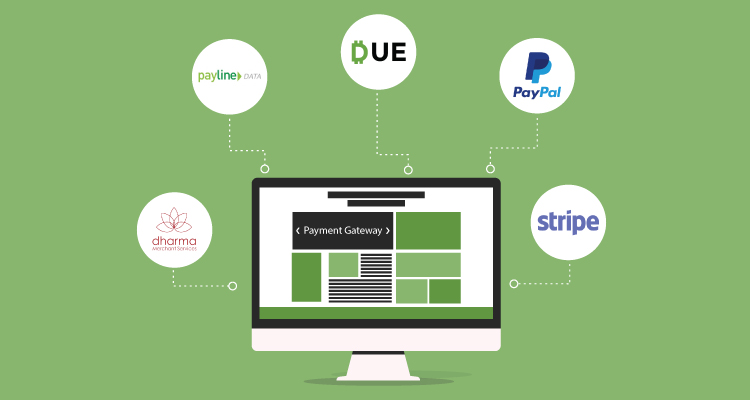

Payment Gateway

If you accept payments online, then a payment gateway, such as Due, PayPal, Dharma Merchant Services, Stripe, Payline Data, and Authorize.net, have become a necessity.

By using a payment application on your website, customers can securely and quickly enter their payment information to complete a transaction. Most gateways APIs allow a one-click checkout for customers and charge a 2.9 percent + $0.30 transaction fee. Even more promising, some payment gateways can be customized to fit the preferences of your customers. For instance, Stripe has released Relay that allows customers to shop on Twitter without being redirected to another page.

Virtual Terminals

Virtual terminals are basically an online version of a traditional POS system and are important for small businesses like mail-order telephone merchants and at-home workers. Unlike payment gateways that process the payment for you, virtual terminals allow merchants to process the payment themselves. There’s no expensive hardware or software to purchase either.

As with payment gateways, you’ll have to create a merchant account. Many payment gateways also feature virtual terminals, but other suggested virtual terminals would be from Host Merchant Services and CDGCommerce.

ACH

Merchants can also choose to process eChecks by using the Automated Clearing House. Previously, it took several days to process eChecks, but NACHA has adopted a rule for same-day ACH. Companies like Dwolla have an innovative API that allows affordable, ubiquitous, and instant ACH transactions.

eCash

One of the most exciting payment trends is eCash, such as bitcoin. Electronic cash eliminates the middleman which means that transaction fees are inexpensive and occur in real-time. It’s perfect for businesses that rely on smaller transactions since fees are only $0.10 or $0.30 for visits or certain small actions and merchants involved in the global economy due to the elimination of exchange rates.

Furthermore, eCash can reduce fraud and chargebacks. Companies like Coinbase allows merchants to start accepting bitcoin.

Fintech Innovations

It’s anticipated that by 2025, 75 percent of all transactions will be made without cash. As Sandra Wrobel-Konior, content marketing manager at SecurionPay, writes, “Consumers around the world understand the benefits of mobile payments” and expect the checkout process to be easy, convenient, made with one-click, and user-friendly. Unfortunately, “many retailers are not prepared to provide mobile users with high quality and well-designed websites or apps.”

“FinTech solutions are here to answer online retailers and customers’ needs. Innovation brings enormous changes and lots of benefits for both merchants and customers,” says Wrobel-Konior.

“We can observe the growing number of innovations in mobile payments. For instance, MasterCard recently launched a program that replaces passwords with selfies. It’s a biometric authentication app which asks a customer to scan his face to pay. The company also announced testing other authentication methods, such as facial identification, voice recognition, and cardiac rhythm.”

Due’s Miranda Marquit suggests that with FinTech business owners can start accepting electronic and blockchain payments, as well as manage your compliance – which ultimately will make processing payments more convenient and affordable.

Improved Security Measures and Authentication

Security is one of the main obstacles to overcome when processing payments – for both merchants and customers. Because of this, the payment industry is most anxious to improve security measures and authentication. “Security practices that rely on knowledge-based authentication are rapidly weakening and data breaches are increasing.

We predict there will be more than one billion consumer records breached in 2017—finally causing many companies to abandon the password for good,” reported Kalle Marsal, CMO of Mitek Systems, an organization that focuses on identity verification.

“Recent research shows that there is an enormous unmet demand among Millennials for using selfies in mobile commerce. We predict that more than $3 billion in mobile commerce transactions during 2017 will incorporate selfies for authorization or authentication,” adds Marsel.

Security measures, such as advancements in authentication that use biometrics and being PCI compliant, will continue to be important for merchants that process payments. In order to make customers feel safe when making a purchase, merchants should be willing to embrace these technological advancements that can thwart any possible data breaches.

Level 4 Merchant PCI Compliance

Speaking of PCI compliance, Visa has found that small businesses are the most at risk when it comes to data breaches. Because of this, Visa has revised the guidelines for Level 4 merchants, which are businesses that process less than 20,000 Visa or Mastercard e-commerce transactions annually.

Effective January 31, 2017, all Level 4 merchants may only use PCI-certified qualified integrators and resellers (QIRs) and conduct annual PCI compliance assessments, unless they are participating in Visa’s Technology Innovation Program (TIP).

The Future of Merchant Processing

Make no mistake about it. Speed, efficiency, and security are where the future of merchant processing is heading. Because of this consumers are opting to use cashless payments, such as Apple Pay, Samsung, and retailer wallets like Walmart Pay.

In fact, BI Intelligence, “estimates that the online processing market in the U.S. will be worth approximately $10.7 billion in 2016 and will grow to $17.5 billion in 2020 as online shopping becomes more common.” Additionally, “more than half of the U.S. population will at least try a mobile wallet by 2020.”

“As a result, more merchants would need to invest in mobile wallet readers, even inside their brick-and-mortar stores. As consumers more frequently expect rapid payment processing, merchants will need to meet that desire or risk losing their customers to other stores that do.”