Things in the blockchain space continue to develop. There’s a lot of excitement when it comes to blockchain applications. The government has been funding blockchain technology projects.

Entrepreneurs, crypto-anarchists, and major companies are all looking to blockchain applications. In fact, blockchain, which is the technology that underpins the increasingly popular Bitcoin, is approaching critical mass in terms of recognition in the mainstream.

A couple of interesting developments related to blockchain applications include the development of smart insurance and of initial coin offerings (ICOs).

The interest in blockchain technology and the fascination with cryptocurrencies are fueling new ways of doing things.

Table of Contents

ToggleSmart Insurance: IBM and AIG Create the First Blockchain-Based Multinational Insurance Policy

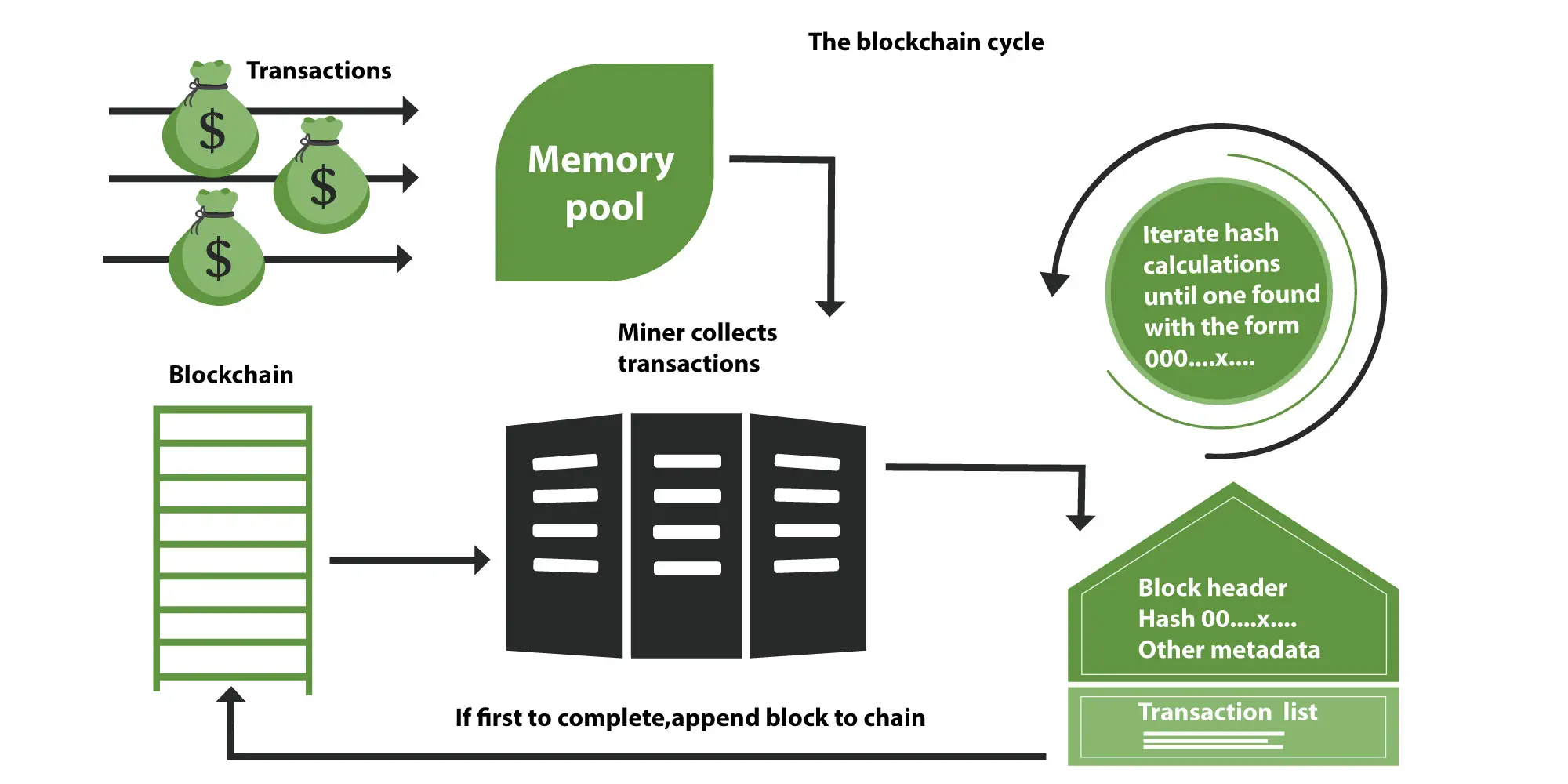

One of the most interesting uses for blockchain applications is the smart contract. With a smart contract, it’s possible to have an automatically enforced contract. When terms are fulfilled, the contract takes care of itself.

The hope is that smart contracts can help streamline transactions, as well as make the secure. Due to the public (or private) distributed ledger model, everyone can see the terms and watch to see them fulfilled.

Smart contracts could be very interesting in the insurance industry, since insurance policies are basically types of contracts. Insurance industry giant AIG is proving this thesis with its latest venture, a multinational insurance policy to Standard Chartered, according to the Financial Times.

Working with IBM’s blockchain division, AIG put together a multinational insurance policy that would be valid across borders. The policy for Standard Chartered is based in the U.K., but includes policies in the U.S., Kenya, and Singapore.

Master policy and local policies

One of the difficulties with issuing multinational insurance policies has to do with the fact that each country has its own laws and regulations regarding insurance contracts. That means that it can take months to put together an appropriate policy. There’s a lot of checking and traditional methods can be slow.

Using blockchain applications, though, it was possible for AIG and IBM to create the Standard Chartered multination policy in a matter of days.

In order to make it work, says the Financial Times, AIG first put together a master policy in the U.K. Next, local policies were added for the individual countries involved. Using blockchain technology, it is possible for everyone involved to see policy terms, premium information, and claims.

Being able to keep track of everything using blockchain technology means that it’s easy to just see what’s happening with the master policy and the related local policies in real time. No need for emails back and forth and processing transactions using older, slower methods.

If the Standard Chartered policy remains effective, there’s a good chance that more insurance companies will begin adopting blockchain technology. Even with more traditional insurance policies that don’t span multiple countries, smart contracts can help improve the insurance industry.

Initial Coin Offerings (ICOs)

The fintech world is enamored of tokens and cryptocurrencies right now. And it’s not just about the technology side. Bitcoin keeps rising in price. As of this writing, Bitcoin is worth more than $2,000.

Speculators love the idea of investing in cryptocurrencies, and Bitcoin isn’t the only currency benefiting from this interest. Now, though, it’s gone beyond just investing in cryptocurrencies and hoping to cash out later for much more. Some companies are using initial coin offerings to raise money with cryptocurrencies, according to Reuters.

The idea is to encourage investors to purchase tokens that would be used to spur innovation with a tech company or in some other company developing blockchain applications. The company would raise capital, and the investor would receive tokens in exchange for the investment. Later, an investor might be able to return the tokens for a stake in the company or some other type of benefit.

How ICOs work

According to Reuters, companies might want to develop some sort of blockchain application that is meant to make improvements to a system. It could be about improving payment processes, upgrading security, or doing any number of things. The company looking to develop the solution might need cash to make it happen.

The company decides to hold an ICO. Investors can hand over capital and receive tokens in return. These tokens are supposed to be redeemed for cash later on, after the successful completion of the project. In some cases, the tokens could be used to buy an ownership stake in a company. The idea is that the investor receives a benefit down the road, assuming the blockchain (or other) project is successful and profitable. It all depends on the structure of the deal.

However, it’s important to realize that buying tokens through an ICO doesn’t actually mean that you have ownership in the company. It’s not the same as buying stock. Instead, it’s more like the crowdfunding efforts seen in the past. You hope the project is successful and makes money so that you can turn in your tokens for a better return.

In some cases the tokens issued can actually be sold on an exchange — before the project is finished. The company holding the ICO can list its token on one of the crytpocurrency exchanges around the world. These tokens then can rise and fall in value along with cryptocurrencies like Bitcoin, Dash, Ethereum, Litecoin, and others.

If you don’t want to wait to see the end of the project, you can see if you can get money for your tokens on an exchange. Speculators are using this as a way to make money, regardless of the success of the original venture.

Regulation and ICOs

For now, ICOs are attractive to many fintech companies and other innovators because there is less regulation by the Securities and Exchange Commission (SEC). In fact, since these aren’t stock offerings, there are less stringent rules about listing. On top of that, says Reuters, some opponents point out that there is often less transparency in ICOs than in stock IPOs.

Going through with a stock IPO requires a great deal of regulation and planning. There’s a lot of reporting that goes into it. ICOs aren’t nearly so onerous.

However, that might be changing. Reuters reports that the SEC is looking into ICOs. The reason is that there are many complexities in these deals. As a result, some speculators might not have the technical expertise needed to properly evaluate an ICO. It’s not just about having good investment instincts. ICO investors also need to understand blockchain, cryptocurrencies, and how they work.

For those who do understand how to evaluate ICO deals, they can turn out to be quite lucrative.

Bottom Line: New Blockchain Applications Every Day

Every day it seems as though there are new blockchain applications. Whether or not blockchain really will completely change things forever, it is certainly making a splash right now.

With insurance contracts becoming one of the next major industry applications, smart contracts fueled by blockchain are moving into the mainstream. Other companies, beyond AIG, are likely to get in the game if things go smoothly with this first multinational contract.

And, of course, if ICOs start getting a little more play, it’s possible that cryptocurrencies and blockchain will become increasingly popular and seen as viable investments for a variety of uses.