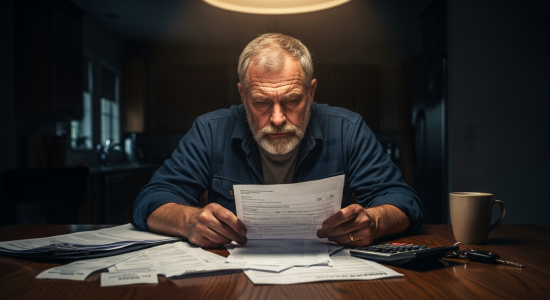

There’s more to money than numbers on a bank statement; it’s tied to peace of mind, freedom, and security. So, when you experience financial instability or uncertainty, it is no surprise that there will be negative effects on your mental health.

The effects of financial stress start with your wallet, but spread to other areas, such as your emotions, relationships, sleep, performance at work, and even your health. But the good news? You aren’t powerless. By adopting the right mindset and tools, you can relieve that stress and reclaim control over your finances and well-being.

Table of Contents

ToggleThe Deep Connection Between Money and Mental Health

Financial stress is extremely common. Since the American Psychological Association’s first “Stress in America” survey in 2007, money has consistently ranked among the top stressors for Americans. A Capital One CreditWise survey also found that 73% of Americans rank their finances as the top stressor in their lives.

Anxiety, depression, and burnout can result from financial pressure, whether it’s debt or living paycheck to paycheck. As such, stress can manifest in a variety of ways;

- A constant worry about bills, expenses, or job security.

- Sleep disturbances or restlessness.

- Short temper or irritability, especially when discussing money.

- Having feelings of guilt or shame as a result of debt or spending.

- Being unable to participate in social activities or with friends because of financial difficulties.

- Money-related panic attacks or anxiety attacks.

If left untreated, these symptoms can compound, making it even harder to make good financial choices or seek assistance. Managing your finances gets harder when you are stressed about money, and more stress fuels the cycle.

Who Is Most Affected?

Financial stress can affect anyone, but certain groups in society are particularly vulnerable;

- Households with low incomes who struggle to cover basic needs, such as food, rent, and health care.

- Young adults struggle with student loans, rising rent, and an uncertain job market.

- A parent who must balance raising his or her children with saving for college and retirement.

- The elderly, especially those without enough savings for retirement.

- Chronically ill or disabled people may face high medical costs and limited earning potential.

However, it is important to remember that even those with relatively stable incomes are not immune. The sudden loss of a job, unexpected expense, or downturn in the market can shake even the most well-built financial plan.

The Physical Toll of Financial Worry

The consequences of chronic financial stress extend beyond an unsettling feeling to your physical health. Long-term financial stress is strongly linked to;

- An increased risk of mental health disorders. A greater susceptibility to depression as well as anxiety disorders.

- Cardiovascular concerns. An increased risk of heart disease and high blood pressure.

- Unhealthy coping mechanisms. As a result of overwhelming stress, there is a greater likelihood of turning to substance abuse or other detrimental behaviors.

- Compromised immunity. The body is more vulnerable to illness due to a weakened immune system.

- Cognitive overload. An impaired cognitive function, resulting in problems with concentration, decision-making, and problem-solving.

Ultimately, financial worries can profoundly impact our overall well-being, impacting all aspects of our lives.

Taking Back Control: Practical Steps to Protect Your Mental Health

When faced with financial stress, it’s important to remember that you have the power to handle it. Even if you can’t magically improve your financial situation overnight, you can take concrete steps to alleviate the mental burden as you work towards greater financial stability. To guide you, here is a roadmap;

1. Acknowledge your feelings without self-condemnation.

First and foremost, you must recognize and validate your emotions without judgment. Money struggles are a reality for many people, but they don’t constitute failure. If you feel overwhelmed by the sheer financial pressure, identify which specific emotions you are dealing with. Do you feel shame or guilt about past financial decisions? Does fear of an uncertain financial future plague you?

By being honest with yourself about your emotions without self-criticism, you can prevent suppressing your feelings or turning to unhealthy coping mechanisms. Acknowledging this can lead to proactive steps rather than continuing to feel shame or denial.

2. Prepare a simple, clear snapshot of your finances.

The fear of the unknown contributes significantly to financial stress. As a result, you often fill in the gaps in your mind with worst-case scenarios, which are frequently much worse than reality. To counter this, you should develop a clear and concise picture of your current financial situation;

- Know your debts. How much do you owe, including credit cards, loans, and other debts?

- Track your outflows. Besides rent and mortgage, how much does food and transportation cost you each month?

- Understand your income. After taxes and deductions, what is your consistent income?

- Identify potential cuts. Do you have any recurring expenses or subscriptions that you could eliminate or reduce?

You can organize this information using a simple spreadsheet, a budgeting application, or a notebook. While gaining clarity may not instantly solve your financial challenges, it will give you peace of mind and a solid foundation.

3. Set small, achievable goals.

A complete overhaul of your financial life can cause further stress. Instead, set small, realistic goals that provide a sense of accomplishment;

- A tiny triumph. Save a modest amount every week, even if it’s just $10.

- Diminishing your debt. Aim to pay an amount slightly higher than the minimum due on at least one of your credit cards.

- Victory at home. Instead of ordering takeout every week, cook one extra meal at home.

- Subscription salvation. You can cancel if you rarely or no longer use a digital subscription or service. Subscription management tools like Rocket Money and Trim can discover and cancel these subscriptions on your behalf.

Even seemingly insignificant victories contribute to rebuilding your sense of agency and slowly chipping away at the overwhelming sense of helplessness.

4. Build a budget that works with your life, not against it.

Budgets are often associated with negative connotations, such as being restrictive and guilt-inducing. However, when used effectively, a budget can be a powerful tool for reducing stress and providing a proactive way to allocate your money.

You should create a budget that reflects your actual spending habits while allowing some flexibility and small pleasures. Consider using the 50/30/20 rule as a general guideline: allocate 50% of your income after taxes to essential needs, 30% to wants, and 20% to savings and debt repayment.

You may need to adjust these percentages depending on your current financial situation. You want to achieve clarity, make conscious spending choices, and track your progress, not rigid perfection.

5. Contact someone you trust and lean on your support system.

Often, financial stress breeds isolation, making you feel like you’re alone in these turbulent waters. Keep in mind, however, that you are not. Sharing your burdens with someone you trust can be incredibly cathartic and healing. If you are struggling with a financial problem, contact a trusted friend, a qualified therapist, or a compassionate financial coach.

If you’re in a committed relationship, financial silence can breed resentment. Discussing your shared finances with honesty and respect can strengthen your relationship.

6. Practice mindfulness to cultivate present moment awareness.

Often, financial stress hijacks your thinking, pulling you into a cycle of anxiety or worry about the past. Practices such as deep breathing, meditation, or simply walking mindfully in nature can anchor you in the present moment and stop negative thoughts from spiraling out of control.

As soon as feelings of financial stress begin to surface, try this simple grounding exercise:

- A four-count breath. For a count of four, breathe deeply through your nose.

- Pause gently. Hold your breath for four counts.

- Slow release. For a count of four, exhale slowly through your mouth.

- Repeat. Repeat this breathing pattern a few times.

By engaging your senses, you can further anchor yourself in the present by naming;

- Five things you can see around you.

- Four things you can physically touch.

- Three things you can hear.

- Two things you can smell.

- One thing you can taste.

This simple exercise can bring your brain back to reality during a panic attack.

7. Take on a side hustle or volunteer role to explore new avenues.

Financial stress can be significantly exacerbated by job loss or underemployment. To mitigate this impact, you can actively seek ways to utilize your existing skills and talents. By pursuing a paid side hustle or volunteering for a cause that provides purpose and structure, you can gain a renewed sense of direction and a path forward.

In addition to boosting your self-confidence, these endeavors can often lead to new and unexpected opportunities.

8. Develop a strategy to reduce debt.

Having debt can leave you feeling drained, particularly when it seems an insurmountable obstacle. Not only should you prioritize debt reduction within your overall financial plan, but you should also try to alleviate the emotional burden it carries.

Consider consolidating your debts if you manage multiple debt payments with varying interest rates to simplify your finances. A few examples are;

- Leveraging home equity. Home equity lines of credit (HELOCs) are sometimes used to consolidate high-interest credit card debt into a single, possibly lower-interest payment.

- Streamlining student loans. Refinancing your student loans could provide a lower overall interest rate by combining several individual loans into one.

Various debt consolidation options are available to you, but not all are suitable for every individual. In addition to potentially reducing your monthly stress, exploring these avenues may also allow you to conserve money on interest in the long run.

9. Seek professional guidance if you need it.

If you feel overwhelmed by your financial situation, don’t hesitate to seek professional assistance. Feel free to contact;

- A reputable financial counselor. Using their guidance, you can create a sustainable financial plan, manage debt, and budget without judgment. You can find cheap or free credit counseling services through non-profit organizations like the National Foundation for Credit Counseling (NFCC).

- A qualified therapist or mental health professional. This is particularly true if your financial stress is severe, persistent, or significantly impacts your daily life. Ideally, choose a therapist with experience working with financial trauma or anxiety related to money.

- Valuable community resources. In many communities, free financial literacy workshops are offered, as well as job search assistance programs and emergency financial assistance. When you recognize you need support, taking advantage of available resources is a smart and proactive step.

10. Acknowledge and celebrate victories that are not financial.

Every step forward you take in managing financial stress will not be reflected in your bank account balance. Were you able to take a few deep breaths before checking your account? Have you and your partner discussed your shared debt honestly and openly? Could you resist an impulsive purchase that would have added to your stress? All of these are positive signs.

You reinforce positive momentum and build resilience by consciously celebrating emotional and behavioral victories, not just tangible financial ones. Even if your overall financial situation is still a work in progress, this can keep you motivated and hopeful.

Final Thoughts: You’re More Than Your Bank Balance

While financial stress can be brutal, it does not define your worth. Rather than being a sentence, it’s a signal. When you feel out of control with your money, it’s easy to feel out of control with yourself. The truth is, you have more power than you realize.

Addressing the numbers and the emotions behind them can begin to relieve the pressure. By creating space, you can breathe, plan, and heal. Additionally, you’ll improve your mental health, quality of life, and financial situation.

Remember, it’s all about taking small steps at a time. You will thank yourself in the future.

FAQs

How are financial stress and mental health connected?

The body reacts to financial stress with a cascade of psychological and emotional effects. Having persistent financial worries can lead to anxiety, depression, low self-esteem, irritability, and difficulty sleeping. In addition, it can worsen mental health conditions that already exist.

Can worrying about money actually make me depressed or anxious?

Yes. As a result of chronic financial stress, anxiety and depression are exacerbated by prolonged worry and uncertainty. If you cannot secure your future or meet your financial obligations, you can feel hopeless and despair.

Are there specific financial situations that are more likely to cause mental health issues

Although any financial worry can be stressful, job loss, significant debt, unexpected expenses, housing insecurity, and inability to afford basic needs are particularly potent triggers for mental health issues. There is also widespread financial stress due to the rising cost of living and economic instability.

Is the impact of financial stress on mental health the same for everyone?

No. Many factors can influence how significantly an individual’s mental health is affected, including financial stress, mental health conditions, social support, income level, and access to resources.

When should I seek professional help for financial stress?

It might be a good idea to seek professional assistance if;

- You are constantly worried about your finances.

- Anxiety, depression, or other mental health symptoms are significant for you.

- Financial stress can negatively impact daily functioning (work, relationships, sleep).

- You’re using unhealthy coping mechanisms like substance abuse to cope.

- You are thinking about harming yourself.

Image Credit: Andrea Piacquadio; Pexels