Imagine waking up one day and realizing that $612,025 has been stolen from you.

Ouch. That’s not just a “rounding error.” That is a house, a retirement fund, and life-changing wealth that just evaporated because of one wrong decision made back in your 20s or 30s.

Let me give you an example. I was once contacted by a 28-year-old subscriber who shared details of his financial plan, and I felt the “Hulk Smash” bubbling up. Why? He was sold a life insurance policy with a $200,000 face value at a $164 monthly cost.

To put that in perspective, I have a $2.5 million term policy, and he pays more for his tiny policy than I do. If his policy doesn’t include a daily Swedish massage and a personal concierge, he’s been ripped off.

Let’s break down how these “advisors” lure you in and how much they really cost.

The Deceptive Pitch: “It’s Like a High-Yield Savings Account!”

It was promised to this young man that after four years, this policy would magically become a high-yield savings account (HYSA) with a 4.5% dividend yield. This is the classic insurance sales pitch, and it is arguably the most misleading comparison in finance. It’s also the reason I’ve recorded videos titled “7 Financial Advisors Want to Punch in the Face.”

Why whole life is NOT a savings account.

- The “gatekeeper” fee. When you put $1,000 in a real HYSA, you have $1,000 the next day. In a whole life policy, the “cash value” is usually zero the first year. Why? The first year of payments goes to the agent’s commission and overhead.

- Liquidity vs. borrowing. With a savings account, the money is yours. You don’t “withdraw” money from a whole life policy; you borrow it. To access your own funds, you must pay interest to the insurance company.

- The dividend shell game. Every dollar you deposit with a bank earns interest. Insurers, however, pay dividends only on the cash value, which is the small amount left over after insurance costs, fees, and commissions are deducted.

The Conflict of Interest: Follow the Money

Why would an advisor sell a 28-year-old single man without children a whole life policy rather than a less expensive term policy? It’s simple math:

- Whole Life Commission. Typically, 60% to 100% of the first year’s premiums are covered (roughly $1,800 to $2,000 in this case).

- Term Life Commission. It usually costs a fraction of that (roughly $200 to $400).

Ultimately, he didn’t pick it because it was best for the client; he picked it because it paid 10x more.

The Math Doesn’t Lie: Whole Life vs. Reality

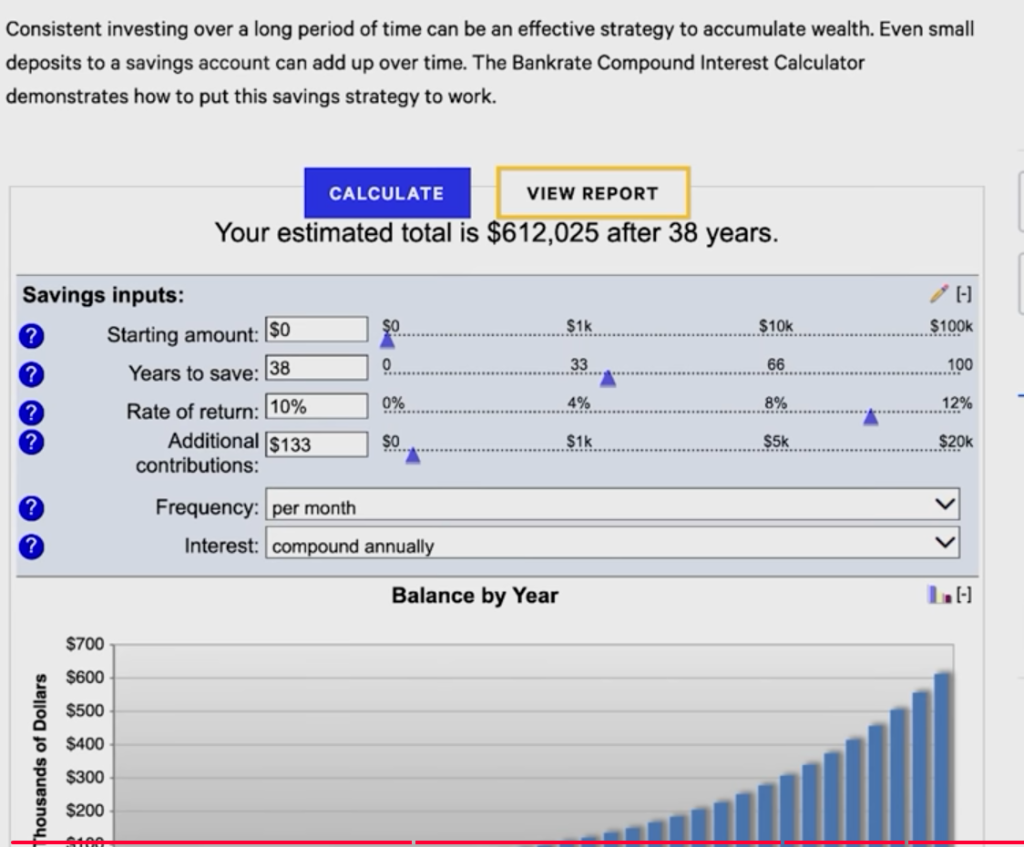

I pulled the actual illustration for this young man. He’d have $71,711 in cash value if he kept this policy for 38 years (until he’s 66).

Now, let’s look at a basic future value calculator. After 38 years, you should have $193,000 if you invested $164 per month in an account earning a modest 4.5% annual rate.

Where did the other $121,289 go? It went to the insurance company. For the sake of “managing” the account, they kept more than 60% of his potential gains.

The Wealth Hacker Strategy: Buy Term and Invest the Difference

Here’s where the $612,025 difference comes from. Regardless of the decade, this strategy works.

- Get a term policy. It costs about $31 a month for a healthy young adult to get a $200,000 term policy.

- Invest the savings. As a result, $133 a month is available for other investments ($164 – $31).

Do you know what he will have after 38 years if he invests that $133 in a Roth IRA, 401 (k), or a diversified index fund earning 10%? $612,025.

By choosing the “high-yield savings” pitch, he hands over $600,000 to an insurance company. Even at an 8% rate of return, he’d still have $366,000, nearly $300,000 more than a whole life policy offers.

How to Protect Yourself from the Scam

If you are sitting across from a “financial professional” and they begin using these red-flag phrases, run!

- “Be your own bank.”

- “Infinite banking.”

- “Tax-free retirement vehicle” (referring to an insurance product).

In most cases, these agents are licensed only to sell life insurance; they aren’t even licensed to sell securities like stocks and bonds.

My Final Advice

You may not even need life insurance if you’re young, single, and have no dependents. Get a cheap term policy if you want to be safe. Investments are for wealth; life insurance is for protection. You should never mix the two.

Don’t be fooled by a “guaranteed” dividend. You are being robbed of your future million dollars. It’s your money, it’s your life, and you alone can make it awesome.

Stop getting ripped off. Start hacking your wealth.

Disclaimer: I’m a guy on the internet who wants you to be rich. I want ALL of us to do better financially, expecially in our side-hustles. I know I’ve been lucky, and I’m grateful–but I hope you will be lucky too!

Talk to a fee-only fiduciary advisor who doesn’t earn commissions from the products they recommend.

FAQs

1. Is Whole Life insurance ever a good idea?

For 99% of people, the answer is no. Typically, it’s useful for ultra-high-net-worth individuals (estates worth $13 million or more) who need specialized estate tax planning. Compared with a simple term policy and an index fund, it’s overpriced and underperforms.

2. What should I do if I already have a Whole Life policy?

Don’t panic, but do a needs analysis. Find out how much your cash surrender value is. It’s often better to stop the bleeding by switching to a term policy. If you wish to cancel, however, you should first contact a fee-only fiduciary advisor to ensure you have new coverage in place.

3. Can I really get a 10% return in the market?

Over long periods (before inflation), the S&P 500 has historically provided an average annual return of about 10%. Even with a conservative 7% or 8% rate, the math still heavily favors “buying term and investing the difference” over whole life insurance.

4. Why does my advisor insist that Whole Life is better?

Verify their license. Often, insurance agents are called “advisors.” That’s because they are qualified to sell the only product that has an investment component, and it pays huge commissions, too.

If you want to know whether they are registered to sell securities (stocks/bonds) or only insurance, you can use FINRA’s BrokerCheck tool.

5. What happens to the cash value when I die?

This is the kicker: In most whole life policies, the insurance company keeps the cash value when you die. Beneficiaries receive only the face value (the death benefit). It took you years to “save” that money, but you can’t take it with you, and your family does not benefit from it either.

Image Credit: Vlad Deep; Pexels