Now that we are in a new year, should you still be trying to max out your 2020 retirement account? Or should you just move on to the year we are in, and start your 2021 contributions? This is one of the big questions new investors have, especially at the start of the year.

If you are new to investing, the deadline for putting money into your IRA (Individual Retirement Account) might come as a surprise. You actually have until Tax Day, normally April 15th, to fund your IRAs for the prior year. If the 15th falls on a weekend, the deadline will be on the following Monday. This means you technically have 15.5 months to make contributions for any given year!

So while we are straddling two years for possible retirement contributions, you need to decide… Is your money going towards 2020, or 2021?

What are the IRA contribution limits?

Before you decide on maxing out your 2020 retirement account, you should know the limits. The dollar amount you can contribute varies by account. The limits increase every few years to keep up with inflation. Make sure you stay on top of future changes!

2020 and 2021 Roth and Traditional IRA

Both of these accounts have the same limit and did not see a change from 2020 to 2021. You can contribute up to $6,000 per year or $7,000 per year if you are over age 50. You will see this extra “catch-up” amount on many accounts for those over age 50. If you are fast approaching retirement and behind on savings, take advantage of the extra savings! The more money you can squeeze into these tax-advantaged accounts, the better!

Keep in mind, this $6,000 or $7,000 limit is for these accounts- COMBINED! You cannot put $6,000 or $7,000 in each! Maxing out both a Roth and Traditional for the same year is a no-no! You can contribute the full amount to one account or the other, or you can split it up. As long as your combined annual contributions do not exceed $6,000 (or $7,000) you are within the limit.

Making a goal of maxing out your Roth or traditional IRA every year is a great way to boost your retirement savings!

2020 and 2021 SEP IRA

This is an IRA designed for those with self-employed income, and it has a much higher contribution limit. You can contribute up to 25% of your self-employed income. The maximum annual amount is $57,000 for 2020 and $58,000 for 2021.

The key thing to note for SEP IRA’s is the “up to 25%”. This is the guideline you will want to be following, not the dollar amount! This means to max out your SEP IRA for 2021 your net self-employed income for the year needs to be $232,000 or higher.

SEP IRA’s are ideal for those without employees. If you have employees, make sure you understand the contribution requirements for your eligible employees before you move money into your own account.

2020 and 2021 SIMPLE IRA

This IRA might not be as common as the ones above, but it’s still a great place to be saving. SIMPLE IRAs are set up by self-employed individuals or small businesses that have less than 100 employees. Unlike the SEP IRA, where all contributions must come from the employer, the SIMPLE IRA also allows contributions from employees.

The limit for employee contributions to a SIMPLE IRA is $13,500 for both 2020 and 2021. However, employee contributions need to be made within the calendar year! If you are an employee and saving in a SIMPLE IRA, your contributions should now be for 2021.

Employer contributions do NOT count towards that limit! Employers can also make contributions for their employees up until Tax Day, or April 15th.

401k and 403b

These accounts can no longer be funded by employees for 2020! Since these are set up by an employer, they typically operate on a calendar-year basis. All contributions into these accounts now will be for 2021!

That being said, these are still great accounts to save in. When offered a 401k or 403b through work, definitely consider taking advantage of this way to save. The limits for 2021 are $19,500 or $26,000 if you are over age 50.

Now that you know how much you can put in, let’s look at the pros and cons of catching up on 2020 contributions.

The pros of maxing out retirement accounts for 2020

If there is a generous timeline given for making contributions, my first thought is “use them!”. If this April deadline means you are able to max out your 2020 retirement accounts, definitely take advantage of it. Here are some perks of continuing to put away money for 2020.

More money invested

The main perk of setting your contributions for the prior year for as long as you can is that you can get more money into your account. Plain and simple. Once the deadline passes, it’s gone. Is your goal is to be saving as much as possible? If you did not yet max out your 2020 accounts, you should file your incoming investments under 2020!

Even if you think you will not be maxing out the current year, you never know. First, make it a goal to get as much money inside your account as you can for 2020. After the April 15th deadline closes, switch to 2021 contributions. You can still set a goal to max out your account for 2021!

Since the deadline for IRA contributions is always Tax Day, you still have a full year to contribute for 2021. Taking advantage of this deadline helps guarantee you are not missing out on potential money inside your account!

Max out retirement accounts to lower your 2020 taxes

This perk does NOT apply to Roth IRA contributions! Roth contributions are not tax-deductible. Contributions to a traditional, SEP, or SIMPLE IRA though, ARE tax-deductible!

Over the next couple of months, you will be getting tax papers in the mail. You’ll also probably be getting ready to file taxes. If you think you will owe taxes this year, contributions to a tax-deductible retirement account can help lower your tax bill. Since contributions directly lower your taxable income, dollar for dollar, they also help shrink the amount you will owe in taxes!

Make sure to abide by any rules if you plan on contributing to a traditional IRA and have access to a 401k or 403b through work. If you are over a certain threshold, your contributions might not be deductible! Those who do not have access to an employer-sponsored plan (401k or 403b) do not have to worry about this rule.

Investing a lump-sum

The time when we are straddling years for retirement account contributions is great for those who have a significant amount to invest!

Let’s pretend you have $12,000 that you are ready to invest, and you haven’t yet started saving for retirement. Up until April 15th, you can invest $6,000 into a Roth or Traditional IRA for 2020. Then, you can invest another $6,000 for 2021! Where if you were to wait until later in the year, after April 15th, you would only be able to fund $6,000 for 2021.

If you have a decent chunk of cash you have been sitting on, waiting to invest, now is a perfect time to do some more research. Time is one of the most valuable ingredients in investing, and being able to still contribute for 2020 is the closest thing you’ll get to a time machine!

Change in income

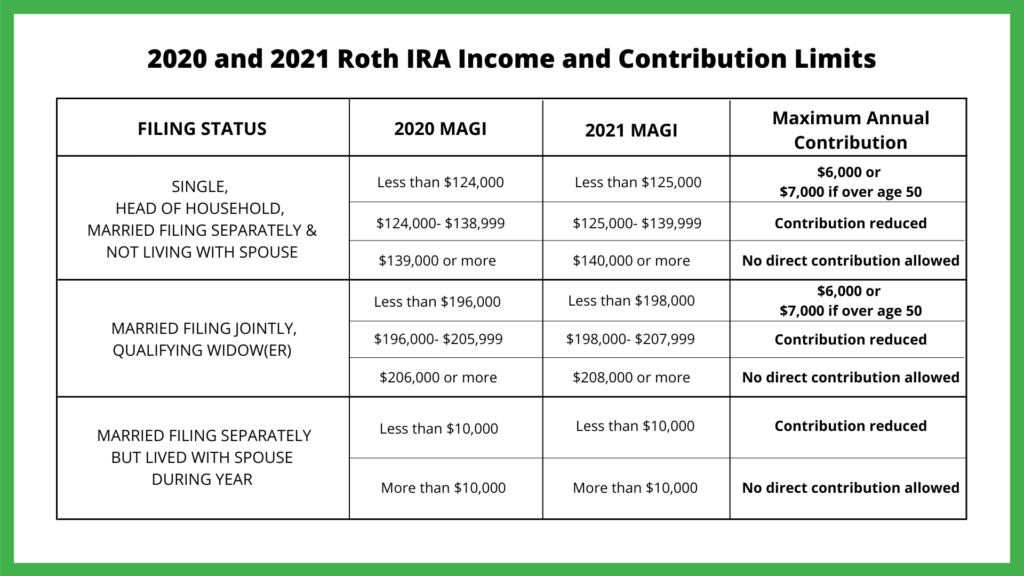

The Roth IRA is a fan-favorite for reaching financial freedom. However, there is an income limitation on this account. This income limit looks at your Modified Adjusted Gross Income or MAGI. If you expect your MAGI for 2021 to take you over the income threshold, but your 2020 income did not- consider maxing out your Roth IRA for 2020.

This year did bring a slight increase for Roth phase-outs. If you earn between $125,000 and $140,000 in 2021 as someone who files their taxes as single, your Roth contribution will be lowered from the $6,000 limit. Direct contributions are not allowed if you make $140,000 or more. Consider doing a backdoor Roth option instead.

For those who file as married filing jointly or qualifying widow(er), the contribution reduction happens if MAGI is between $198,000 – $207,999. If your MAGI is over $208,000, you will also not be able to directly contribute to the Roth IRA.

People who file as married filing separately get the short end of the stick here. Roth contributions are reduced regardless of your income, and then not allowed if your MAGI is over $10,000.

If you think 2021 will put you over the income limit for contributing to a Roth IRA, but 2020 did not, go back and max out that account! While being over the income threshold is a good problem to have, you will still want to take advantage of any contributions you are eligible to make.

To compare the change in 2020 to 2021 Roth Income and Contribution Limits, check out the table below.

If you find yourself over the income threshold but still want to contribute to a Roth IRA, read more about back-door conversions here.

The cons for contributing for the prior year and maxing out accounts

While the perks for maxing out your retirement account are huge, there are a few potential negatives. I do not believe these outweigh the pros, but they are still worth considering.

Waiting to include deductible contributions on your taxes

With the exception of the Roth IRA, all of these IRA’s are tax-deductible. Contributions for a given year will get deducted from that year’s income. This happens when you file your taxes. Since you are deducting contributions, you will want to have this information when you go to file your taxes.

Do you prefer filing your taxes early? Have your retirement contributions complete when you go to file! You can file an amendment if you end up contributing more after they are filed…but refiling your taxes isn’t something people normally get in line for.

If you want your taxes to be done when you file, make sure your IRAs are maxed out for the prior year. If they are not maxed out, at least make sure you are happy with the amount inside.

The mental toll of playing catch-up

Saving for your future and watching your investment accounts grow can be an empowering thing, but it can also be stressful. If you feel “behind” and you are struggling to put money away, squirreling money away for 2020 when we are in 2021 can make investing feel even more daunting.

When we start a new year, it’s understandable to want to move on from last year’s finances. I have a feeling that will hold especially true for 2020. Trying to max out your retirement account from last year for the next three months can often feel like running a race you already lost. If this is how you feel, try not to let deadlines get you down!

Any money you are able to put away into a retirement account is money that has the potential to grow, and help you in the future. Whether it’s 2020 or 2021 contributions, focus on the positive things that are going to come from your savings!

Are you maxing out your retirement accounts?

Did your financial goals last year include maxing out your 2020 retirement accounts? Or are you still striving towards that goal? Whether your accounts are maxed out or not, this is a great time to think about your investing goals!

Being at the start of a year not only gives you a full year ahead for contributions, but you also are sitting on a great window of time to make any last-minute contributions for 2020. Focusing on your goals and starting on a good foot this month will help set the tone for a successful year ahead!