Recessions are a hot topic – and never far from any investor’s mind.

It’s a sad fact of life that these periods are inescapable – sooner or later, the economy starts shrinking, asset prices drop, and the stock market takes a nosedive. In such circumstances, it is natural to enter damage control mode.

However, entering damage control the wrong way can easily result in wiping out years of positive progress in your portfolio. There are ways to not only survive but thrive in recessionary periods. Yet, this will require a large adjustment to the way you probably do things. If you can make that switch – do things differently than you would in a period of economic growth – your portfolio will continue to grow even in a recession.

Whether you want to protect your retirement portfolio from recession or are just starting out in your investing journey, there are six guiding lights that will lead you to water during a drought.

Let’s dive in.

What Exactly is a Recession?

Unsurprisingly, there isn’t a crystal-clear, universally agreed-upon answer to this very simple question. So let’s lay things out in the most fair, objective way we can.

The textbook answer is that a recession is a significant decline in economic activity that lasts for a prolonged period. The exact definition of a recession can vary depending on the source, but generally, it is characterized by a decline in gross domestic product (GDP) for two consecutive quarters or more.

These things are always tied to regulatory bodies, and in the United States, the National Bureau of Economic Research (NBER), a private, non-profit organization, is the body that officially declares when recessions start and end.

Here is where things get even trickier. The NBER uses a variety of lagging indicators to make the final call – declaring that a recession has arrived is big news (and it tends to make investors panic), so, in fairness, the NBER doesn’t want to risk a false positive.

However, that means that by the time the NBER sounds off on the issue, a recession could have been going on for months. This isn’t conjecture – in the case of the notorious 2008 ‘great recession’, NBER confirmed an official recession with an announcement in late 2008 – while also stating that the recession had begun in December of 2007, a full year earlier.

It’s best to be aware of how you can protect yourself in a recession even before one has officially been declared.

1. Before You Dive In, Make Sure:

In times of recession, risk tolerances change. Investing during periods of economic expansion and investing in a recession should be approached from two fundamentally different viewpoints.

Let’s lay the groundwork first by looking at a wider context. Your personal finances consist of more than just a stock portfolio. Recessions have adverse, far-reaching consequences on numerous industries, lead to rises in the cost of living expenses, and can make retaining employment a challenge.

First things first – make sure that your emergency savings fund is well stocked. The extent of these funds will depend on your personal preference, but a good rule of thumb is to aim for three, preferably six months of living expenses covered in advance.

If that condition is met, you can plan the scope of your investment. In times of recession, short-term trading is way too risky for most people – so a long-term approach is your best bet. This means that you shouldn’t count on taking money out of your portfolio for at least seven years.

In tandem with that, do yourself a favor and don’t obsessively check the performance of your investments – this is one of the classic mistakes when investing in a recession. Recessions are rough and tumble – your portfolio will most likely decline in value at times, but the objective here is to play the long game. If you can weather the long storm, you’ll end up on top – panic selling will only force you to absorb losses that would have been rectified in time.

2. Cash is King

Cash is an underappreciated asset class – but for completely understandable reasons. In general, cash doesn’t offer a rate of return that most investors are interested in – particularly when you factor in inflationary woes.

But that long-held belief has come under fire recently, and plenty of investors are changing their tune. We’ll just use the example of Ray Dalio – founder of the world’s largest hedge-fund firm. Dalio has been a champion of the “cash is trash” narrative for as long as anyone can remember. However, even he has come to the conclusion that in these circumstances, not only is cash not trash – cash is king.

There are a couple of reasons behind such a drastic shift in opinion – cash has outperformed expectations consistently, and money markets have seen levels of volume and inflow not seen since 2020.

The second point is opportunity cost and liquidity. A cornerstone of economics, think of opportunity cost as a missed opportunity – owning stock A would give you $5 in capital gains, but owning stock B would give you $7 in capital gains.

The $2 is the opportunity cost in this case. Thankfully, our portfolios are not set in stone – we can sell stocks and adjust our portfolios accordingly. But some stocks and other assets aren’t always easy to sell – and by that point, our window of opportunity might have already passed.

This is where and why cash, and cash equivalents, are king. Having cash enables you to take advantage of opportunities and get into positions that you might have otherwise missed due to a lack of capital. Cash equivalents, thankfully, are very liquid.

Allocating a large portion of your portfolio to cash and cash equivalents, however, is risky. If you sell off a portion of your portfolio at the bottom, and markets then rise, you’ll be incurring a large opportunity cost.

To make the best use of this method, allocate a small portion of your portfolio to cash – large enough to take advantage of great opportunities, but not large enough to present a risk to your portfolio.

A good way to combat the risks of inflation and holding large sums of cash is dollar-cost averaging. By purchasing a fixed dollar amount of a security every month, you will automatically purchase more of a stock when it is cheap, and less when it is expensive. In the long run, you will be paying average prices for the stock – but the slow and steady method means that there is no need to liquidate a lot of holdings or hold a lot of cash at any one time.

3. Stay Away From These Types of Stocks:

An ounce of prevention is worth a pound of cure – and in a recession, you don’t want to bring any unnecessary risk to the table. Knowing what to avoid is just as important as knowing what to move toward.

The fact of the matter is that the nature of some businesses makes them a poor choice for investing in during a recession. On the other hand, historically, several industries have proven themselves to be recession-resistant – but we’ll get to that in a minute.

So, what types of stocks should you give a wide berth?

- Highly indebted companies: Companies with a large amount of debt on their balance sheets can struggle to service that debt during a recession, especially if their revenues decline. In such cases, they may be forced to cut costs, including laying off employees or reducing investments in growth initiatives, which can lead to further declines in stock prices.

- Cyclical companies: These are companies whose fortunes are closely tied to the business cycle, such as those in the manufacturing, construction, or automotive industries. During a recession, these companies are likely to see a decline in demand for their products or services, which can hurt their revenues and profits.

- Speculative or growth stocks: These are stocks of companies that are not yet profitable but are expected to grow rapidly in the future. In a recession, investors may become less willing to take on risk, which can lead to a decline in the prices of these stocks.

- Tech companies: While tech companies are generally viewed as more resilient to economic downturns, they can still be vulnerable if their business models rely heavily on advertising or consumer spending. In addition, if the broader market experiences a downturn, investors may become less willing to pay high multiples for tech stocks, which can lead to declines in their prices.

Not all companies within these categories will necessarily perform poorly during a recession. Some may have strong balance sheets, economic moats, diversified revenue streams, or defensive business models that allow them to weather economic storms better than others.

To put it in plain English, it’s not necessarily a requirement to completely divest from these sectors – but be very wary of making new investments during times of recession.

4. Stocks that Tend to Do Well in a Recession

In a recessionary environment, investors tend to favor defensive stocks, which are companies that are less sensitive to changes in the business cycle and can continue to generate steady revenues and profits even during economic downturns. In today’s stock trading market, many of these shares are available to trade on commission-free stock trading platforms with advanced tools and research capabilities.

Note that not all companies within these defensive sectors will necessarily perform well during a recession. Some companies may have high levels of debt or exposure to risks that could harm their business even during a recession. Therefore, it’s essential to do your own research and analysis before making any investment decisions.

The types of investments that tend to do well in a recession are:

- Utilities: companies that provide essential services, such as electricity, gas, and water, which are needed regardless of economic conditions. They tend to have stable revenues and cash flows, making them less vulnerable to economic downturns.

- Consumer staples: products such as food, beverages, household products, and personal care items. Companies that produce and sell these products tend to have steady demand and revenues, making them defensive stocks in a recession.

- Healthcare: Healthcare companies, including pharmaceuticals, biotech, and medical device manufacturers, tend to have stable demand for their products and services regardless of the state of the economy. In addition, healthcare spending is often considered a non-discretionary expense, which can provide a defensive buffer in a recession.

- Insurance companies tend to do well in a recession because consumers are more likely to purchase insurance products to protect their assets and income. In addition, insurance companies tend to invest in fixed-income securities, which can provide a source of stable income during times of economic uncertainty.

- Precious metals, such as gold and silver, are often considered safe-haven assets during times of economic uncertainty. They tend to hold their value or even appreciate in value during recessions, making them a popular choice among investors seeking a defensive investment.

- Real estate can be a defensive investment in a recession, especially if the properties generate stable rental income. Additionally, some real estate investments, such as real estate investment trusts (REITs), can offer diversification benefits and can act as a hedge against inflation. The law requires REITs to distribute 90% of their taxable income as dividends.

Since we’ve touched on the topic of dividends, dividend stocks also deserve a mention. Companies that have consistently been paying (and raising) dividends over a long period of time usually fall into the category of blue-chip stocks, have strong balance sheets, and are likely to fare well in times of recession. Important factors to consider here are their current dividend yield, years of dividend growth, and recent business fundamentals.

Investing in dividend stocks is a simple approach that can lead to revenue generation even in declining or sideways markets, while still offering investors all the benefits of capital appreciation.

[Realted: Should You Invest in Real Estate in a Market Downturn?]

5. Look into Bonds and Uncorrelated Assets

Investing in uncorrelated assets can be a good way to diversify your portfolio and reduce overall risk. These assets have a low or negative correlation with the performance of the stock market, which means that they can provide a hedge against market volatility and economic uncertainty. Here are some examples:

- Investment-grade bonds: These are bonds issued by companies or governments with a high credit rating. They tend to have lower risk and lower returns than stocks but can provide a source of stable income during times of market volatility.

- Insurance-linked securities: These are investments that are tied to insurance events, such as natural disasters or other catastrophic events. They are a source of uncorrelated returns because their performance depends on global climate policies, not the stock market, tying them.

- Carbon credits: Carbon credits are a type of environmental asset that represents the right to emit a certain amount of carbon dioxide or other greenhouse gases. Carbon credits can provide a source of uncorrelated returns, as their performance is not tied to the stock market but instead dependent on global climate policies.

- Commodities: Commodities, such as gold, oil, or agriculture products, can provide a source of uncorrelated returns, as their performance is often tied to supply and demand factors rather than the stock market.

- Other alternative investments: this can include private equity, hedge funds, or venture capital funds. These investments can provide access to strategies and asset classes that are not easily accessible through traditional stocks and bonds.

While uncorrelated assets can provide diversification benefits, they may not always perform well, and some of these assets may carry additional risk, such as liquidity or regulatory risk. Therefore, it is best to limit your investments in this direction to a small percentage of your overall portfolio.

6. If Your Risk Tolerance Can Handle It, Consider Options Trading

Last but not least, number six on our list might be the only legitimately unexpected point we’re going to raise. Options, being derivatives, are inherently risky. At first glance, one would expect that the inherent volatility would make them a poor choice in times of recession – but that isn’t necessarily true.

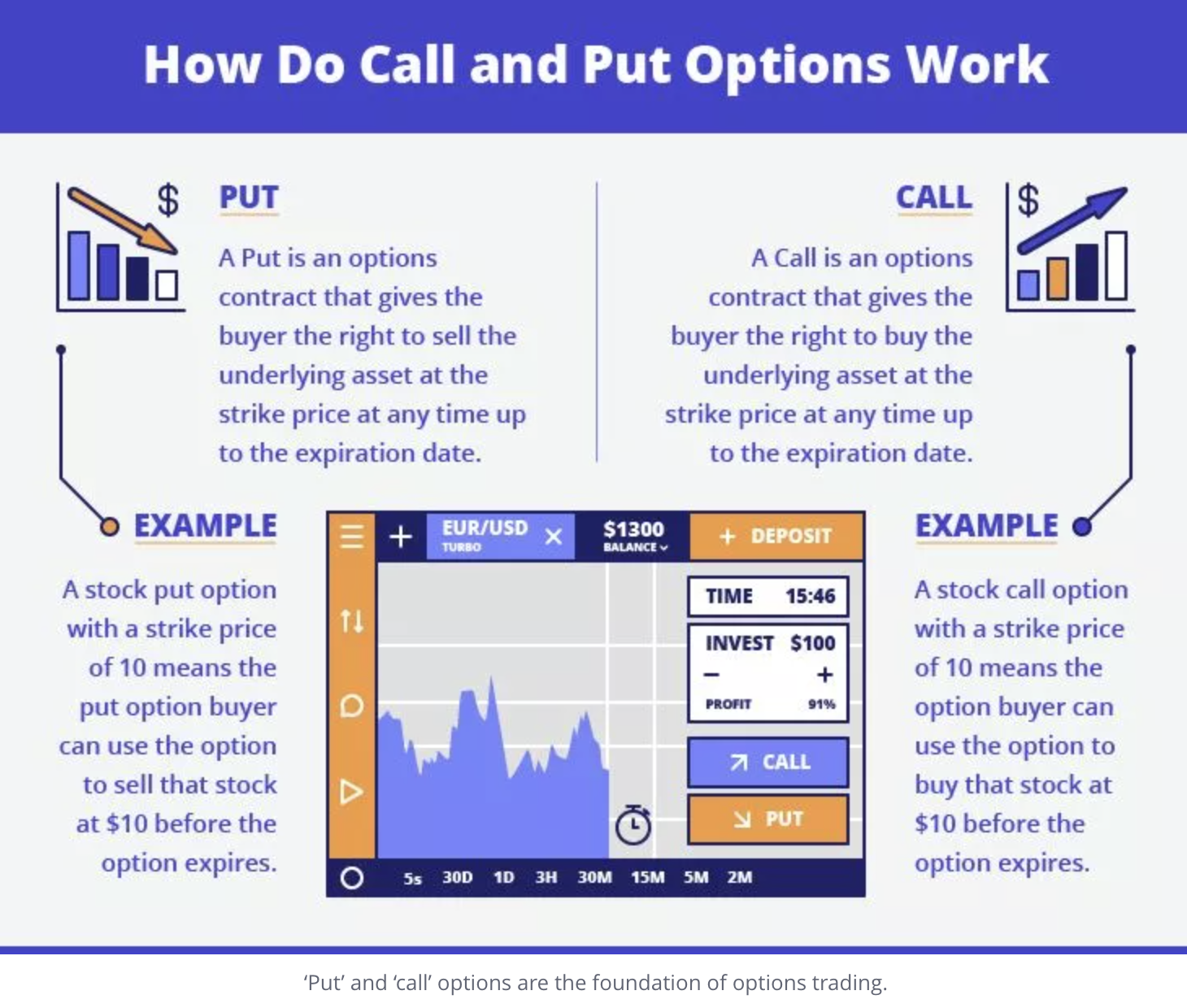

Although going about things in this way does require a high-risk tolerance, options trading offers a unique opportunity to profit directly from falling stock prices. There are two basic types of options contracts: calls and puts, and puts are chiefly what interests us in this particular discussion.

A put option is a contract that gives the buyer the right, but not the obligation, to sell a stock at a specific price (known as the strike price) on or before a specific date (known as the expiration date). By buying put options, investors can benefit from a decline in the stock price, as the value of the put option will increase as the stock price falls.

Suppose an investor believes that a recession is likely to cause a decline in the stock market. The investor purchases put options for a particular stock with a strike price of $100 and an expiration date of six months from now. The current price of the stock is $110.

If the stock price falls to $90 at the expiration date, the investor can exercise the put option and sell the stock for $100, even though the market price has fallen to $90. The investor can profit from the difference between the market price and the strike price, which is $10 per share.

If the stock price does not fall below the strike price of $100, the investor can choose not to exercise the put option and allow it to expire worthless. In this case, the investor’s maximum loss is limited to the premium paid for the put option.

Of course, we don’t recommend trying this unless you’ve already got a pretty good handle on how options work – but the presence of beginner-friendly option trading strategies, as well as risk management methods such as stop loss orders and sell targets, means options trading looks a lot more daunting than it actually is, once you actually get down to it.

In addition to profiting from falling prices using put contracts, people commonly use puts as a hedge against other long positions. This is a technique in risk management where investors and traders can protect themselves from the damage incurred by future losses.

Conclusion

Recessions are tough, scary, and risky times. Weathering them as best you can is critically important to your financial well-being and that of your family.

However, making the right investment decisions in those tough times allows you not only to avoid or better handle some of that hurt but to actually thrive in those conditions.

At the end of the day, the sad fact is that none of us will avoid a recession and that none of us are recession-proof. Knowing what to do in those critical moments is of the utmost importance – and we hope we’ve been able to help you along in that regard.