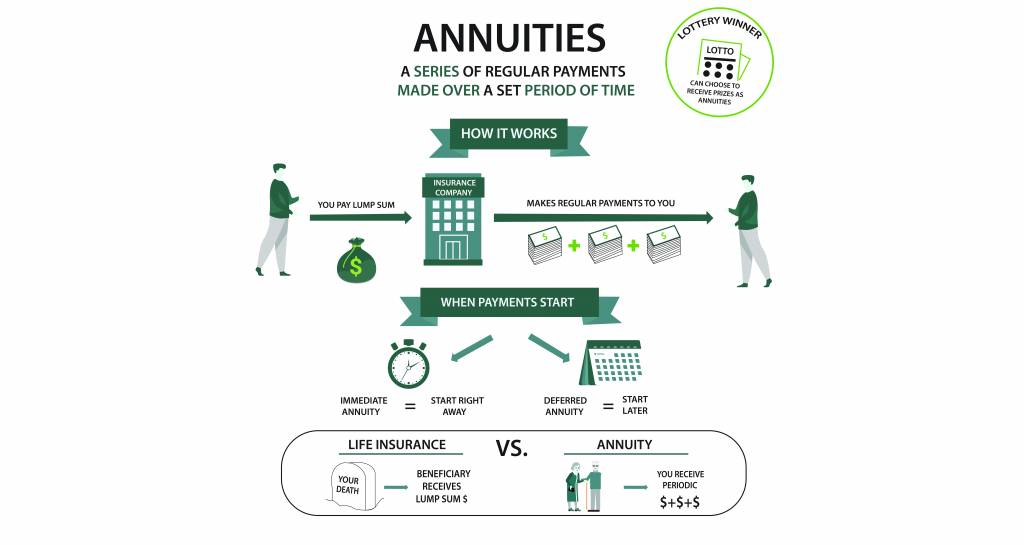

An annuity is a contract between an individual and an insurance company in which the individual pays a lump sum or series of payments to the insurance company in return for periodic payments for life or a specified period. How much income annuities pay can vary depending on the purchaser’s age, gender, and other factors. But, regardless of that, annuities provide retirees with a stable source of income that can help them maintain their standard of living during retirement.

But, exactly how much do you have to put upfront to maintain that standard of living? In this blog post, we will discuss how much income annuities pay and some factors that affect annuity payments. We’ll also cover some examples of how much you would receive for different types of annuities and different circumstances. So, whether you’re already retired and want to know how much income you can get out of your nest egg or just starting to save for retirement and want to get an idea of how much you’ll have to save for comfortable living according to your particular needs, this post is for you.

Table of Contents

ToggleHow is annuity income calculated?

Annuity income depends on a wide array of factors that include your age, gender, the type of annuity contract you’re entering, whether or not it offers guaranteed lifetime income, guaranteed rates, and the particular type of contract riders you add to the annuity when you sign.

Although annuities usually won’t get you the rate of growth of other investment vehicles, like stocks, bonds or ETFs, they do offer much more security and peace of mind.

Types of annuity contracts

When calculating annuity income, the first thing to consider is the type of annuity you’re purchasing. There are several types of annuities, including:

- Immediate fixed annuities

- Immediate variable annuities

- Deferred fixed annuities

- Deferred variable annuities

- Indexed annuities

- Multi-year Guaranteed Annuities or MYGAs, and more,

In addition, you can also personalize your annuity contract by adding special annuity riders to add more leverage, principal protection and guarantees. Most of these riders come with a fee that reduces the amount of income-generating capital you’ll have in your favor for a set.

Each particular type of annuity has its way of calculating present and future values and payouts.

How payments are calculated for immediate fixed annuities:

This is the simplest type of annuity, and in this case, payouts only depend on your principal amount (the present value of your annuity or the lump sum you pay to purchase it), the number of payouts per year (12 if you want monthly payments, 6 if you want them bi-monthly, 4 if you want them quarterly or 1 if you prefer annual payments), the annual rate and the number of years the contract will pay you income.

How payments are calculated for deferred fixed annuities:

There are two different scenarios in the case of deferred annuities. One is when you pay a single lump sum to the insurance company, and your money grows at a certain rate before the annuitization phase, and another is when you make periodic payments to the insurance company like you would make contributions to a 401(k).

In either of the two cases, payments depend on the same factors as above during the annuitization phase (once payouts begin) but also on the number of years your money grows during the accumulation phase and the number and size of the payments you make during this time.

Age, gender and annuity payouts

After the type of contract, age and gender are two of the most important factors determining payouts. They affect immediate and deferred annuities and are particularly important for guaranteed lifetime annuities.

It all has to do with your average life expectancy, which insurance companies are particularly good at estimating. When you start receiving payments, the younger you are, the more payments you’re likely to receive. Also, women tend to live longer than men, so, for the same age, they’ll receive more payments than men do.

If you’re purchasing a fixed annuity that guarantees a monthly income for a predefined number of years, then age and gender will play into the insurance company’s rate. The longer you’re expected to live, the lower the annuity’s rate and vice versa.

On the other hand, if you’re purchasing a lifetime annuity that guarantees you won’t outlive your savings, then the order you are, the higher the monthly payments will be because the insurance company will have to pay your principal plus interests in a shorter amount of time. This means that, in the case of men and women of equal age, men will usually receive slightly higher income for the same price than women, simply because women are likely to live longer.

How much income does a Single Premium Immediate Annuity pay?

In this and the following sections, we’ll go over several examples of the amount of estimated income you may receive from different types of annuities. As stated above, annuity income depends on the rate the insurance company offers in the contract, which is at their sole discretion. Therefore, any amount we present in this and the following sections will be no more than an estimate of how much you can potentially receive if you purchase an annuity under a very specific set of conditions.

It should give you a rough idea of how much you would need to invest to receive the guaranteed income you feel you’ll need during retirement. It will also give you an idea of how much you stand to receive based on the current size of your nest egg.

Example of a $100,000 immediate annuity

The following table shows the monthly income you can expect from a $100,000 immediate annuity that pays monthly income for different total numbers of years and at various common rates. As a general rule, the longer the annuitization phase (i.e., the number of years you’ll receive monthñy payments), the higher the insurance company’s rate. Therefore, the lower rates apply mostly to short-term fixed annuities, while the highest rates (from 2.65% and up) apply to longer-term ones.

| # of | years | ||||||

| Rate (r) | 1 | 2 | 3 | 5 | 7 | 10 | 20 |

| 1.50% | $8,401 | $4,232 | $2,842 | $1,731 | $1,255 | $898 | $483 |

| 2.00% | $8,424 | $4,254 | $2,864 | $1,753 | $1,277 | $920 | $506 |

| 2.15% | $8,431 | $4,261 | $2,871 | $1,759 | $1,283 | $927 | $513 |

| 2.65% | $8,453 | $4,283 | $2,893 | $1,781 | $1,306 | $950 | $537 |

| 3.15% | $8,476 | $4,305 | $2,915 | $1,804 | $1,328 | $973 | $562 |

| 3.25% | $8,481 | $4,309 | $2,919 | $1,808 | $1,333 | $977 | $567 |

As you can see, depending on how long you want your money to last, you’ll receive different monthly payments. The longer the time, the lower the payment since your principal has to be spread out over more months. However, you’re receiving more because of the annuity rate when you add up the total amount.

The most common scenario is for retirees to purchase long-term annuities that last 5 to 20 years, on which you can usually get anywhere from a 2.5% to a 3.25% rate, depending on the conditions of your contract and your age and gender and any riders you may have added.

Rounding out the numbers, a $100,000 annuity purchased today can payout between $550 and $1,300, depending on the number of years the contract lasts.

Example of a $500,000 annuity

If instead of $100,000, you invest $500,000, you’ll receive 5X the amounts we saw before. You can see the actual numbers in the following table:

| # of | years | ||||||

| Rate (r) | 1 | 2 | 3 | 5 | 7 | 10 | 20 |

| 1.50% | $42,006 | $21,160 | $14,212 | $8,655 | $6,274 | $4,490 | $2,413 |

| 2.00% | $42,119 | $21,270 | $14,321 | $8,764 | $6,384 | $4,601 | $2,529 |

| 2.15% | $42,154 | $21,303 | $14,354 | $8,797 | $6,417 | $4,634 | $2,565 |

| 2.65% | $42,267 | $21,413 | $14,464 | $8,907 | $6,528 | $4,748 | $2,686 |

| 3.15% | $42,381 | $21,524 | $14,574 | $9,018 | $6,641 | $4,863 | $2,811 |

| 3.25% | $42,404 | $21,546 | $14,596 | $9,040 | $6,663 | $4,886 | $2,836 |

With higher premiums, you may be able to access better rates to receive more than 5X monthly payouts from a $500,000 compared to a $100,000 annuity.

How much income does a deferred annuity pay?

As we saw before, there are two basic types of deferred annuities, those where you pay a single premium and let that grow until it reaches maturity and you annuitize it, and those where you make periodic contributions over time. In either case, payments during the annuitization phase will depend on when you made the initial payment or when you started making your regular payments. It also depends on the insurance company’s rate during the accumulation phase and for how long you will receive payments once they start.

Let’s take a look at one example of each case. In both examples, we assume a fixed rate of 3.5% during the accumulation period, which is a good rate by industry standards for 20 or more years of growth. In all the examples, you begin receiving payments at age 60.

Example of a $100,000 annuity purchased at age 20 at a 3.5% annual rate with payments starting at age 60

The following table shows payments for different annuitization periods and rates, assuming you purchase a $100,000 deferred annuity at age 20, growing over 40 years at 3.5%.

| # of | years | ||||||

|---|---|---|---|---|---|---|---|

| Rate (r) | 1 | 2 | 3 | 5 | 7 | 10 | 20 |

| 1.50% | $33,999 | $17,127 | $11,503 | $7,005 | $5,078 | $3,634 | $1,953 |

| 2.00% | $34,091 | $17,216 | $11,591 | $7,093 | $5,167 | $3,724 | $2,047 |

| 2.15% | $34,119 | $17,243 | $11,618 | $7,120 | $5,194 | $3,751 | $2,076 |

| 2.65% | $34,211 | $17,332 | $11,707 | $7,209 | $5,284 | $3,843 | $2,174 |

| 3.15% | $34,303 | $17,421 | $11,796 | $7,299 | $5,375 | $3,936 | $2,275 |

| 3.25% | $34,321 | $17,439 | $11,814 | $7,317 | $5,393 | $3,955 | $2,295 |

As you can see, through the magic of compounding interests, the $100,000 grow into more than $400,000 by the end of the accumulation period, giving you a guaranteed monthly income of between $2,300 and $5,300, depending on the total duration of the annuity.

Example of a $100,000 annuity purchased at age 40 at a 3.5% annual rate with payments starting at age 60

The following table shows payments for different annuitization periods and rates, assuming you purchase a $100,000 deferred annuity at age 40, growing over 20 years at 3.5%.

| # of | years | ||||||

| Rate (r) | 1 | 2 | 3 | 5 | 7 | 10 | 20 |

| 1.50% | $16,901 | $8,514 | $5,718 | $3,482 | $2,524 | $1,806 | $971 |

| 2.00% | $16,946 | $8,558 | $5,762 | $3,526 | $2,568 | $1,851 | $1,018 |

| 2.15% | $16,960 | $8,571 | $5,775 | $3,539 | $2,582 | $1,865 | $1,032 |

| 2.65% | $17,006 | $8,615 | $5,819 | $3,584 | $2,627 | $1,910 | $1,081 |

| 3.15% | $17,052 | $8,660 | $5,864 | $3,628 | $2,672 | $1,956 | $1,131 |

| 3.25% | $17,061 | $8,669 | $5,872 | $3,637 | $2,681 | $1,966 | $1,141 |

As you can see, payments dramatically decrease if you buy the same annuity 20 years later than before.

Example of an annuity contract where you deposit $250 every month from age 20 with payments starting at age 60

The following table shows an example of payments for different annuitization periods and rates, assuming you purchase an annuity by making monthly contributions of $250 starting at age 20, growing over 40 years at 3.5%.

| # of | years | ||||||

|---|---|---|---|---|---|---|---|

| Rate (r) | 1 | 2 | 3 | 5 | 7 | 10 | 20 |

| 1.50% | $22,005 | $11,085 | $7,445 | $4,534 | $3,287 | $2,352 | $1,264 |

| 2.00% | $22,065 | $11,143 | $7,502 | $4,591 | $3,344 | $2,410 | $1,325 |

| 2.15% | $22,082 | $11,160 | $7,519 | $4,608 | $3,362 | $2,428 | $1,344 |

| 2.65% | $22,142 | $11,217 | $7,577 | $4,666 | $3,420 | $2,487 | $1,407 |

| 3.15% | $22,202 | $11,275 | $7,635 | $4,724 | $3,479 | $2,547 | $1,472 |

| 3.25% | $22,214 | $11,287 | $7,646 | $4,736 | $3,491 | $2,560 | $1,486 |

If at age 20, you start saving $250 every month and put the money into an annuity that grows at 3.5% annually, by the time you’re 60, you’ll have $262,000 saved up. That will guarantee you an income of around $1,500 every month for the next 20 years, or around $4,600 for the next five years.

How much income does a lifetime annuity pay?

Lifetime annuities differ from the others we’ve seen here in that their duration isn’t predefined. Instead, the insurance company guarantees you’ll continue to receive payments until the day you die (if it’s a single life annuity) or until you and your spouse die (if it’s a joint-life annuity).

Consequently, it all boils down to how long the insurance company expects you (and possibly your spouse) to live. This depends on your current age and gender as well as other factors. Then, they’ll do a similar calculation to the one we did in the previous tables.

The bottom line

Annuities are a great way to ensure a steady income stream for the rest of your life. We’ve shown you how annuity payments are calculated and how much they pay under different circumstances. We’ve also given examples of different annuities and how much they pay. In general terms, every $100,000 you invest in an immediate annuity when already retired can bring in close to $600 per month for the better part of the rest of your life. Including a lifetime income rider may lower your payouts slightly, but you’ll get the guarantee of not outliving your savings in return.

On the other hand, if you start saving from an early age, you can get much more bang for your buck by the time you retire, and could even retire early. The same $100,000 invested at age 20 will guarantee over $2,000 per month.