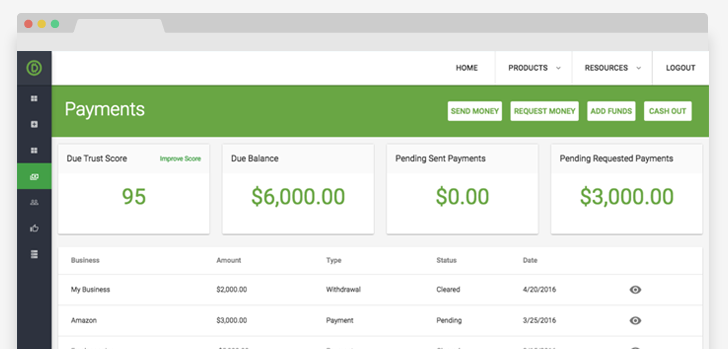

Even in other countries, online transactions are rapidly gaining ground as the preferred way to shop and access services. Companies are also seeking outsourced talent from all over the globe, increasing the demand for an international payment solution that offers currency exchange, language support, and tax compliance. When you can address this demand, you will be able to attract many more customers and clients.

While the technology is available to make international credit card processing efficient, the costs to process transactions is still considerably higher. This includes exchange rates and fees as well as other taxes and fees imposed by different countries. Wire transfers and other payment methods previously used are expensive However, by using an international credit card processing company that maintains a transparent pricing system and flat transaction fee, you will be able to minimize the cost of each transaction.

Other methods of receiving an international payment can become quite time-consuming, especially if traditional mail is involved. Then, there is the time it takes to find a financial institution that may accept that international payment. All this time takes away from what could be a higher cash flow that you need to cover expenses, sustain your business, or use for reinvestment and expansion purposes.

As part of an entire billing and payment system that can become automated, removing paper and people from the process, you will gain significant efficiencies while allowing you to focus on your core capabilities.

![]()

“I highly recommend sites like Due.com to handle your finances. With them, you have everything you need to bill clients, keep track of finances and do your taxes.”

Chicago Tribune

![]()

“In looking at the various country regulations related to online payments, it becomes clear that more work needs to be done. Due is the answer”

Inc

![]()

“If you are already in business and looking to expand, you might be held back by a similar concern: you don’t have the funding to take your company to the next level.”

business.com

![]()

“Due is one of the top payment tools that will grow your online retail business.”

Blog Herald

![]()

“Due.com has been used to easily keep track of their hours and then invoice clients and get paid in more than 100 countries.”

Inc

“We like Due.com for how easy it is for users to track time from anywhere you happen to be working – from home or the local coffee shop”

LifeHacker

The days of the mom and pop stores might not be completely over but owners of small firms who know all their customers by name, have known them all for years—and can visit their homes after a short walk—have become rarer than ever. Big box stores have crowded out old-fashioned hardware stores, and every other type of store. The local place to get a coffee and a cake is more likely to be a Starbucks than a Marge’s Diner. Independent bookstores were beaten up by Borders and Barnes and Noble, and then killed off by Amazon. When local customers can buy anything they want online, without leaving their living room, location is no longer all it used to be for retailers.

It’s not all bad news though. While businesses that cater only to local buyers have come under pressure, it’s now easier than ever for even the smallest of firms to reach markets anywhere in the world. As residents of cities from Brazilia to Beijing have seen their incomes grow, these global customers now have the means to make the purchases they want from companies selling far away.

The result is that we’re now living with an entirely new opportunity, a world of global trade in which anyone can participate, selling to customers on the other side of the world, shipping products and taking payments.

For many businesses, this scenario is already happening. In 2014, eMarketer1 reported that for the first time, consumers in the Asia-Pacific region were set to spend more on ecommerce purchases than buyers in North America; consumers were on course to spend more than $525 billion in comparison to North America’s $483 billion. By 2017, the research company estimated the value of global ecommerce was likely to reach $2.357 trillion.

That’s a giant amount of money, and it means that businesses that choose only to trade locally are cutting themselves out of a much bigger market. For many businesses, there’s no reason to cut themselves out of anything anywhere. Shipping abroad might be expensive but if the product can’t be bought locally at all, customers will be willing to pay the extra delivery costs. In 2015, around 30 percent of Etsy’s $2.4 billion worth of sales were international2.

Of course, those sales aren’t always straightforward. International marketing may need some localization but it might only be a matter of finding local affiliates, translating a sales page or picking an additional geographic region. Local laws and customs may demand some changes but these laws are rarely an obstacle to international trade that can’t be overcome.

The same is true of accepting payments.

1. eMarketer.com, Global B2C Ecommerce Sales to Hit $1.5 Trillion This Year Driven by Growth in Emerging Markets, February 3, 2014 (http://www.emarketer.com/Article/Global-B2C-Ecommerce-Sales-Hit-15-Trillion-This-Year-Driven-by-Growth-Emerging-Markets/1010575#sthash.NEEDdgF9.dpuf)

2. Statista.com, International share of Etsy’s gross merchandise sales volume from 2012 to 2015 (www.statista.com/statistics/409373/etsy-international-gms/)

Today’s payment platforms, such as Due, now assume that clients will want to sell abroad, and they’re set up to accept multiple currencies from buyers in almost every location.

That digital payment platforms take international payments shouldn’t surprise anyone because the need for a way to make international payments is almost as old as trade itself. The island of Delos had little to recommend it to travelers but a temple of Apollo, but this island was able to generate wealth by offering credit transfers for clients across the ancient world whose accounts were kept up to date by a record of receipts. At a time when payments were made in cash consisting of bags of gold, silver and bronze coins, this island’s ability to make credit transfers may well have been the first instance of international banking.

Coins, made during the Roman period, have been found in locations as distant as Scotland and India, a sign not just of an enormous empire, but tells of a system whose merchants were able to trade beyond the borders of that empire.

And the hawala system used across the Islamic world dates back to the eighth century, allowing money to be deposited with an agent in one country then withdrawn from the agent’s partner in another.

For as long as trade routes have stretched beyond the forum—which is as long as trade has taken place—there has been a need for payments to be able to travel as far as the long distances the very travelers themselves have gone and to be able to be used in a way that’s fast, reliable and inexpensive.

In this guide, we’re going to explain not just how to accept those payments but who you should be accepting them from and what you need to know about trading in multiple currencies.

We’ll start by looking at the opportunities which have presented themselves. The rise not just of China but of all the BRIC countries (Brazil, Russia, India and China) has created giant new markets for sellers, all of which can now be reached easily through online marketing. We’ll explain which countries are the biggest buyers and we’ll explore what people in those countries are looking to buy.

We’ll then discuss the various ways in which payments can be made and collected overseas. There are lots of different methods of taking payments from customers and buyers in places as distant as Suriname and South Africa, so it’s important to understand the different options and know which option will be the best for your business.

We’ll also look at the risks involved in those payments. International payments can have long floats and when you’re shipping long-distance, dealing with disputes is much harder than working through a local legal system. We’ll look at the dangers in selling around the world, explain what you can do to lower the risks and show you why any remaining risk is far outweighed by the opportunity.

Finally, we’ll discuss exchange rates. When you’re taking payments in foreign currencies, you will have to deal with the exchange rates, a situation that can be a large opportunity as well as a small obstacle.

Selling internationally used to be impossible for small businesses. It’s now an opportunity for small businesses to reach out, and a chance to break into a giant market made up of happy customers all around the world. In this guide, we’ll show you how to turn a small firm into a global success.

In August 2015, Brendon Farley, an artist in Minnesota with an Etsy store, asked other sellers on the craft platform what percentage of their sales were international4. He had recently added a shipping profile for Canada after a customer in that country had asked for a painting, and had been surprised to find that most of his views over the last 30 days had come from north of the border.

“I get regular views from the USA, Canada, Australia, and Eastern European countries,” he said. “Really starting to wonder how much business I am losing.”

The post in the forum generated 45 responses, and the percentages ranged considerably. Just one person said that they made no international sales. A few, particularly those selling outside the United States, said that all of their sales were international while other percentages ranged from 2 percent to as much as 95 percent.

For anyone selling online, the market is definitely global and not merely local. Restricting business only to people with minimum shipping rates and no international borders means losing a great deal of business. The question isn’t whether a business can expand their sales, but rather, how much they can expand their sales? Which countries they should a company be targeting and what do these businesses need to do to reach buyers in those regions?

Sellers should be looking for buyers in every country that has people willing to pay for the goods or services that seller can produce, and from which the seller can accept payments in the currency of the country. But, some countries are easier targets than others.

A survey4 conducted in 2014 by Pitney Bowes asked around 12,000 people in twelve countries about their online purchases. Almost all of them (96 percent) had bought something online and as many as 40 percent of the buyers had bought goods from another country. Australians were the people most likely to import products they’d bought online, followed by Canada and Russia. Shoppers in South Korea, China, India and Japan were more reluctant, believing they could only purchase goods online from retailers in their own country. “But our research shows there is a significant opportunity in markets like Brazil, Germany and China,” the commerce company said. “And those markets – particularly Brazil and China – are growing at a much faster rate.”

While any country should be considered a potential target market, for the sake of ease, U.S. sellers can divide customers outside the United States into three regions.

1. English-Speaking Countries

Pitney Bowes, which helps companies expand internationally, notes that the biggest “U.S. cross-border growth engines are Canada, the UK and Australia,” all English-speaking countries. When there are no language barriers to overcome and few cultural differences that make products and

3. https://www.etsy.com/teams/7722/discussions/discuss/16673897/

4. 2014 Pitney Bowes Global Online Shopping Study

tastes formed in one country unattractive in another – those countries make up the easiest opportunities. There’s no need to translate sales pages. Customer services can be conducted directly and without using translations. Each side understands the other and knows exactly what to expect. With the exception of the delivery fees and possible custom charges, selling from the U.S. to Australia, the UK, Canada and even South Africa can feel as familiar and as straightforward as selling to Hawaii or Alaska.

For sellers in northern U.S. states, customers in Canada may be closer than those in the south, and Australia, in particular, suffers from a lack of supplies that makes imports attractive. The duty threshold of $1,000 AUS also makes most of those product imports duty-free.

2. European Countries

Not only do the UK, Canada and Australia speak the same language as the U.S. sellers, they also have similar standards of living, which means that a product aimed at average earners in the U.S. will be targeting a similar demographic in those other countries. The same language and standard of living is generally true in the countries in Western Europe, as well.

Pitney Bowes highlights Germany as one of “the most desirable e-destinations,” helped no doubt by its stable economy and thrifty customers. But other European countries, including France, Spain, Italy, Holland, Belgium and the Scandinavian nations should also be on the list of target markets. Those countries alone contain more than 220 million potential customers and have a GDP per capita ranging from around $30,000 in Spain to nearly $101,000 in oil-rich Norway.

A US-only retailer that can tap into those countries will have increased their market size by about two-thirds and be reaching people with similar spending power or even a higher spend growth.

3. BRICs

The most exciting market development over the last couple of decades has been the rise of countries whose populations traditionally had little spare cash, in particular Brazil, Russia, India and China. Between 1989 and 2016, China experienced GDP growth of 9.85 percent5 , a rate high enough to suck in Western brands as large as Louis Vuitton and Ferrari. Shopping malls in the tier one cities of Shanghai and Beijing are filled with the kinds of luxury goods that are more usually found in the best parts of New York or Beverly Hills.

But they’re also mostly empty. Although Beijing has now overtaken New York as the world’s billionaire capital6 , the average wage is still only around $8,655 a year and the average consumer spends only $7 every day, mostly on food and clothing. Americans typically spend $97 a day with nearly one dollar in five going to recreation. The numbers are changing quickly. McKinsey7 estimates that by 2022 more than 75 percent of China’s urban consumers will be earning between $9,000 and

5. TradingEconomics.com, China GDP Annual Growth Rate (www.tradingeconomics.com/china/gdp-growth-annual)

6. Bloomberg.com. Rachel Change, Here’s What China’s Middle Classes Really Earn — and Spend, March 10, 2016 (www.bloomberg.com/news/articles/2016-03-09/here-s-what-china-s-middle-class-really-earn-and-spend)

7. McKinsey.com, Dominic Barton, Yougang Chen, and Amy Jin, Mapping China’s middle class, June 2013 (www.mckinsey.com/industries/retail/our-insights/mapping-chinas-middle-class)

$34,000 a year. China may already have 109 million people with wealth of between $50,000 and $500,000 – a size that gives the country a bigger middle class than America.

This wealth has grown as the Internet in China has developed. According to eMarketer, about 16 percent ($672 billion) of all spending in China takes place online, of which about half is spent on mobile devices.

So preparing a pitch to a market in China, and you’ll be aiming at a lot of people with rapidly growing funds who are used to spending online. But you’ll also be dealing with a place where the normal online sales strategies just don’t work. Not only will you need to translate your content and deal with the fact that same day-delivery in Chinese cities has been common for more than a decade and costs very little, you’ll also be working in an environment that has none of the Internet tools you’ll be used to employing. Google, Twitter and Facebook are all blocked in China, together with the platforms they own. China’s online consumers search on Baidu.com, chat on WeChat, a mixture of WhatsApp and Twitter, and they buy on AliBaba. China might have a giant market with deepening pockets but reaching it is difficult.

There are some open doors though. AliBaba has an opening for foreign sellers on its Tmall Global property. (Macy’s used it to create their Chinese online store.) Jing Dong (JD.com) offers a similar service in the form of JD Worldwide, and different industries have their own dedicated platforms such as Suning.com for electronics.

Brazil and Russia each offers a very different challenge. While both countries appeared to be shaking off years of slow growth, both are now battling shrinking economies and smaller pay packets. Real average monthly incomes in Brazil have fallen from $568 in 2015 to $550 a year later. Russia’s monthly wages have stayed relatively stable at around 35,000 rubles over the same period but the value of the ruble against the dollar has declined by 50 percent since 2014, increasing the price of imports. The volatility of the ruble led Apple to stop online sales in that country.

But Brazil is the only South American country that eMarketer8 places in its top ten worldwide retail ecommerce markets, one place below Russia. About 5 percent of retail sales are made online, with fashion products and health and beauty aids together making more than a third of all purchases. Like China’s online market, Brazil too has large malls such as Deremate.com, Dereto.com and MercadoLibre.com, Latin America’s equivalent to Ebay. In 2011, Brazil’s government tried to choke orders made for goods outside Brazil by raising taxes on credit card purchases for cross-border purchases from 2.28 percent to 6.38 percent.

Russian officials have been more generous… but not much more. In 2014, the government agreed to continue not to tax products ordered from foreign retailers, provided the purchases do not exceed 150 euros in value or weight more than ten kilos. (Purchases above those limits are taxed at 30 percent.)9 That was better than hoped for, but it was a decline from a limit of 1,000 euros and 31 kilos. Like China, search in Russia uses a local site, Yandex, rather than Google, and payment is often in the form of cash on delivery rather than credit cards or secure payment platforms.

8. eMarketer.com, Brazil Ranks No. 10 for Retail Ecommerce Sales Worldwide, January 7, 2015, (www.emarketer.com/Article/Brazil-Ranks-No-10-Retail-Ecommerce-Sales-Worldwide/1011804)

InternetRetailer.com, Adrien Henni, Good news for online retailers selling into Russia, June 2, 2014 (www.internetretailer.com/commentary/2014/06/02/good-news-online-retailers-selling-russia)

While India has the advantage for US-based retailers of having an English-speaking population, the growth of its middle class has been slower than in China. McKinsey Global Institute10 defines India’s middle class as households with annual disposable incomes of between $3,606 to $18,031, and sees the numbers rising from 50 million in 2005 to over 250 million in 2015. By 2025, the organization expects it to reach 583 million, which is 41 percent of the population.

That’s a large income spread though, and making significant inroads can require a great deal of localization. Fashion store Koovs, chaired by Britain’s Lord Alli who also chairs retail chain Asos, grew its sales in India by 210 percent between mid-September 2015 and the start of January 2016 to reach £2.96 million11. The company used marketing that took its inspiration from India’s Bollywood movie industry. Smaller sellers can use platforms that include Flipkart.com, SnapDeal.com and Zepo.in but success in India will depend on a combination of choosing the kinds of unique products that can’t be bought locally and using careful pricing. Google’s search trends suggest that electronics, clothing and accessories are the most sought items online in India but local prices are low, so exporters will need to bring something unique to the market in order to land sales.

According to Pitney Bowes, the highest volume of cross-border purchases have been of luxury goods and brands, such as clothing, jewelry and shoes. As the cost of shipping has fallen, product categories have expanded so that auto parts are now being exported to Australia, for example.

This commerce company advises businesses considering expanding overseas to look at the market from a local perspective to see if you have something saleable. “What kind of supply is there for a product like yours and at what price point? What kind of selection is there? This information will help you decide if it’s a market you can do well in,” the organization says.

That’s always sound advice but advice that requires either a strong knowledge of the local market, including competitors, or the offer of a unique product range that can’t be acquired elsewhere. One of the reasons that Etsy sellers have managed to promote themselves with such success outside their local markets is that their products are handcrafted and unique. Luxury brands have succeeded on a larger scale in markets like China because there are no local competitors to market who are as respected as Ferrari and Maserati or Luis Vuitton and Gucci. Uniqueness sells.

But in Pitney Bowes’ own ecommerce study, “availability” and “selection” were only the second and third reasons that it found consumers shopped outside their own countries. The most popular reason was price. If, even after adding the cost of delivery and any customs charges, you can still come in beneath local prices, you’ll have a product that can compete. That might not be as difficult as it sounds. Not all countries have open markets and many importers have exclusive contracts that allow them to cut out competition and keep their prices high. If your company can offer customers similar products at a competitive price, you can take their business.

10. AmericasQuarterly.com, India’s Middle Class (americasquarterly.org/indias-middle-class)

11. Telegraph.co.uk, Ashkey Armstrong, Online retailer Koovs woos India’s middle classes, January 11, 2016 (www.telegraph.co.uk/finance/newsbysector/retailandconsumer/12093202/Online-retailer-Koovs-woos-Indias-middle-classes.html)

It’s an option that’s been particularly successful in Israel where consumers who want to avoid paying local prices kept high by a lack of competition use courier companies like USAddress.com. The company gives them an American address (in fact, of their warehouses in New Jersey, together with an identifying code) which they can use to place orders for products that retailers like Amazon won’t ship abroad. The courier company then sends the purchase on to the buyer’s address in Israel. Demand for those services will be present for any product in any market for which there is little local competition, even goods that are relatively low value. Pitney Bowes’ survey found that the average order across all types of goods was around $120. “There is a lot of demand for lower value goods. This is especially true for Canada because shipping is relatively cheap relative to overseas markets.”

The best items to sell overseas are those with minimum competition and a price level high enough to make comparison shopping worthwhile but cheap enough to appeal to international middle classes.

In theory, businesses looking to sell beyond their local markets shouldn’t need to make any great efforts. As long as there are no geo restrictions on website visits, anyone should be able to find the company’s website, browse the products and place an order.

In practice, making sales abroad is far more complex. Two issues determine success: the ability to reach foreign customers; and the impression the business makes on them.

1. Understand Local Marketing Channels… Or Find People Who Do

Firms that have already been successful selling in their own markets may find that the skills and knowledge they have picked up in building their customer base are of little use when selling in foreign markets. An understanding of keywords, for example, is of little value when you’re selling in a different language or need to use Chinese characters instead of letters. Google, the most popular online advertising channel in much of the world, is not used at all in China and is barely used in Russia.

The first step for any business targeting an additional market then is to understand how people find the products and services they need in those markets. Which search engines do they use? What are the most popular social media sites for winning engagement and spreading information? How is word of mouth spread?

One solution available to retailers is to build stores on local shopping platforms and benefit from some of the traffic the mall should generate naturally. It’s a limited solution, however. Online malls usually rely on stores to do their own marketing, though the platform may be able to help with badges and banners. And it’s not an option in every market. Pitney Bowes’ survey found that a little over three-quarters of consumers in Russia, China and the U.S. would consider buying in online marketplaces. More than eight out of ten consumers in Australia, and more than seven out of ten in the UK and Canada, prefer to buy directly from the retailer’s own website.

An additional strategy may be to hand over control of those online stores and localized versions of a website to a local manager and to recruit local affiliates. If you lack a good understanding of local marketing techniques, find people who do and pay them a commission.

2. Localize Your Content

Finding the right marketing channels will only bring customers to look at your products. You then have to persuade them to buy, and that means talking not just a different language but using a different format. While buyers in the U.S. and the UK are used to reading customer reviews, buyers in China, for example, are accustomed to seeing multiple pictures of a product. And consumers in every market want to see visual imagery with which they can identify. The most common demands of stock photo agencies is for photos that use models of different ethnic backgrounds. If a business selling a product to Mexico uses pictures of people in its marketing, those people should look familiar to local consumers.

When you’re building localized stores or website sections, don’t just use the same imagery and change the language; change the imagery as well so that it matches the language and the customers you’re hoping to attract.

3. Practical Barriers

Businesses that sell long-distance might be trying to exploit the lack of a product or service in that market but they do face a number of in-built barriers. The most common complaints mentioned by long-distance buyers include shipping costs, additional fees at time of delivery, time to deliver, and the difficulty of returning products:

Selling to buyers in different countries isn’t always straightforward. Breaking into these markets can take effort and planning. It often requires a new approach to marketing but when the size of the opportunity is so large it’s always worth making the effort to find and target those additional customers.

When anyone is ready, willing and able to give you money, you should gear up and be ready to take that money and grow your business.

The days of the mom and pop stores might not be completely over but owners of small firms who know all their customers by name, have known them all for years—and can visit their homes after a short walk—have become rarer than ever. Big box stores have crowded out old-fashioned hardware stores, and every other type of store. The local place to get a coffee and a cake is more likely to be a Starbucks than a Marge’s Diner. Independent bookstores were beaten up by Borders and Barnes and Noble, and then killed off by Amazon. When local customers can buy anything they want online, without leaving their living room, location is no longer all it used to be for retailers.

It’s not all bad news though. While businesses that cater only to local buyers have come under pressure, it’s now easier than ever for even the smallest of firms to reach markets anywhere in the world. As residents of cities from Brazilia to Beijing have seen their incomes grow, these global customers now have the means to make the purchases they want from companies selling far away.

The result is that we’re now living with an entirely new opportunity, a world of global trade in which anyone can participate, selling to customers on the other side of the world, shipping products and taking payments.

For many businesses, this scenario is already happening. In 2014, eMarketer1 reported that for the first time, consumers in the Asia-Pacific region were set to spend more on ecommerce purchases than buyers in North America; consumers were on course to spend more than $525 billion in comparison to North America’s $483 billion. By 2017, the research company estimated the value of global ecommerce was likely to reach $2.357 trillion.

That’s a giant amount of money, and it means that businesses that choose only to trade locally are cutting themselves out of a much bigger market. For many businesses, there’s no reason to cut themselves out of anything anywhere. Shipping abroad might be expensive but if the product can’t be bought locally at all, customers will be willing to pay the extra delivery costs. In 2015, around 30 percent of Etsy’s $2.4 billion worth of sales were international2.

Of course, those sales aren’t always straightforward. International marketing may need some localization but it might only be a matter of finding local affiliates, translating a sales page or picking an additional geographic region. Local laws and customs may demand some changes but these laws are rarely an obstacle to international trade that can’t be overcome.

The same is true of accepting payments.

1. eMarketer.com, Global B2C Ecommerce Sales to Hit $1.5 Trillion This Year Driven by Growth in Emerging Markets, February 3, 2014 (http://www.emarketer.com/Article/Global-B2C-Ecommerce-Sales-Hit-15-Trillion-This-Year-Driven-by-Growth-Emerging-Markets/1010575#sthash.NEEDdgF9.dpuf)

2. Statista.com, International share of Etsy’s gross merchandise sales volume from 2012 to 2015 (www.statista.com/statistics/409373/etsy-international-gms/)

Today’s payment platforms, such as Due, now assume that clients will want to sell abroad, and they’re set up to accept multiple currencies from buyers in almost every location.

That digital payment platforms take international payments shouldn’t surprise anyone because the need for a way to make international payments is almost as old as trade itself. The island of Delos had little to recommend it to travelers but a temple of Apollo, but this island was able to generate wealth by offering credit transfers for clients across the ancient world whose accounts were kept up to date by a record of receipts. At a time when payments were made in cash consisting of bags of gold, silver and bronze coins, this island’s ability to make credit transfers may well have been the first instance of international banking.

Coins, made during the Roman period, have been found in locations as distant as Scotland and India, a sign not just of an enormous empire, but tells of a system whose merchants were able to trade beyond the borders of that empire.

And the hawala system used across the Islamic world dates back to the eighth century, allowing money to be deposited with an agent in one country then withdrawn from the agent’s partner in another.

For as long as trade routes have stretched beyond the forum—which is as long as trade has taken place—there has been a need for payments to be able to travel as far as the long distances the very travelers themselves have gone and to be able to be used in a way that’s fast, reliable and inexpensive.

In this guide, we’re going to explain not just how to accept those payments but who you should be accepting them from and what you need to know about trading in multiple currencies.

We’ll start by looking at the opportunities which have presented themselves. The rise not just of China but of all the BRIC countries (Brazil, Russia, India and China) has created giant new markets for sellers, all of which can now be reached easily through online marketing. We’ll explain which countries are the biggest buyers and we’ll explore what people in those countries are looking to buy.

We’ll then discuss the various ways in which payments can be made and collected overseas. There are lots of different methods of taking payments from customers and buyers in places as distant as Suriname and South Africa, so it’s important to understand the different options and know which option will be the best for your business.

We’ll also look at the risks involved in those payments. International payments can have long floats and when you’re shipping long-distance, dealing with disputes is much harder than working through a local legal system. We’ll look at the dangers in selling around the world, explain what you can do to lower the risks and show you why any remaining risk is far outweighed by the opportunity.

Finally, we’ll discuss exchange rates. When you’re taking payments in foreign currencies, you will have to deal with the exchange rates, a situation that can be a large opportunity as well as a small obstacle.

Selling internationally used to be impossible for small businesses. It’s now an opportunity for small businesses to reach out, and a chance to break into a giant market made up of happy customers all around the world. In this guide, we’ll show you how to turn a small firm into a global success.

In August 2015, Brendon Farley, an artist in Minnesota with an Etsy store, asked other sellers on the craft platform what percentage of their sales were international4. He had recently added a shipping profile for Canada after a customer in that country had asked for a painting, and had been surprised to find that most of his views over the last 30 days had come from north of the border.

“I get regular views from the USA, Canada, Australia, and Eastern European countries,” he said. “Really starting to wonder how much business I am losing.”

The post in the forum generated 45 responses, and the percentages ranged considerably. Just one person said that they made no international sales. A few, particularly those selling outside the United States, said that all of their sales were international while other percentages ranged from 2 percent to as much as 95 percent.

For anyone selling online, the market is definitely global and not merely local. Restricting business only to people with minimum shipping rates and no international borders means losing a great deal of business. The question isn’t whether a business can expand their sales, but rather, how much they can expand their sales? Which countries they should a company be targeting and what do these businesses need to do to reach buyers in those regions?

Sellers should be looking for buyers in every country that has people willing to pay for the goods or services that seller can produce, and from which the seller can accept payments in the currency of the country. But, some countries are easier targets than others.

A survey4 conducted in 2014 by Pitney Bowes asked around 12,000 people in twelve countries about their online purchases. Almost all of them (96 percent) had bought something online and as many as 40 percent of the buyers had bought goods from another country. Australians were the people most likely to import products they’d bought online, followed by Canada and Russia. Shoppers in South Korea, China, India and Japan were more reluctant, believing they could only purchase goods online from retailers in their own country. “But our research shows there is a significant opportunity in markets like Brazil, Germany and China,” the commerce company said. “And those markets – particularly Brazil and China – are growing at a much faster rate.”

While any country should be considered a potential target market, for the sake of ease, U.S. sellers can divide customers outside the United States into three regions.

1. English-Speaking Countries

Pitney Bowes, which helps companies expand internationally, notes that the biggest “U.S. cross-border growth engines are Canada, the UK and Australia,” all English-speaking countries. When there are no language barriers to overcome and few cultural differences that make products and

3. https://www.etsy.com/teams/7722/discussions/discuss/16673897/

4. 2014 Pitney Bowes Global Online Shopping Study

tastes formed in one country unattractive in another – those countries make up the easiest opportunities. There’s no need to translate sales pages. Customer services can be conducted directly and without using translations. Each side understands the other and knows exactly what to expect. With the exception of the delivery fees and possible custom charges, selling from the U.S. to Australia, the UK, Canada and even South Africa can feel as familiar and as straightforward as selling to Hawaii or Alaska.

For sellers in northern U.S. states, customers in Canada may be closer than those in the south, and Australia, in particular, suffers from a lack of supplies that makes imports attractive. The duty threshold of $1,000 AUS also makes most of those product imports duty-free.

2. European Countries

Not only do the UK, Canada and Australia speak the same language as the U.S. sellers, they also have similar standards of living, which means that a product aimed at average earners in the U.S. will be targeting a similar demographic in those other countries. The same language and standard of living is generally true in the countries in Western Europe, as well.

Pitney Bowes highlights Germany as one of “the most desirable e-destinations,” helped no doubt by its stable economy and thrifty customers. But other European countries, including France, Spain, Italy, Holland, Belgium and the Scandinavian nations should also be on the list of target markets. Those countries alone contain more than 220 million potential customers and have a GDP per capita ranging from around $30,000 in Spain to nearly $101,000 in oil-rich Norway.

A US-only retailer that can tap into those countries will have increased their market size by about two-thirds and be reaching people with similar spending power or even a higher spend growth.

3. BRICs

The most exciting market development over the last couple of decades has been the rise of countries whose populations traditionally had little spare cash, in particular Brazil, Russia, India and China. Between 1989 and 2016, China experienced GDP growth of 9.85 percent5 , a rate high enough to suck in Western brands as large as Louis Vuitton and Ferrari. Shopping malls in the tier one cities of Shanghai and Beijing are filled with the kinds of luxury goods that are more usually found in the best parts of New York or Beverly Hills.

But they’re also mostly empty. Although Beijing has now overtaken New York as the world’s billionaire capital6 , the average wage is still only around $8,655 a year and the average consumer spends only $7 every day, mostly on food and clothing. Americans typically spend $97 a day with nearly one dollar in five going to recreation. The numbers are changing quickly. McKinsey7 estimates that by 2022 more than 75 percent of China’s urban consumers will be earning between $9,000 and

5. TradingEconomics.com, China GDP Annual Growth Rate (www.tradingeconomics.com/china/gdp-growth-annual)

6. Bloomberg.com. Rachel Change, Here’s What China’s Middle Classes Really Earn — and Spend, March 10, 2016 (www.bloomberg.com/news/articles/2016-03-09/here-s-what-china-s-middle-class-really-earn-and-spend)

7. McKinsey.com, Dominic Barton, Yougang Chen, and Amy Jin, Mapping China’s middle class, June 2013 (www.mckinsey.com/industries/retail/our-insights/mapping-chinas-middle-class)

$34,000 a year. China may already have 109 million people with wealth of between $50,000 and $500,000 – a size that gives the country a bigger middle class than America.

This wealth has grown as the Internet in China has developed. According to eMarketer, about 16 percent ($672 billion) of all spending in China takes place online, of which about half is spent on mobile devices.

So preparing a pitch to a market in China, and you’ll be aiming at a lot of people with rapidly growing funds who are used to spending online. But you’ll also be dealing with a place where the normal online sales strategies just don’t work. Not only will you need to translate your content and deal with the fact that same day-delivery in Chinese cities has been common for more than a decade and costs very little, you’ll also be working in an environment that has none of the Internet tools you’ll be used to employing. Google, Twitter and Facebook are all blocked in China, together with the platforms they own. China’s online consumers search on Baidu.com, chat on WeChat, a mixture of WhatsApp and Twitter, and they buy on AliBaba. China might have a giant market with deepening pockets but reaching it is difficult.

There are some open doors though. AliBaba has an opening for foreign sellers on its Tmall Global property. (Macy’s used it to create their Chinese online store.) Jing Dong (JD.com) offers a similar service in the form of JD Worldwide, and different industries have their own dedicated platforms such as Suning.com for electronics.

Brazil and Russia each offers a very different challenge. While both countries appeared to be shaking off years of slow growth, both are now battling shrinking economies and smaller pay packets. Real average monthly incomes in Brazil have fallen from $568 in 2015 to $550 a year later. Russia’s monthly wages have stayed relatively stable at around 35,000 rubles over the same period but the value of the ruble against the dollar has declined by 50 percent since 2014, increasing the price of imports. The volatility of the ruble led Apple to stop online sales in that country.

But Brazil is the only South American country that eMarketer8 places in its top ten worldwide retail ecommerce markets, one place below Russia. About 5 percent of retail sales are made online, with fashion products and health and beauty aids together making more than a third of all purchases. Like China’s online market, Brazil too has large malls such as Deremate.com, Dereto.com and MercadoLibre.com, Latin America’s equivalent to Ebay. In 2011, Brazil’s government tried to choke orders made for goods outside Brazil by raising taxes on credit card purchases for cross-border purchases from 2.28 percent to 6.38 percent.

Russian officials have been more generous… but not much more. In 2014, the government agreed to continue not to tax products ordered from foreign retailers, provided the purchases do not exceed 150 euros in value or weight more than ten kilos. (Purchases above those limits are taxed at 30 percent.)9 That was better than hoped for, but it was a decline from a limit of 1,000 euros and 31 kilos. Like China, search in Russia uses a local site, Yandex, rather than Google, and payment is often in the form of cash on delivery rather than credit cards or secure payment platforms.

8. eMarketer.com, Brazil Ranks No. 10 for Retail Ecommerce Sales Worldwide, January 7, 2015, (www.emarketer.com/Article/Brazil-Ranks-No-10-Retail-Ecommerce-Sales-Worldwide/1011804)

InternetRetailer.com, Adrien Henni, Good news for online retailers selling into Russia, June 2, 2014 (www.internetretailer.com/commentary/2014/06/02/good-news-online-retailers-selling-russia)

While India has the advantage for US-based retailers of having an English-speaking population, the growth of its middle class has been slower than in China. McKinsey Global Institute10 defines India’s middle class as households with annual disposable incomes of between $3,606 to $18,031, and sees the numbers rising from 50 million in 2005 to over 250 million in 2015. By 2025, the organization expects it to reach 583 million, which is 41 percent of the population.

That’s a large income spread though, and making significant inroads can require a great deal of localization. Fashion store Koovs, chaired by Britain’s Lord Alli who also chairs retail chain Asos, grew its sales in India by 210 percent between mid-September 2015 and the start of January 2016 to reach £2.96 million11. The company used marketing that took its inspiration from India’s Bollywood movie industry. Smaller sellers can use platforms that include Flipkart.com, SnapDeal.com and Zepo.in but success in India will depend on a combination of choosing the kinds of unique products that can’t be bought locally and using careful pricing. Google’s search trends suggest that electronics, clothing and accessories are the most sought items online in India but local prices are low, so exporters will need to bring something unique to the market in order to land sales.

According to Pitney Bowes, the highest volume of cross-border purchases have been of luxury goods and brands, such as clothing, jewelry and shoes. As the cost of shipping has fallen, product categories have expanded so that auto parts are now being exported to Australia, for example.

This commerce company advises businesses considering expanding overseas to look at the market from a local perspective to see if you have something saleable. “What kind of supply is there for a product like yours and at what price point? What kind of selection is there? This information will help you decide if it’s a market you can do well in,” the organization says.

That’s always sound advice but advice that requires either a strong knowledge of the local market, including competitors, or the offer of a unique product range that can’t be acquired elsewhere. One of the reasons that Etsy sellers have managed to promote themselves with such success outside their local markets is that their products are handcrafted and unique. Luxury brands have succeeded on a larger scale in markets like China because there are no local competitors to market who are as respected as Ferrari and Maserati or Luis Vuitton and Gucci. Uniqueness sells.

But in Pitney Bowes’ own ecommerce study, “availability” and “selection” were only the second and third reasons that it found consumers shopped outside their own countries. The most popular reason was price. If, even after adding the cost of delivery and any customs charges, you can still come in beneath local prices, you’ll have a product that can compete. That might not be as difficult as it sounds. Not all countries have open markets and many importers have exclusive contracts that allow them to cut out competition and keep their prices high. If your company can offer customers similar products at a competitive price, you can take their business.

10. AmericasQuarterly.com, India’s Middle Class (americasquarterly.org/indias-middle-class)

11. Telegraph.co.uk, Ashkey Armstrong, Online retailer Koovs woos India’s middle classes, January 11, 2016 (www.telegraph.co.uk/finance/newsbysector/retailandconsumer/12093202/Online-retailer-Koovs-woos-Indias-middle-classes.html)

It’s an option that’s been particularly successful in Israel where consumers who want to avoid paying local prices kept high by a lack of competition use courier companies like USAddress.com. The company gives them an American address (in fact, of their warehouses in New Jersey, together with an identifying code) which they can use to place orders for products that retailers like Amazon won’t ship abroad. The courier company then sends the purchase on to the buyer’s address in Israel. Demand for those services will be present for any product in any market for which there is little local competition, even goods that are relatively low value. Pitney Bowes’ survey found that the average order across all types of goods was around $120. “There is a lot of demand for lower value goods. This is especially true for Canada because shipping is relatively cheap relative to overseas markets.”

The best items to sell overseas are those with minimum competition and a price level high enough to make comparison shopping worthwhile but cheap enough to appeal to international middle classes.

In theory, businesses looking to sell beyond their local markets shouldn’t need to make any great efforts. As long as there are no geo restrictions on website visits, anyone should be able to find the company’s website, browse the products and place an order.

In practice, making sales abroad is far more complex. Two issues determine success: the ability to reach foreign customers; and the impression the business makes on them.

1. Understand Local Marketing Channels… Or Find People Who Do

Firms that have already been successful selling in their own markets may find that the skills and knowledge they have picked up in building their customer base are of little use when selling in foreign markets. An understanding of keywords, for example, is of little value when you’re selling in a different language or need to use Chinese characters instead of letters. Google, the most popular online advertising channel in much of the world, is not used at all in China and is barely used in Russia.

The first step for any business targeting an additional market then is to understand how people find the products and services they need in those markets. Which search engines do they use? What are the most popular social media sites for winning engagement and spreading information? How is word of mouth spread?

One solution available to retailers is to build stores on local shopping platforms and benefit from some of the traffic the mall should generate naturally. It’s a limited solution, however. Online malls usually rely on stores to do their own marketing, though the platform may be able to help with badges and banners. And it’s not an option in every market. Pitney Bowes’ survey found that a little over three-quarters of consumers in Russia, China and the U.S. would consider buying in online marketplaces. More than eight out of ten consumers in Australia, and more than seven out of ten in the UK and Canada, prefer to buy directly from the retailer’s own website.

An additional strategy may be to hand over control of those online stores and localized versions of a website to a local manager and to recruit local affiliates. If you lack a good understanding of local marketing techniques, find people who do and pay them a commission.

2. Localize Your Content

Finding the right marketing channels will only bring customers to look at your products. You then have to persuade them to buy, and that means talking not just a different language but using a different format. While buyers in the U.S. and the UK are used to reading customer reviews, buyers in China, for example, are accustomed to seeing multiple pictures of a product. And consumers in every market want to see visual imagery with which they can identify. The most common demands of stock photo agencies is for photos that use models of different ethnic backgrounds. If a business selling a product to Mexico uses pictures of people in its marketing, those people should look familiar to local consumers.

When you’re building localized stores or website sections, don’t just use the same imagery and change the language; change the imagery as well so that it matches the language and the customers you’re hoping to attract.

3. Practical Barriers

Businesses that sell long-distance might be trying to exploit the lack of a product or service in that market but they do face a number of in-built barriers. The most common complaints mentioned by long-distance buyers include shipping costs, additional fees at time of delivery, time to deliver, and the difficulty of returning products:

Selling to buyers in different countries isn’t always straightforward. Breaking into these markets can take effort and planning. It often requires a new approach to marketing but when the size of the opportunity is so large it’s always worth making the effort to find and target those additional customers.

When anyone is ready, willing and able to give you money, you should gear up and be ready to take that money and grow your business.

The rewards that follows the effort of marketing to foreign buyers and persuading them to buy, perhaps in a foreign language and with localized marketing, is additional certainly income, and it can be big income. Fortunately, collecting that income is easier than it sounds. While a businesses might need to expand beyond their current forms of payment methods, every business now has the opportunity to take payments in multiple currencies, from multiple countries and in a number of different ways:

The problem for global sellers is that many payment processors regard international payments as a greater risk of fraud and more likely to result in chargebacks. They either refuse to accept overseas payments or they charge higher fees to cover the risk. PayPal, for example, doesn’t charge its customers for sending personal payments from one U.S. account to another U.S. account using a PayPal balance or bank account, and transfers made using a debit or credit card are charged a flat rate of 30 cents plus 2.9 percent of the transferred amount. But PayPal’s cross-border fees are much higher. The kind of personal payments that would be free within the U.S. cost between 0.5 and 2 percent of the transferred fee when the money crosses a border. If the transfer is made using a credit or debit card, the fees can rise as high as 7.4 percent. International purchase payments cost 3.9 percent plus a fixed fee that’s based on the currency of the payment. And if all that’s not enough, the company also warns that it might charge additional fees to perform a currency conversion and the card owner’s financial institution may have its own fees as well.

In addition to charging higher amounts to cover the costs of delivery, international sellers sometimes have to decide whether to add more for the extra payment charges or absorb the losses and cut their profits.

But those costs aren’t universal. Even payment platforms that work with major credit card companies have leeway to reduce the fees for customers. Due’s international payments, for example, cost a flat 2.75 percent of the transaction price—far lower than the amounts charged by PayPal.

Even if a company is willing to absorb additional costs, taking payments from some countries using the same platforms is rarely as simple as they claim. PayPal does have a Chinese franchise that accepts UnionPay cards, for example, but payments have to be made with a dual currency card, which few Chinese own, or the buyer needs to verify their identity with PayPal so that the company can track the flow of funds and ensure that buyers don’t breach their $50,000 annual outflow limit.

China’s online customers are more accustomed to using AliPay, a local clone of PayPal owned by AliBaba, the country’s biggest Internet company. It does have an international department capable of taking payments on behalf of foreign companies but when Kyle Chen12 , owner of a small online store, called the company to find out how he could use it, he was given a long list of requirements. Accounts can only be opened by registered companies. The CEO must sign some documents and send over a pile of profile papers. If they’re approved, they’ll receive access to a special AliPay

12. https://www.quora.com/Whats-the-best-way-to-accept-payment-from-China

account after a “few weeks” but that account cannot be touched by the owner. When funds in the account reach $5,000, AliPay wires the funds automatically. “It’s impossible for small [sic] business online shop to use Alipay unless you’re Chinese market turnover is $250k+,” Chen concluded.

A payment platform that can handle payments, is accessible on mobile devices, doesn’t charge enormous fees, and is easily integrated onto localized Web pages may well be the easiest way to solve the problem of accepting money from customers overseas, but there are alternatives.

Wire transfers is probably the most secure way to send funds from one bank account to another but typically costing around $30, they’re too expensive for most B2C payments. These transfers also can’t be refunded which makes settling disputes difficult. A customer buying a product large enough to make the transfer fee worth paying is likely to balk at sending those large sums through a channel that gives them no dispute resolution and leaves them hoping that the product is on its way from a seller in a foreign country.

Wire payments may be suitable for some types of one-off B2B payments but they’re rarely a good, scalable solution for a retailer looking to pick up new customers abroad.

Personal checks are still a surprisingly popular way to settle B2B payments. Around half of all business invoices are said to be settled with checks but that figure may rise to as high as 90 percent for small firms. Although using checks is relatively cheap, they’re slow and have a high risk of fraud. Marketplaces usually restrict the use of checks. eBay, for example, prohibits the use of both checks and wire transfers to settle payments for all products other than vehicles and industrial equipment. For small businesses selling the kind of $120-products that sell best across borders, waiting for a personal check that might have been written in a different currency is an impractical way to do business.

For major international purchases by large companies, letters of credit are one of the standard ways of making payment. Supplied by banks, a letter of credit guarantees to a seller that the payment will be made on time and in full. If the buyer is unable to make payment, the bank will have to make it, bringing complete security to the seller and enabling them to release the product. The bank does not release the funds until it receives confirmation that the products have been shipped.

The process of acquiring a letter of credit can be complex, especially for small business. First, the buyer and seller agree a deal, and the seller demands a letter of credit to guarantee payment. The buyer applies to their bank, and the buyer’s bank checks the client’s credit risk before sending the letter of credit to a correspondent bank usually in the same geographical region as the seller. That correspondent bank checks the credit note and forwards it to the seller. The seller then ships the goods and presents evidence to the correspondent bank for payment processing. If all the paperwork is in order, the correspondent bank pays the seller and recoups the funds from the bank that issued the letter of credit, which in turn takes it from the buyer.

13. AmericanBanker.com, BC Krishna, Check Please! The Future of B2B Payments, September 30, 2015 (www.americanbanker.com/partnerinsights/check-please-the-future-of-b2b-payments-1077019-1.html)

It’s a long and complex process, and one that can run into a large range of different problems. Delays can invalidate the letter of credit, as can mistakes in the description of the goods, a lack of detail in the invoice, changes to delivery dates, and a whole host of other issues. Banks have no freedom to negotiate on behalf of buyer or seller.

Letters of Credit can also be expensive. They can rack up multiple fees depending on the size of the guarantee and its terms. Rates are typically 0.75 percent for letters of credit in excess of $100,000 but can rise to 1.5 percent in developing countries. Buyers and sellers can expect to have to dole out a dozen more fees to the banks for authenticating, sending and receiving the letter of credit; for examining the letter; for any communications between the banks; and for a host of other issues. Letters of credit have long been a bank’s bread and butter and they know very well how to earn from it.

For big companies ordering machine parts and bits of jet engines, letters of credit are a familiar part of the business process. They’re not going to write checks for six or seven figures and they want to be certain that the transfer of the payment matches the issuance of the goods. But unless you’re in the business of selling locomotives, planes or weapons, the banking system’s international payment process is likely to be too expensive and difficult to function as a solution.

Credit (and debit) cards may well be the most convenient way for customers to make purchases. The customer is already used to entering card numbers onto websites and cards are fairly easy to use. But not only do credit card companies charge fees for their use, different companies also have different rules regarding their use in international payments. Retailers that want to offer credit card payments on their websites will always be forced to work around the rules of the credit card companies.

In practice, those rules may be acceptable, though expensive, in countries like the UK, Australia or Canada, but try selling to the larger markets in developing countries, and the rules can become prohibitive, and even unreliable. In 2014, Visa and Mastercard stopped processing some Russian transactions in response to sanctions imposed by the U.S. government following Russia’s invasion of Crimea. The move only affected the credit card companies’ operations with four banks and may also have had relatively little effect on purchasing. According to Euromonitor International14, Russia’s population of 143 million has just 30 million credit cards between them.

Credit card payments in China have become less complex—and possibly too simple. UnionPay is the country’s only credit card network. The organization has brokered agreements with Visa, Mastercard and other major credit card companies to allow its cards to be used abroad, and they can now also be used for ecommerce and in card-not-present payments.

One of the biggest changes to hit payment systems over the last few years has been the rise of mobile payment systems. Venmo has become the default method for young people to send each

14. Bloomberg.com, Carol Matlack and Elizabeth Dexheimer, Russia Gets Ready for Life Without Visa and MasterCard, March 24, 2014 (www.bloomberg.com/news/articles/2014-03-24/russia-gets-ready-for-life-without-visa-and-mastercard)

other small amounts of money using their mobile phones. Google offers a similar service with Google Wallet, and even social media platforms like Facebook and Snapchat now allow their users to send each other cash.

While those platforms have began to grow in popularity (Venmo, which is now owned by PayPal, processed $1 billion in January 2016 alone), they also reveal the difficulty of taking international payments. None of them allows users to send money across international borders.

The reasons for these restrictions have more to do with measures against money laundering than the technical difficulties of making international transfers but the features that have attracted users to applications like Venmo would be equally attractive to consumers. Located on mobile phones, they’re easy to use, trusted and the payments are almost instantaneous. They’re also currently unavailable to buyers looking to make cross-border purchases.

When Australian entrepreneur Craig White told the BBC and a small number of other media outlets that he was Satoshi Nakamoto in May 2016, it looked like the creator of Bitcoin, the world’s most successful cryptocurrency had finally been revealed. He offered proof, which was disputed, so he promised to show more… only to pull out at the last minute, saying that he just couldn’t do it.

The continuation of the mystery hasn’t done Bitcoin itself any harm however. The cryptocurrency continues to be used, and although there are no accurate data that reveal the number of people who own Bitcoin, rough estimates on Reddit put the figure between one and three million15.

Backed by no country’s central bank, the digital currency is becoming a common a popular method of payments and should be an ideal solution for making international payments. People who own bitcoins can indeed make payments from anywhere in the world, and the currency is most popular among the high-tech firms that have set up shop in the hubs of Bali.

Kyle Chen noted that when he asked Chinese buyers to pay through PayPal International, more than 90 percent failed to complete the transaction. This shouldn’t surprise anyone. Tell a customer that the money they’re accustomed to using isn’t good enough and few people will be willing to look for an alternative and an unfamiliar method. When customers buy online, their only concern about the location of a seller should be the cost of delivery and the time it will take for the product to reach them. Customers don’t want to wonder how they can send their money to a retailer on the other side of the world and they don’t want stop to ask if some new method of payment is safe and secure.

If a person is used to entering their credit card details into secure payment forms on websites, that’s the method they want to use. For retailers wondering which of the multiple methods of accepting international payments is the best, the easiest solution remains a payment platform that can accept the most common cards internationally at a rate that is fair and equitable, won’t eat into their profit margins and doesn’t gouge them for looking to expand their market.

15. https://www.reddit.com/r/Bitcoin/comments/3yrr9z/estimating_number_of_users_some_ideas/

Even those methods, though, will entail some risk. In the next chapter, we’ll look at the most common dangers for both buyers and sellers of taking international payments… and explain how to reduce them.

In May 2015, “searchingforgoodies” posted a message on the forum of Etsy:16

I have bought an item from the U.S. I want to return it for a refund but the seller is refusing.

As I’m in the EU my consumer rights say I am entitled to return an item up to 14 days for a full refund.

How can this be enforced?

The post triggered around two dozen responses but produced very little usable clarity. The first response argued that EU consumer rights could not be enforced outside of the Union, and that U.S. law and Etsy’s own terms and conditions allow the site to set its own policies. “searchingforgoodies” responded by digging out a couple of paragraphs from Etsy’s Help pages that told sellers they needed to abide by the EU law if they were selling to buyers in the Union:

The regulations… apply to all Etsy sellers who sell to buyers in the EU (even if an Etsy seller is based outside of the EU) and buyers based in EU member countries … Failure to comply with these regulations can invalidate a sale and possibly even violate the law.

Worse, sellers affected by those regulations were also supposed to “clearly inform” buyers about their rights before they made their purchase. If they didn’t, instead of having fourteen days to make a return, the buyer would have a year and fourteen days.

The response to that post was mostly head scratching. No one seemed entirely sure how a buyer in the EU could enforce the regulation and require a seller in the U.S. to issue a refund. Some people argued that buyers would still have to pay their own shipping so a return is unlikely to be worth even requesting. One commenter in the UK said that the consumer advice in her country was that EU rules aren’t applicable outside the Union, and another noted that regardless of the law’s meaning, it adds costs to sales which eat into margins. At least two of the commenters stated that the rule, which no one seemed to really understand, was why they had stopped shipping to Europe entirely.

Selling always carries some risks. Buyers might demand a refund. Payments might not be processed. Credit cards can receive a chargeback, and the seller might not be able to follow through in the way that they thought they would be able to, generating bad reviews and feedback. But those risks are multiplied when sales are made across borders. Not only does the seller have to cope with the extra costs of shipping and sometimes insurance, they also have to know about local customs charges, about any local legal restrictions on the products they want to sell, and about local consumer laws. (Even if those laws aren’t applicable in the seller’s country, they will form part of the expectations of the buyer.)

Solving those problems will usually require no more than a little reading and some research. At worst, you might have to adapt the product slightly to make it compatible with local laws although

16. https://www.etsy.com/teams/7718/questions/discuss/17760012/page/1

it’s more likely that you’ll have to adapt your pricing or profit margin to take into account the added costs.

But selling internationally brings in two additional and very special risks.

All sellers have to be concerned about the failure of customers to make their payments. Checks can bounce, credit cards can be charged back, even ACH and wire transfers can be reversed and the money returned. Complaints are rare and fraud is even rarer, but both do happen, and they can hit any business.

When the unfortunate risks show up and happen within a national jurisdiction, sellers and buyers can make use of a legal system established to ensure that trade can be conducted easily and contracts can be enforced. When one of the partners to a trade is in a different jurisdiction however, enforcing the contract becomes much harder… and much more expensive. The seller might have to find a legal firm in the buyer’s country, or one familiar with that country’s legal code. Even with a contract for a large purchase or terms and conditions that lay out exactly where and how a conflict should be resolved actually enforcing those conditions is particularly complex for international sales.

And there’s much more room for conflict to happen when shipping across borders.

In every transaction, the buyer would prefer to receive the product, use it and ensure that they feel entirely satisfied that it meets their needs before they hand over their payment. Similarly, the seller would prefer to receive the payment in full before shipping the product and hoping the customer likes it. Brick-and-mortar stores have an easy solution: customer can handle the product, test it or try it but they have to hand over payment before they can take it away. There’s no standard corresponding purchase process for international shipping. Sellers usually demand payment in advance, promise to ship as soon as they receive it, then require the buyer to wait, sometimes for weeks, until the product reaches them.

That sounds as though all the advantages are with the seller. But once the product has left the warehouse, they no longer have control over it. The buyer will usually receive a message informing them that the product is on the way… and they can then use the delivery time to cancel the check or demand a chargeback on their credit card. The payment processor may issue the refund but the seller will be powerless to pull back the product.

When it comes to international payments, there’s more time for buyers to withdraw their payments and fewer options for the sellers if they do.

Companies closing large contracts in developing countries have to take country risk into account. An agreement to build an oil well in Nigeria might only have force as long as the current government remains in power. It took Netflix years to negotiate the rights that would enable it to start allowing subscribers to stream movies and television shows in Europe… only to be met with a protectionist demand for 20 percent of the content on the platform to have been made in the EU.

For retailers selling jewelry or clothing to buyers in France or Canada the risks are much lower… but they’re not zero. The laws surrounding the sale of antique artworks made of ivory, for example, are complex and constantly changing. (Sellers of objects made of African-elephant ivory need documentation proving that the ivory was harvested before 1976 or imported before that year but importing countries will also have their own regulations.) The item most commonly confiscated from visitors to the U.S. isn’t drugs or guns… it’s Kinder eggs. The chocolate eggs with a children’s toy inside are banned from sale in the U.S. as a choking hazard. In 2011, U.S. Customs and Border Control confiscated 60,000 of them from travelers who could be slapped with a $2,500 fine17.

And in 2010, Danish customs authorities seized a watch ordered on a Hong Kong website in the belief that it was a counterfeit Rolex. The buyer opposed the destruction of the watch but the European Court of Justice found that under customs regulations, owners of intellectual property are protected against the sale of fake goods to residents of the EU from websites outside the Union. The brand owners don’t need to prove that the suspected goods were advertised or offered specifically to those buyers.

Again, unless a seller is exporting handbags marked “Louis Vuillon,” it’s unlikely to be an issue. But an exporter whose products are similar to those created by a well-known brand, whether they’re t-shirts, iPhone covers or watches, would have to deal with the additional risk that a zealous customs official could seize the package and destroy the contents.

So all trade carries some risk and expanding to international markets increases those risks. The cross border trade makes dealing with disputes harder, increase the chances of fraud and misunderstanding, and these sales expose the seller to laws and regulations that they might not be aware of.

None of these risks is prohibitive. A slight rise in risk is not the same as a prohibition or a prevention of a sale. It just means that instead of a tiny chance of a loss on a particular trade there’s now a very small chance of a loss on a sale.

And there are things that you can do to keep those slightly increased risks to a minimum.

The first consideration is that you need to do the research.

Know the consumer laws in each of the countries that you’re selling to. You don’t have to become a commercial lawyer—or hire one—but you should be aware of what buyers expect when they make a purchase, and whether there are any laws governing the sale of the products you sell.

17. Yahoo.com, Thomas Bink, Seattle pair detained for smuggling Canadian contraband – Kinder Surprise eggs, July 18, 2012 (ca.news.yahoo.com/blogs/daily-buzz/seattle-pair-detained-smuggling-canadian-contraband-kinder-surprise-204518469.html)

You should know about any customs fees or duties that the importing country might levy. You might well find that the cost of customs effectively prices you out of the market. That is, after all, their point. Better to know before you begin marketing than after you’ve already paid the translator, the Web page designer and the advertising program.

You should also understand the market. You probably already know the main competitors in your current market but a foreign market may well have different sellers with different pricing and different features. There are likely to be some costs in expanding your marketing to new countries, even if it’s just the cost of editing a Web page, so you should know who you’ll be competing against before you make those investments.

If you offer insurance during your deliveries, you’ll want to talk to the insurance company about their rates for longer distances and the higher risks of cross-border trade. You should also know about delivery times so that you can tell buyers when they can expect their goods, and try to find different options that might be faster or cheaper.

The biggest issue, though, will be the payment risk because it’s the hardest one to reduce. Before you start selling internationally, you should have a plan to handle demands for refunds and to cope with failures to pay.

In general, the best strategy for any business looking to make sales, especially online, is to have a generous returns policy and let everyone know about it. There’s a reason that so many companies offer money-back guarantees and promise 100 percent satisfaction: every buyer’s biggest fear is that they’re going to buy something they regret and will feel that they’ve wasted their money. Declaring that you’re always prepared to hand back the funds if the customer isn’t happy goes a long way towards resolving those doubts.

For international sales, those promises make life easier for the seller and they’re also cheaper to make than they might be for domestic sales.

If you’ve decided that there are few situations in which you wouldn’t offer a refund, then you don’t have to worry too much about local consumer laws; your own policy is likely to be more generous. But if you also make clear that buyers have to return their purchase in order to obtain that refund, your offer looks fair but becomes difficult to implement in practice. Even the EU’s laws require an unsatisfied buyer to pay for their own postage in order to claim their refund. Tasked with boxing up their purchase, taking it to the post office, paying for the shipping and waiting for the package to reach its destination before they can get their money back, many (though not all) unhappy buyers will let it slide.

Inevitably though, there will be times when a customer will complain that they didn’t receive the product or claim that it wasn’t as described or say that they did send it back even though you didn’t receive it, and they’ll kick up such a fuss that you just want the problem to go away. And occasionally, there will credit card chargebacks or failures to pay that only become clear after you’ve already shipped.

One strategy is to consider those occasional losses as part of the cost of doing business. Count how frequently you decide to make exceptions to your return policy and how often you choose to pay a refund on demand in order to stop complaints, keep a customer happy and build trust with other potential buyers. Make sure that it’s not happening too often, and factor the costs into the price of your product.