Whether you’re ready or not, we’re quickly approaching 2017. In a few weeks, we’ll have a new president, but also a new set of tax laws and codes that will influence how we conduct business.

Since it’s always best to be well-prepared when it comes to taxes, here are some of the new changes that you should be aware of. As with anything to do with the government or taxes — if you really want to stay-top of this information, meet with your tax advisor and frequently check for updates on IRS.gov.

Keep in mind, this isn’t legal advice as I’m not in the legal space. This post is new tax laws for 2017 that I’ve noticed that business owners should pay attention too.

Section 179 Expensing/Bonus Depreciation

Under Section 179 of the tax code, explains Brian McCuller, JD, CPA, “the expensing provision allows capital investments of up to $500,000 for certain property to be taken as an expense deduction — rather than being depreciated break — which was made permanent under the PATH Act passed at the end of 2015 — phases out for asset purchases above $2 million.”

Additionally, HVAC units are now eligible for as an expense deduction instead of depreciation in tax years beginning after Dec. 31, 2015.

“The bonus depreciation provision allows businesses to claim additional depreciation for certain property in the first year of the recovery period. If placed in service from 2015 to 2019 (with an additional year for certain property with a longer production period),” adds McCuller. “For property placed in service in 2015, 2016 and 2017, the bonus depreciation is 50 percent. 2018, it drops to 40 percent; 2019 it goes to 30 percent.”

Let’s say you purchased or leased new hardware or software for your business. You can depreciate half the cost as part of “bonus depreciation.” For 2017, it may be in your best interest to invest in the most up-to-date equipment possible.

Tighter Filing Deadlines

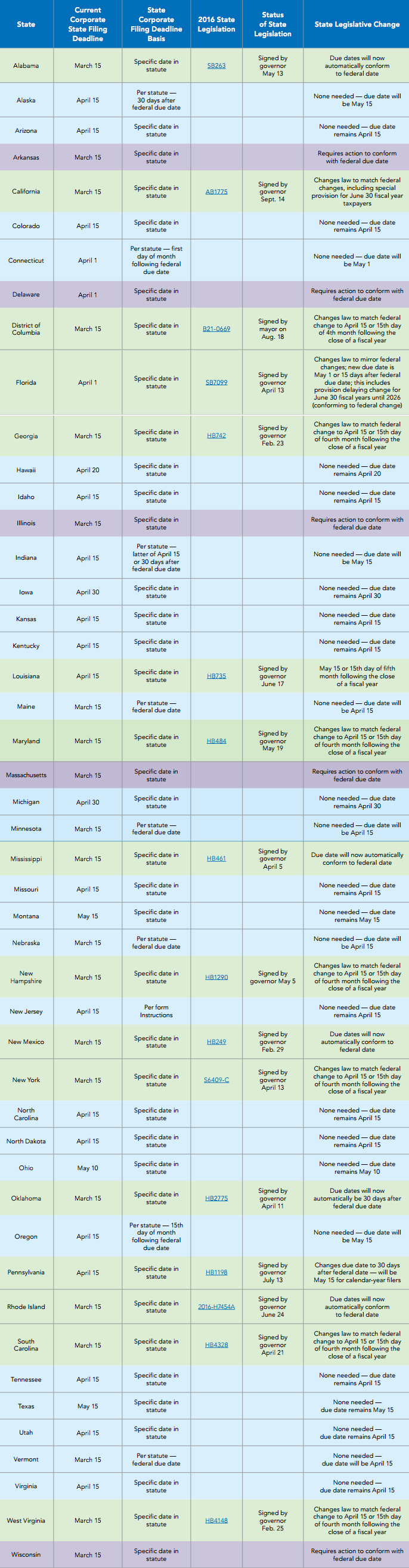

Filing deadlines have been changed so that flow-through entity return deadlines are due prior investor return deadlines. This means that partnerships and S-corporations operating on a calendar year will have a new deadline of March 15. The deadline for calendar year based C-Corporations will be pushed from March 15 to April 15.

Below is a the complete list of changes to deadlines for each state.

Furthermore, if your business provides health benefits then please note that the deadline for Form 1095, which is the proof of insurance coverage, will be on January 31. Also take note that hard filing deadlines have been imposed for Forms 1094-B and 1095-A, B, and C.

These are due by February 28 by mail or by e-file on March 31.

New Partnership Audit Rules

Effective in 2018, partnerships could be liable at the entity, as opposed to partner level for audit-related tax collections. This change will have a significant impact on how partnership interests are valued and transferred.

Because they’re also so complex, it’s best to speak to your tax advisor for additional information.

Expanded Eligibility for R&D Tax Credit

Until the PATH Act, the development of internal use software was not eligible for the research and development tax credit.

Organizations, particularly in construction, software, manufacturing, wine, aerospace subcontracting, boat building, and biotech, can qualify for this credit. They can qualify if they have engineers, scientists, or product development personnel on staff.

Other qualifications include software that is innovative and can be commercially sold.

Tom Sanger, a partner with accounting and advisory firm Moss Adams, says that “small businesses, now defined as having an average of less than $50 million in gross revenue over the prior three years. This will be able to offset (the alternative minimum tax ) AMT with R&D credits generated after Jan. 1, 2016.”

“This provision opens up the credit to small corporations subject to the AMT, as well as pass-through entities. Where the credits flow through to shareholders.” Sanger adds. “In the past, these credits were suspended and carried forward for up to 20 years until they were no longer subject to the AMT.”

Pending Estate Planning Changes

“The IRS has proposed changes in the rules for how minority stakes in family-owned businesses are valued when owners transfer interests to the next generation during their lifetimes,” explains McCuller.

“The changes have not been finalized, and business owners who have been considering passing along part of their ownership interests may want to consult with their tax advisors about accelerating those plans to take advantage of current rules.”

Possible Tax Laws Under President Trump

In addition, business owners should also pay attention to the tax laws that may take effect under President-elect Donald Trump.

For starters, “The Trump plan would reduce the corporate tax rate from a maximum rate of 35% to a rate of 15% (the GOP Blueprint calls for a US corporate rate of 20%),” says accounting, tax and consulting firm Elliott Davis Decosimo.

Also, “US manufacturers would be able to fully expense new plant and equipment investments. Though by doing so would forego any deduction for net interest expense.

“Most tax credits, other than the research credit would be eliminated. US taxpayers with foreign subsidiaries would be a one-time deemed repatriation tax of 10% on foreign earnings of those subsidiaries.”

This could have major tax consequences for small businesses. In fact, Trump’s tax reform will most likely benefit the wealthy and large corporations as opposed to SMBs.

When it comes to healthcare, Trump plans to repeal the ACA. According to an article in Fortune, “That could include changing regulations to let states buy and sell insurance across state lines.” The article goes on to state that Trump “favors giving individual consumers access to federal health savings accounts, and making monthly premium payments fully deductible at tax time.”

Small business owners may also want to pay attention to changes in immigration, regulations, and trade agreements under President Trump. Even if they don’t’ strictly apply to taxes, they could have major implications for your small business.