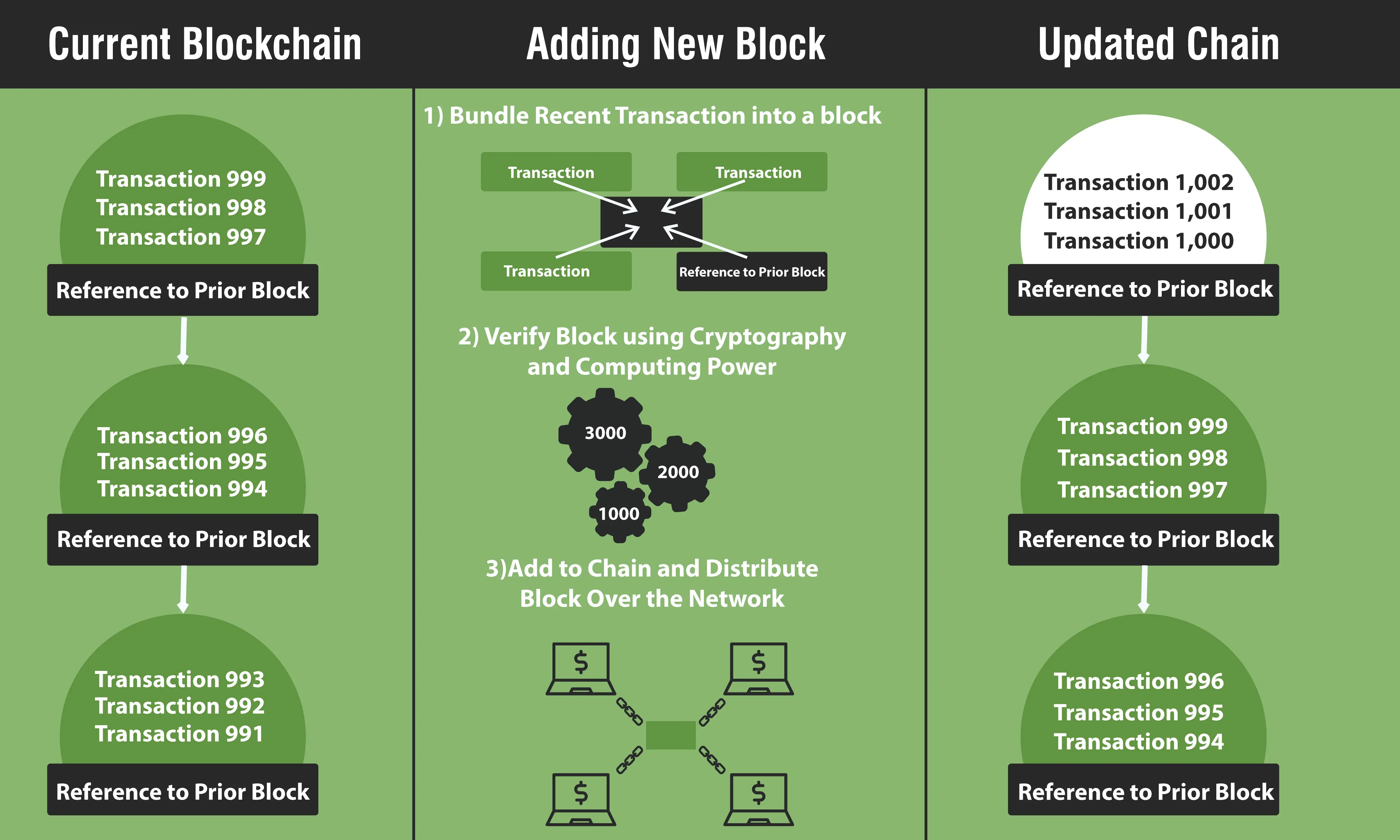

If you are familiar with the term “blockchain” then you are ahead of some people. Blockchain uses cryptography to create a digital record of transactions. These monetary exchanges are secure because they are decentralized. To put it more simply, transactions involving money are secure through their code and because they are done over multiple computers instead of just one. By its very nature, blockchain could save your business money. Here’s how.

Table of Contents

Toggle1. Deters Theft

The first way blockchain could save your business money is through deterrence of thievery. Cash is easy for thieves to steal and so are some credit and debit cards because they can be easily hacked. In addition, if your business accepts checks, they can be forged by people out to steal your products or services.

Digital currency through blockchain, however, is not so easy to steal. What does this mean for your business?

If transactions with your customers are made through blockchain your business may not experience as much theft. Monetary exchanges through blockchain can’t be forged easily. This equals increased savings for you and your business due to less loss of money and products or services.

2. Reduces Banking Fees

There are some people who feel that using blockchain could eliminate public need for banking altogether. Certainly it can eliminate or greatly reduce the amount of money your business pays in banking fees.

When financial transactions are made without the need for a centralized server or bank you essentially skip the need for their services altogether. Instead of having to pay transaction fees or banking fees each month you can keep that money in your business.

Over the fiscal year of your business, not having to use a bank to exchange money could save hundreds if not a thousand dollars or more.

3. Lowers Taxes

Blockchain can enable you to lower the tax liability of your business. Through blockchain transactions you may decide to accept cryptocurrency as a form of payment, for example.

In turn, cryptocurrency is not recognized as money by the IRS. Therefore, any cryptocurrency you have is not taxable in the same way as money. Check with your tax preparer and financial professional before deciding whether or not to accept cryptocurrency payments using blockchain technology in your business.

4. Blockchain Save Your Business because it Saves Time

Transactions using blockchain do not take the same amount of time as credit card transactions. They are nearly instant where credit card transactions can take several minutes.

Because blockchain information is not stored at a financial institution your computer, cash register, or credit card machine no longer has to exchange information with a bank. There is no back and forth between your system and a bank’s before exchanges can be accepted and completed.

The amount of time this saves your business means increased productivity and less cost for you.

5. Other Reduced Costs

Other ways blockchain can save your business money is through fewer supplies overhead. You may be able to go paperless with your business when it uses blockchain technology.

There is no need for digital printouts when you use blockchain. All of the information you need can be accessed electronically. This eliminates the use of paper and ink and therefore reduces the costs to your business.

As you can see, there are many ways blockchain can save your business money. Very likely if you are not already using blockchain you might end up considering its use in the near future.