As I’ve said a thousand times before: I love Roth IRAs. In fact, when entrepreneurs ask for my advice on how to secure their future financial security, I always recommend they open a Roth IRA as soon as possible.

It all boils down to two words: tax-free. If you invest after-tax dollars today, your money grows tax-free and can be withdrawn tax-free in retirement. By locking in a lower tax rate now, you effectively lock in a lower tax rate later in life if you plan to climb the ladder.

Despite this, 44% of U.S. households had an IRA at mid-2025. Most households had traditional IRAs (33%), followed by Roth IRAs (28%). Almost all of these families maintained employer-sponsored retirement plans in addition to their IRAs.

Roth structures, however, offer unique operational flexibility. To begin with, you can withdraw your original contributions at any time, penalty-free and tax-free. Moreover, Roth IRAs are not subject to Required Minimum Distributions (RMDs), unlike traditional IRAs. When you take money out, those tax-free withdrawals supplement your income without putting you in a higher tax bracket or increasing Medicare premiums.

Despite this, a staggering number of people ignore this strategy. I’ve found that the most common reason is not a lack of capital, but a lack of direction. In the financial industry, dozens of financial institutions claim to be the best, and the paradox of choice paralyzes beginners into inaction. Let’s eliminate guesswork. In my experience as a financial planner and investor, I’ve compiled a list of the six best Roth IRA accounts for beginners, organized by style, along with my all-time favorite.

1. The Institutional Powerhouse: Charles Schwab

A lot of people prefer doing everything through an app on their phone. Others feel more at ease discussing their money with a living, breathing human being. As such, Charles Schwab offers a classic, hands-on relationship along with the latest technology.

Since its founding in 1971, Schwab has become one of the world’s most respected discount brokerages. After acquiring TD Ameritrade in 2020 and merging with it in 2023, they became an industry powerhouse.

Schwab operates as a traditional, self-directed brokerage firm. They provide the infrastructure, but you manage the portfolio. Unless you specifically opt into their separate robo-product, they do not auto-invest your money for you; you log in, search for a ticker symbol, and execute the trade yourself.

Together, the two legacies boast more than 400 physical branch locations across the country. Using their branch locator tool, you can easily find an office near you by typing in your ZIP code. With a $0 minimum deposit, you can open an account today even if you only have $5 to spare. The best part is that online stock or exchange-traded fund (ETF) trades cost you nothing, giving you a huge range of low-cost options.

2. The Algorithmic Optimizer: Betterment

Alternatively, we have investors who do not want to choose individual stocks or rebalance their portfolios. When analyzing market charts makes you itch, you need a robo-advisor. Betterment is the solution.

Betterment uses automated algorithms based on Modern Portfolio Theory to handle the heavy lifting. In this case, you do not buy individual shares of specific companies. Instead, their algorithm uses a fixed basket of highly liquid, low-cost index ETFs to determine a risk-adjusted asset allocation based on your age and your goals.

When you sign up for Betterment, it asks you basic questions like what you are saving for, when you want to retire, and how much you can save each month. Using your timeline, they automatically build and maintain a diversified portfolio divided among twelve specific asset classes, mainly taking advantage of massive Vanguard and iShares funds.

Dividend reinvestment and portfolio rebalancing are handled automatically, so you don’t have to do anything. With fractional shares, Betterment breaks down your deposit into tiny pennies and distributes them across all funds instantly in a way that preserves your target asset mix. For managing your money, traditional financial advisors typically charge one to two percent of your assets annually. Betterment charges a quarter-percent annual management fee on your balance, billed on a monthly basis at roughly two hundredths of a percent of your balance. As long as you maintain a dollar balance in your account, it’s exceptionally affordable and accessible.

3. The Real Estate Syndicate: Fundrise

Most people associate Roth IRAs with Wall Street. But what if real estate is your true passion? In the past, buying real estate inside an IRA required setting up a complex, expensive self-directed custodian account. The script has been completely flipped by Fundrise.

With Fundrise, you can pool money with other investors to buy institutional-grade commercial and residential real estate through electronic Real Estate Investment Trusts (eREITs) and private placement funds. Fundrise bypasses Wall Street entirely.

Since investing with Fundrise over five years ago, my favorite feature has been the sheer transparency. The app shows me a map of the exact physical buildings my money is helping purchase, such as an apartment complex. When viewed in the context of their historical client returns, Fundrise portfolios have shown remarkable stability even during turbulent market cycles because real estate provides excellent diversification away from stock market volatility.

As a result of physical property management and a specialized self-directed structure, Fundrise IRAs charge a one-percent annual asset management fee and a one-hundred-and-twenty-five-dollar annual custodial fee. Real estate cannot be sold in seconds, unlike stocks, so liquidity is key. With Fundrise, dividends are automatically paid quarterly and reinvested tax-free within the IRA, allowing your money to compound over time.

4. The Retail Disruptor: Robinhood

Almost everyone knows about company matching, where an employer contributes extra funds to a workplace retirement account as an incentive to save. Until Robinhood disrupted the industry, nobody offered a retail Roth IRA.

With a one-percent cash match on every dollar you contribute, Robinhood is bringing the same disruptive energy to retirement accounts.

Robinhood will automatically credit your account with an extra one percent when you contribute to your Roth IRA. For example, if you max out your annual contribution, you will receive a free cash bonus. As that free money is reinvested over decades, a one-percent boost might seem modest at first, but compound interest completely changes the math over twenty or thirty years.

Robinhood offers zero-dollar account fees and zero-dollar commissions on stocks and ETFs. In exchange for the one-percent match, Robinhood requires you to keep the funds in the account for at least five years before withdrawing them. Although they have been criticized for gamifying investing, their interface is sleek and intuitive. That cash match is pure gold if you don’t treat your retirement account like a casino and stick to long-term index funds.

The company has also introduced Robinhood Social, an in-app social trading platform that lets verified users share real-time trades and track performance metrics directly from the community interface.

5. The Low-Cost Index Pioneer: Vanguard

With Vanguard, you can buy the entire market, sit back, and watch global capitalism work for thirty years.

As the inventor of the index fund, John Bogle founded Vanguard, the spiritual home of passive investing. Due to the company’s structure as a client-owned mutual organization, they are legendary among long-term investors for keeping costs low.

Despite Vanguard’s reputation for DIY index funds, beginners should consider its Vanguard Digital Advisor. Vanguard’s robo-advisor uses its own low-cost index funds to build automated portfolios that cover international equities, stock markets, and bonds. Based on a gross advisory fee, minus a credit for underlying fund expenses, the advisory fee translates to a net fee of roughly fifteen-hundredths of a percent annually.

Using Vanguard’s software, you can see how your retirement timeline balances perfectly with your cash needs by analyzing your external accounts via secure connections. As a purist platform, Vanguard has structural boundaries. To qualify for the Digital Advisor, you must invest at least $3,000.

6. My Top Choice Overall: M1 Finance

Finally, let me share my personal favorite Roth IRA option for beginners. M1 Finance blends the best of both worlds into a perfect hybrid by combining Betterment’s automated goals with Schwab’s hands-on control.

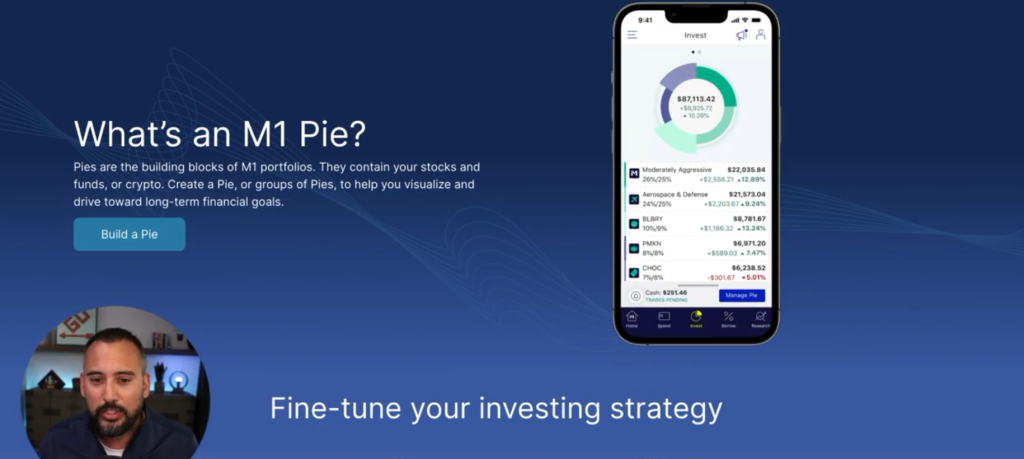

With Investment Pies, M1 Finance organizes your investments visually.

Imagine ordering a custom pizza. You want half pepperoni, a quarter extra cheese, and a quarter mushrooms. You can build your portfolio exactly like that with M1 Finance. Your money can be split between a total stock market ETF, a tech ETF, and an individual growth stock ETF. As soon as you deposit money into M1, the algorithm calculates exactly which pieces of your pie are currently underweight compared to your target percentages and invests the money only in those specific laggards to rebalance your portfolio naturally without selling assets.

If making your own pie seems too intimidating, M1 has an expert pie solution built in. Instead of customizing your portfolio, you can choose a pre-built portfolio crafted by financial professionals, customized to your specific risk tolerance or retirement goal. Unlike robo-advisors, it offers seamless, automated ease, while allowing you to choose individual assets as you gain confidence. Unlike other trading platforms, M1 does not charge any platform fees or commissions. To open an IRA account, you must deposit $500. However, once you have reached that threshold, subsequent deposits can be as low as ten dollars.

Final Thoughts: Just Start

In the end, choosing the perfect platform matters much less than simply taking action. After all, the biggest threat to compounding interest is delay. But if you want the human touch of Schwab, the automated process of Betterment, or the flexibility of M1 Finance, it is best to open an account, set up an automatic recurring deposit, and allow time to work its magic.