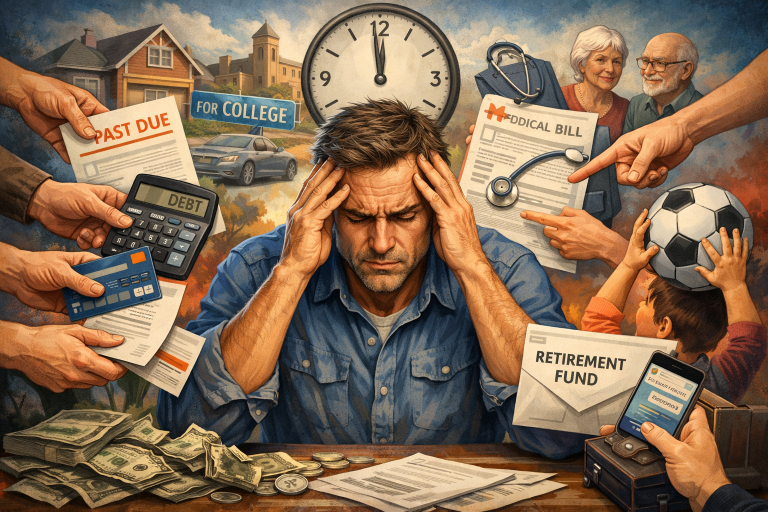

For the generation born between 1965 and 1980, the “Golden Years” still feel like a distant, hazy mirage. Generation X, survivors of the analog-to-digital conversion, the Great Recession, and the rise of the side hustle, is trapped in an unusual economic bind. Further, as the sandwich generation, Gen X has to care for aging parents while also launching their children into an increasingly expensive world. In fact, half of Gen X caregivers also have children, and 56% provide financial support to parents or children.

As many 40- and 50-somethings delay retirement and rethink their financial legacies, it isn’t just an issue of “feeling the squeeze.” It is a systemic, multi-directional financial pressure.

Table of Contents

ToggleThe Anatomy of the Crunch: A Multi-Front War

On three fronts, Gen X is engaged in a financial war. As we consider the sheer scale of the obligations facing this generation, we can begin to understand why they feel so overwhelmed.

The aging parent pillar.

With medical advancements extending life expectancy, Gen Xers are caring for their elderly parents for much longer than previous generations. In addition to being emotionally draining, this care is also financially straining.

Aside from assisted living, home modifications, or simply managing the complex web of Medicare and long-term care insurance, the costs are staggering.

The “failure to launch” factor.

On the other side of the sandwich are the children. As tuition costs surge and the housing market feels increasingly closed, many Gen X parents are supporting “boomerang kids.”

Young adults are moving back home or relying on parental subsidies for insurance, cell phone bills, and student loan payments well into their 20s as a result of skyrocketing tuition costs and a tight housing market.

The retirement gap.

Despite being the “Chief Financial Officer” for everyone else, Gen X often neglects its own retirement accounts. In contrast to Boomers before them, Gen X relied almost entirely on the 401(k) model rather than employer pensions. Their future security is directly impacted if the market dips or if they have to pause contributions for a daughter’s wedding or a father’s hip surgery.

As a result, market volatility is a huge risk to their future. A Gen X professional who pauses contributions to cover a “sandwich generation” crisis, such as paying for a child’s wedding or a parent’s surgery, could lose out on centuries of compound interest.

The data backs up this “crunch.” Research from the Retirement Income Institute at Alliance indicates that Gen Xers are financially unprepared for retirement by nearly every measure. For instance, only 14% of Gen X workers have a traditional pension, compared to 56% of boomers.

The Hidden Costs of Caregiving

It’s not just the direct checks written to doctors and landlords that hurt. In addition to opportunity costs, there is the “money crunch.” In return for caregiving responsibilities at home, many Gen X professionals, particularly women, reduce their work hours or turn down promotions. As a result, about one in five respondents have taken on high levels of debt, reduced or stopped retirement savings, and/or tapped into retirement accounts or investments.

In the long run, the “caregiving penalty” can easily reach six figures if you include the loss of salary, the pause in retirement contributions, and the reduced Social Security benefits due to lower lifetime earnings.

Breaking the Cycle: Strategies for Survival

It’s okay if you feel as if you have the weight of the world on your shoulders. If you want to survive the Gen X money crunch, you’ll have to switch from reactive spending to proactive boundary setting. The following tips will help you navigate the squeeze without collapsing.

Put your oxygen mask on first.

It’s a simple rule in aviation: secure your own mask before helping others. The financial equivalent is that you must save for your retirement before paying your child’s college tuition. Kids can get a loan for school; you can’t get a loan for retirement. Keeping your 401(k) or IRA contributions isn’t selfish — it’s a gift to your kids, ensuring they won’t have to support you later in life.

Have the “uncomfortable conversations” now.

Among the major factors contributing to the Gen X crunch is the lack of transparency.

- With parents. Is there a copy of their estate documents somewhere? Are they covered by long-term care insurance? By understanding their finances, you can avoid panicking in times of crisis and plan ahead.

- With adult children. Establish “sunset dates” for financial support. When their car insurance or streaming service is no longer your responsibility, establish a clear timeline for when they will take over those billings.

Leverage technology and tax advantages.

Gen X is likely tech-savvy enough to use tools that their parents would have overlooked.

- Health Savings Accounts (HSAs). Depending on your tax status, these can be used for your own or your dependents’ health care costs.

- 529 Plans. Don’t forget to use tax-efficient methods if you’re supporting education.

The Psychological Toll: The Cost of Being the “Strong One”

It is impossible to discuss the Gen X money crunch without mentioning mental health issues. Often, this generation is the “glue” that holds families together. In addition to organizing the holiday dinners, managing medication schedules, and budgeting, they are responsible for balancing the checkbook.

In the midst of making stressful financial decisions for three different generations, it’s easy to make mistakes or freeze up.

Key Takeaway: For Gen X, financial wellness isn’t just about balancing a bank account; it’s about setting boundaries with others.

Looking Ahead: Is There Light at the End of the Tunnel?

The good news? Gen X is resilient. These are the kids who learned to be self-sufficient as latchkey kids, and independence is their greatest asset. As a result of using modern financial tools, such as AI-driven budgeting apps and telehealth services that reduce caregiving travel, and the growing flexibility of remote work on retirement planning, Gen X has found a way to automate their lives and reclaim their time.

As the “Sandwich Generation” approaches 60, the emphasis has shifted from accumulation to preservation. It’s no longer about becoming rich, but rather about staying secure.

Summary Table: Gen X Financial Priorities

| Priority Level | Focus Area | Action Step |

| High | Retirement Savings | Maximize employer match and catch-up contributions (available at age 50) |

| Medium | Parental Planning | Review wills, Power of Attorney, and healthcare directives |

| Medium | Debt Reduction | Aggressively target high-interest debt before entering the final decade of work |

| Low | Adult Child Subsidies | Gradually transition “luxury” bills (phone, subscriptions) to the child |

Conclusion

There is a real, relentless cash crunch among Gen Xers. Although being pulled in many directions can be exhausting, it also demonstrates the importance of this generation in society. As the bridge between the past and the future, you are the bridge between the past and the future. Prioritizing your financial health, having truthful conversations with your family, and taking advantage of today’s resources will allow you to survive the sandwich years and emerge with your future intact.

Even though the “Golden Years” have been delayed, they are still attainable with the right strategy.

FAQs

Should I prioritize my child’s college savings over my own retirement?

The short answer is no. As a parent, it feels counterintuitive to learn that, while loans, grants, and scholarships are available for education, there are no retirement loans. Your children won’t need to support you financially later in life if you secure your own financial future — the best gift you can give them in the long run.

How do I start the “money talk” with my aging parents without offending them?

Focus on “empowerment” rather than “taking over.” Ask yourself, “I’ve been updating my wills and health directives recently, and it made me realize I don’t know what yours say if something happens?”

At what age can I start making “catch-up” contributions to my retirement accounts?

After reaching age 50, you are permitted to make additional contributions to your 401(k) and IRA. For Gen Xers who had to pause their savings during their 30s or 40s to cover family expenses, this is a powerful tool.

My adult child moved back home; should I charge them rent?

Depending on their financial situation, many experts suggest charging them a symbolic rent or requiring them to pay for specific household utilities. In addition to preventing “lifestyle creep” for the child, this will help offset your increased grocery and energy costs. Alternatively, you could save their “rent” as a security deposit in a separate account.

How can I manage the “decision fatigue” that comes with being the Sandwich Generation?

Whenever possible, automate. Consider using a shared family calendar app to track appointments, and consider automating transfers to your savings and paying your parents’ recurring bills. If you reduce the number of small financial decisions you have to make daily, you will have more energy for big financial decisions.

Image Credit: Albert Costill/ChatGpt