As we enter the Trump Presidency, there are concerns that must be addressed for anyone in the payment industry. For anyone involved in the global market, this is especially true.

While the payment industry is constantly evolving, there are simply too many unknowns on how the new administration is going to treat the payments industry. For now, there are some issues we need to focus on.

Repealing the CFPB

“Any time the presidency changes parties, you have to expect some significant realignment in regulatory and enforcement policies, and priorities. Due to the divisiveness of this election, I think we can expect a lot of gridlock,” says Judith Rinearson, Partner, K&L Gates LLP.

“On the other hand, with the Senate, the House and the Presidency under one party, there’s also a reasonable chance some major changes in existing law could be implemented. From a payments perspective, I’d keep an eye on Dodd-Frank and the CFPB, both of which will likely come under fire. Overall, the banking and financial services industry might benefit from a reduction in overall regulatory and enforcement burdens.”

It’s no secret that Trump isn’t the biggest Elizabeth Warren fan, who was the founder of the CFPB. Because of this, many political observers believe that Trump would be open to dismantle or change the agency.

“Trump may repeal the CFPB, given his disdain for the Dodd-Frank Wall Street Reform and Consumer Protection Act that created it. If this occurs, the CFPB’s new prepaid card rules will be repealed along with the agency, and another entity will be created to replace it,” says Lori Breitzke, Founder, E&S Consulting.

“If Trump cannot repeal the CFPB, he will instruct the agency to ignore, rather than enforce, the existing rule governing prepaid cards. Trump also will lower taxes on small businesses, fostering growth and the need for more merchant accounts and services.”

![]()

Remittances

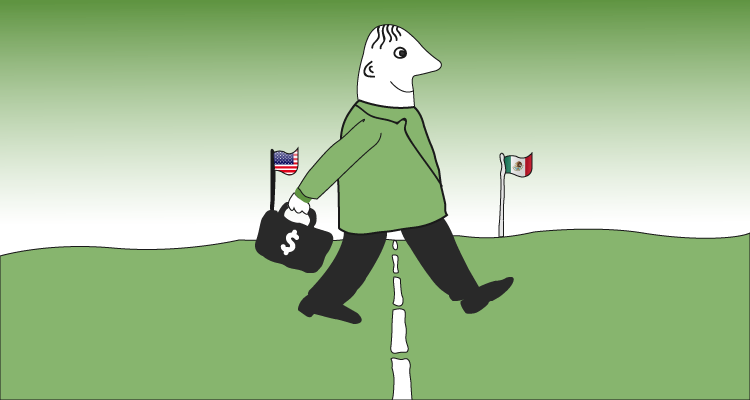

Trump also publically said that would consider threaten to cut off remittance send from the U.S. to Mexico. According to Business Insider, in April 2016, “the Washington Post received a memo regarding Trump’s plans to fund his proposed 1,000-mile border wall between the US and Mexico.” The memo stated that Trump “planned to force Mexico to pay for the wall by invoking the US Patriot Act to cut off portions of the flow of money between the US and Mexico until Mexico made a one-time $5 billion-$10 billion payment. That monetary flow would likely include remittances.”

As John Adams notes in PaymentsSource, this “could have significant ramifications for a major sector of the payments industry.” For starters, “Remittance is big business for the U.S., too. The United States is the world’s biggest sender of remittances worldwide, with nearly $135 billion flowing to other countries each year.”

“Millions of people from abroad work hard in the U.S. and contribute to the economy, sending money to support family and friends overseas,” said Brion Nazzaro, group compliance director and director for WorldRemit Corp. “Likewise families all over the world rely on these remittance payments from people working in the U.S.”

What does this mean?

Adams adds that the “use of remittance as a bargaining tool would take an immediate chunk out of Mexico’s economy, potentially damage U.S. companies and unintentionally rearrange how digital technology executes payments”. This means traditional wire money transfer companies, like Western Union, would be hit the hardest.

“For the traditional guys in the business, I’d watch out,” said Richard Crone, a payments consultant. For the record. MoneyGram has more than 16,000 locations in Mexico and has partnered with Walmart to provide easy and low-cost transfer to Mexico. Western Union has more than 10,000 locations in Mexico. “Cutting off access to the corridor, even temporarily, could drastically change the trajectory for these companies,” notes Business Insider.

Cross-border Payments

However, the remittance industry also happens to be complex. While it could be possible for Trump to use regulations to prevent banks from doing business with firms in Mexico; it’s more difficult to achieve with peer-to-peer transfers.

This is because these mobile applications aren’t categorized as cross-border transfers. This means they can appear to involve two accounts in the U.S., with one of them actually in Mexico.

“Does PayPal or Venmo fall in? Does Xoom?,” asks Crone. Another question that I have, is how can you get payment platforms that use blockchain technology to fall in-line as well. The anonymity and decentralization is the appeal with cryptocurrencies.

At the same time, Trump has championed isolationist trade policies and issued tougher manufacturing restrictions. This could theoretically cause a decrease in international spending since “consumers are either unable to make transactions due to restrictions or unwilling to pay any extra fees.”

Domestic Spending

It’s too early to predict the effect that the Trump administration will have on the economy. On one hand, some people believe that Trump’s proposed tax plan will lower a lot of people’s tax bills outright. Additionally, as Steven Anderson writes in Payment Week, “It will not only be simpler to calculate—which means your need to pay H&R Block might be removed—but it will likely also be lower.”

“That means more cash in pocket, and that means more potential for spending. Spending routed, at least somewhat, through mobile payment systems”. Also, with more expendable income, consumers may be willing to spend for additional services offered by payment companies. This includes premium features, like inventory management or security software.

Also, because there is so much economic uncertainty, businesses and customers may be cautious with their spending.

“A reduction in spending would likely have a negative impact on sales for all the major players in the payments ecosystem, including but not limited to credit card companies, payment gateways, retailers, and even banks,” Business Insider points out.

The Impact on FinTech

Since the 2016 presidential elections caused so much volatility in financial markets, BI Intelligence expects the fintech/payment industry to be one of the many that Trump could disrupt for the following reasons;

- Following the trend in the UK following Brexit, due to economic uncertainty, fintech funding may slow.

- The Consumer Finance Protection Bureau (CFPB) may be dismantled. If so, there would no longer be a fintech-friendly agency that will help simplify compliance and encourage growth.

- If Trump reduces immigration, “it could be a serious setback for the US startup scene, including fintech, which sources a large volume of its skilled workers and entrepreneurs from outside the country.

As BI Intelligence perfectly states, “Regardless of how the situation plays out under President Trump, there is no denying that the world has still entered the most profound era of change for financial services companies since the 1970s brought us index mutual funds, discount brokers and ATMs.”